Key Takeaways

- The Extra Card links to your bank account to help build credit without a credit check.

- The company reports your payments to Experian and Equifax, which may help improve your credit score over time.

- The card charges a monthly fee starting at $20 for basic features or $25 for rewards.

- It offers a spending limit based on your bank balance, referred to as “Spend Power.”

- The card includes real-time credit tracking and 1% rewards with the upgraded plan.

- The Extra Card does not support cash withdrawals and focuses solely on purchases.

Are you wondering about the Extra card and if it might be able to help you build credit without applying for loans and lines of credit? Here, I’m going to break down exactly what the extra card is (including the company itself), how it may help you establish credit and boost your FICO score, and the features and benefits of an account.

This is what’s in store:

- What is the Extra Card?

- Extra Card Features & Benefits

- Extra Card VS Chime: Side-by-Side Comparison

- Frequently Asked Questions

- Conclusion: Does Extra Work to Build Credit?

Now, let’s roll!

What is the Extra Card?

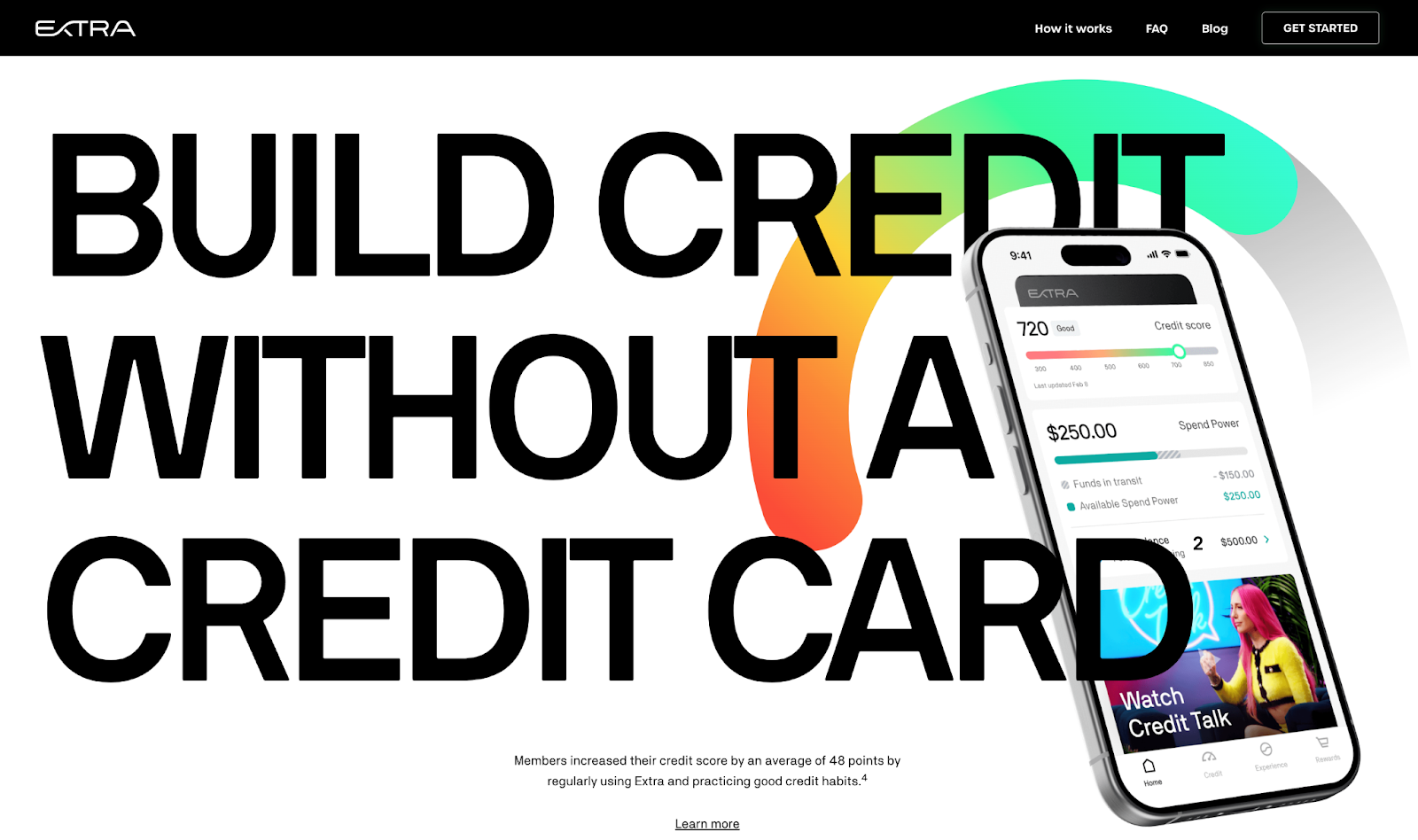

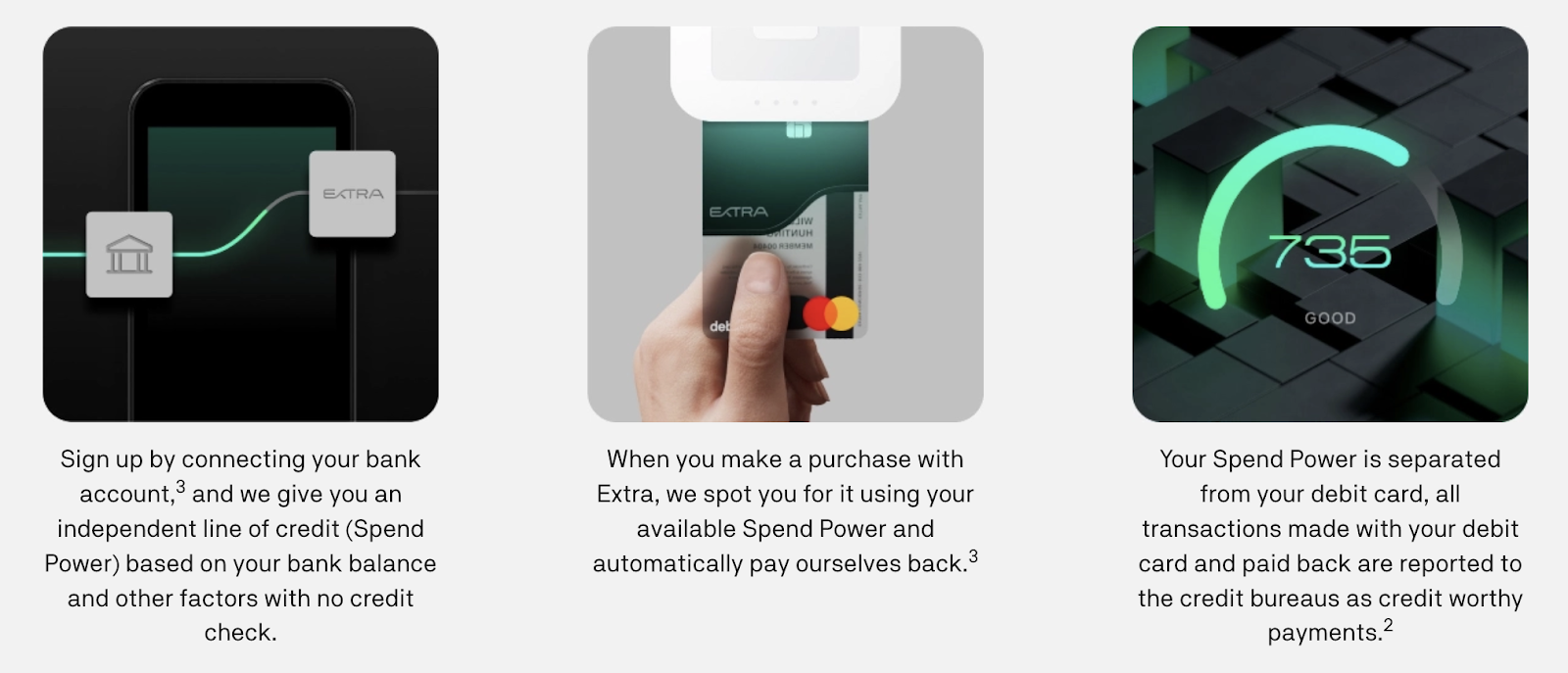

The Extra Card is a debit card designed to help you build credit without needing a traditional credit card. Unlike credit cards that charge high interest or require credit checks, the Extra Card connects directly to your bank account.

It offers a unique feature called “Spend Power,” which sets a spending limit based on your bank balance. When you make purchases, Extra fronts the cost and automatically pays itself back.

These transactions are then reported to credit bureaus as credit-worthy payments to potentially help you improve your credit score over time.

Many users have seen significant credit score improvements by using Extra responsibly and practicing good financial habits. With no interest, hidden fees, or deposits required, the Extra Card offers a simple and effective way to build credit while sticking to your budget.

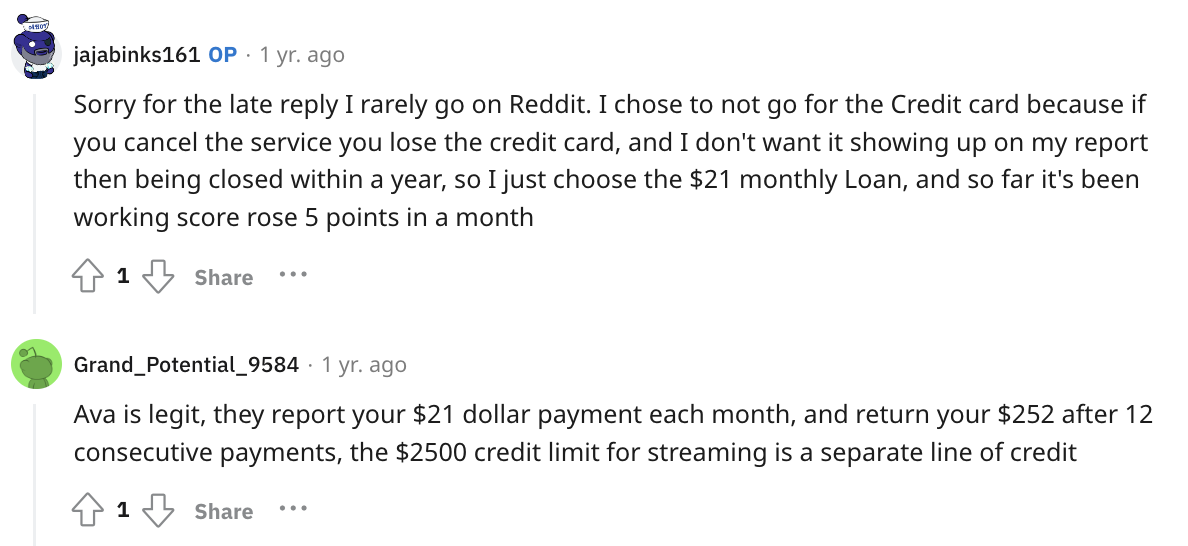

You might also like: Meet the Ava Card: An Uncut Credit Builder Review

Extra Card Requirements

The requirements for Extra are based on income, not credit score. So, it’s a fairly simple application process, as long as your bank account is in good standing and compatible with the system.

To apply for an Extra Card, you need:

- A U.S.-based checking account that is compatible with Plaid.

- A stable bank balance to calculate your “Spend Power.”

To get started, complete the sign-up process, and link your bank account—No credit check is required.

You might also like: Ally Financial Review: No PG, No Credit Check Auto Loans +More

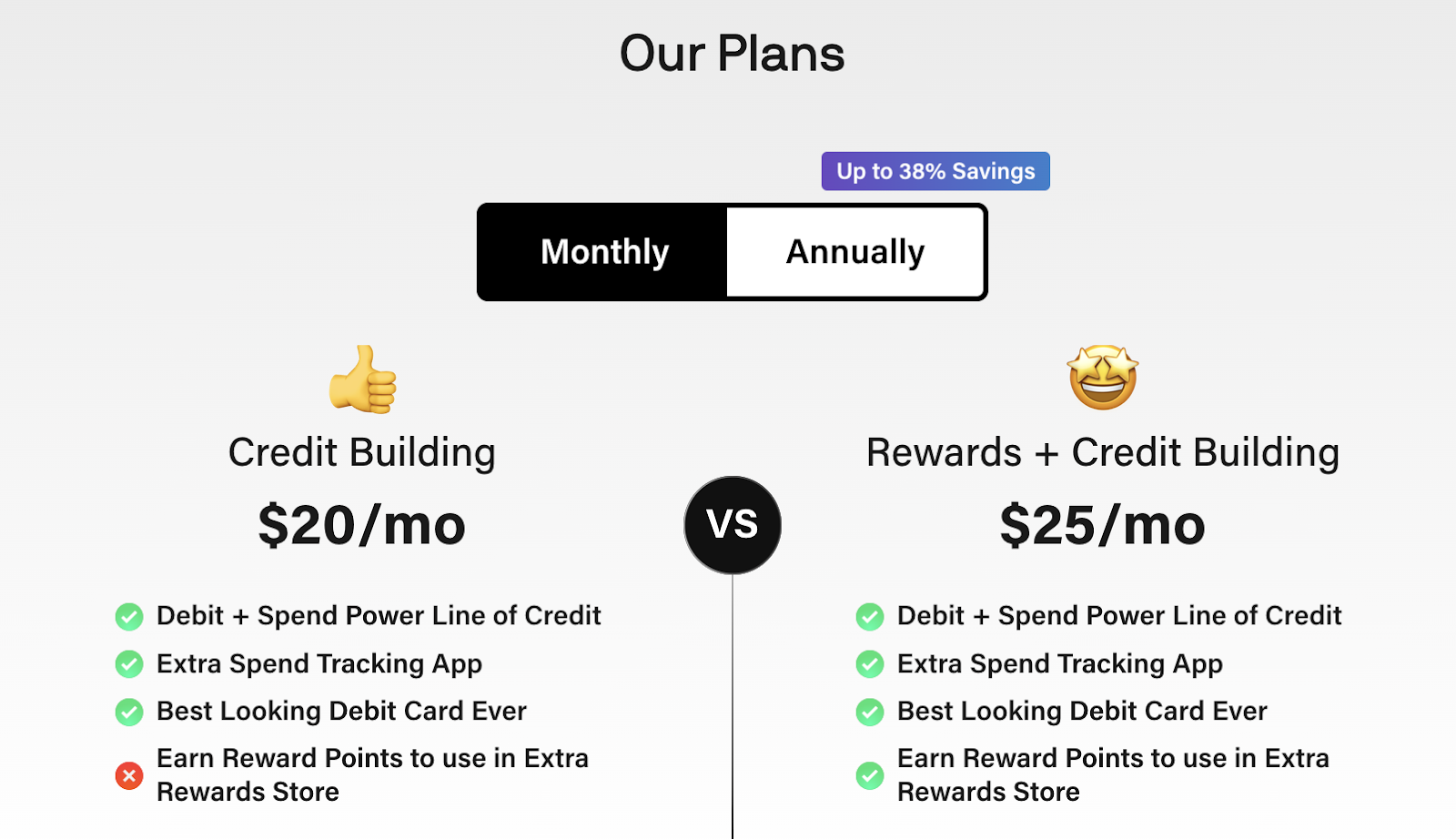

Extra Card Membership Cost

So, how much is an extra card membership? It can’t be free…right? While the pricing isn’t super easy to find on the main website (you have to scroll down the home page a bit), the Extra Card is not free.

It requires a membership plan, with options starting at $20 per month for the Credit Building plan. The Rewards + Credit Building plan, which includes earning points on purchases, costs $25 per month.

These plans cover all features without hidden fees or interest charges.

You might also like: A Credit Stacking Breakdown: What it is & How it Works

Company Overview

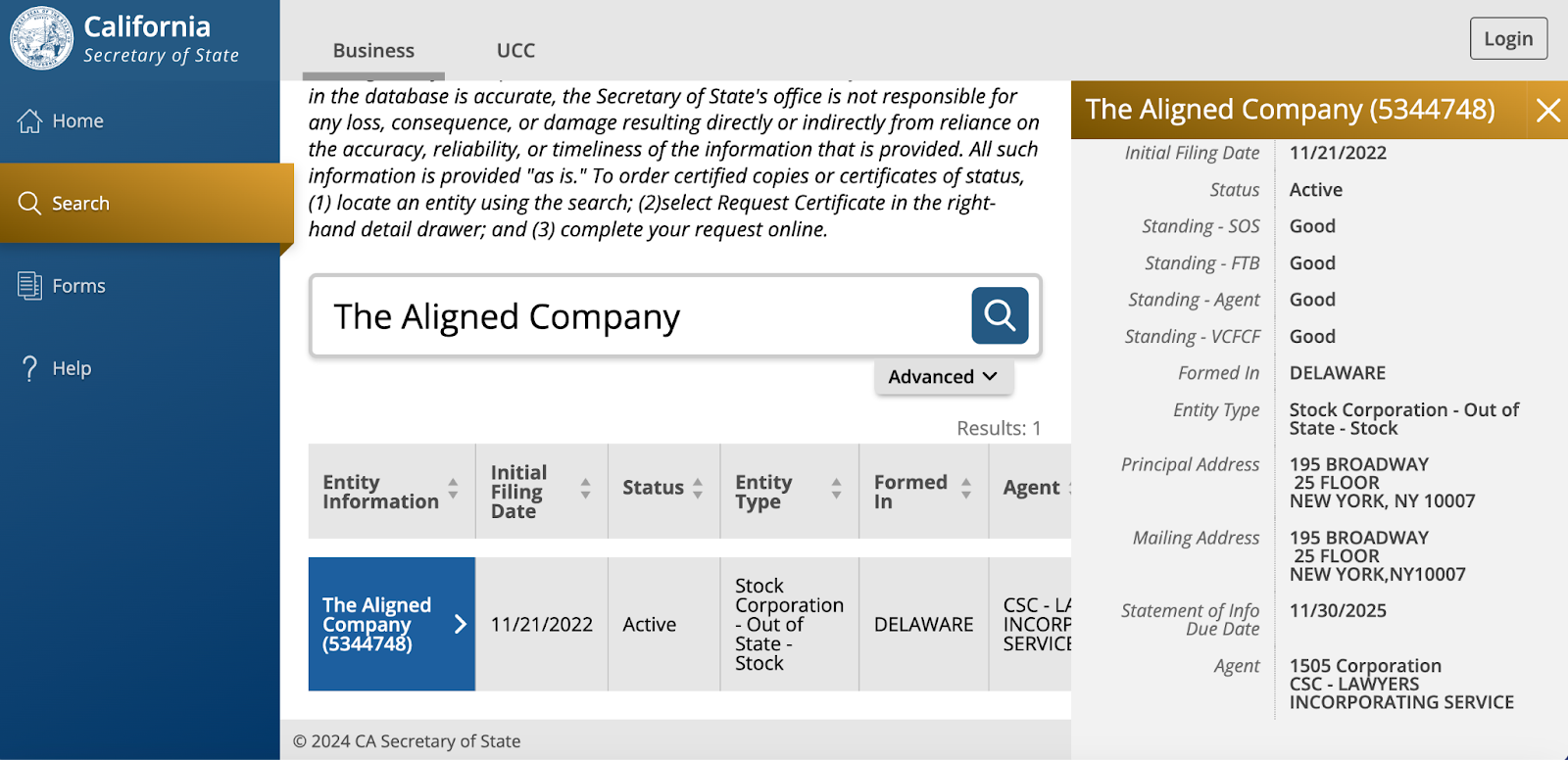

The Aligned Company, Inc., doing business as “Extra”, is a US-based for-profit corporation that was founded in 2018. Depending on which source you look to, they’re either based in “the greater New York area” (Crunchbase) or 3,000 miles away in Los Angeles, California (LinkedIn). It’s actually registered in Delaware, which is common for entities to do since the state’s laws are some of the most corporate-friendly.

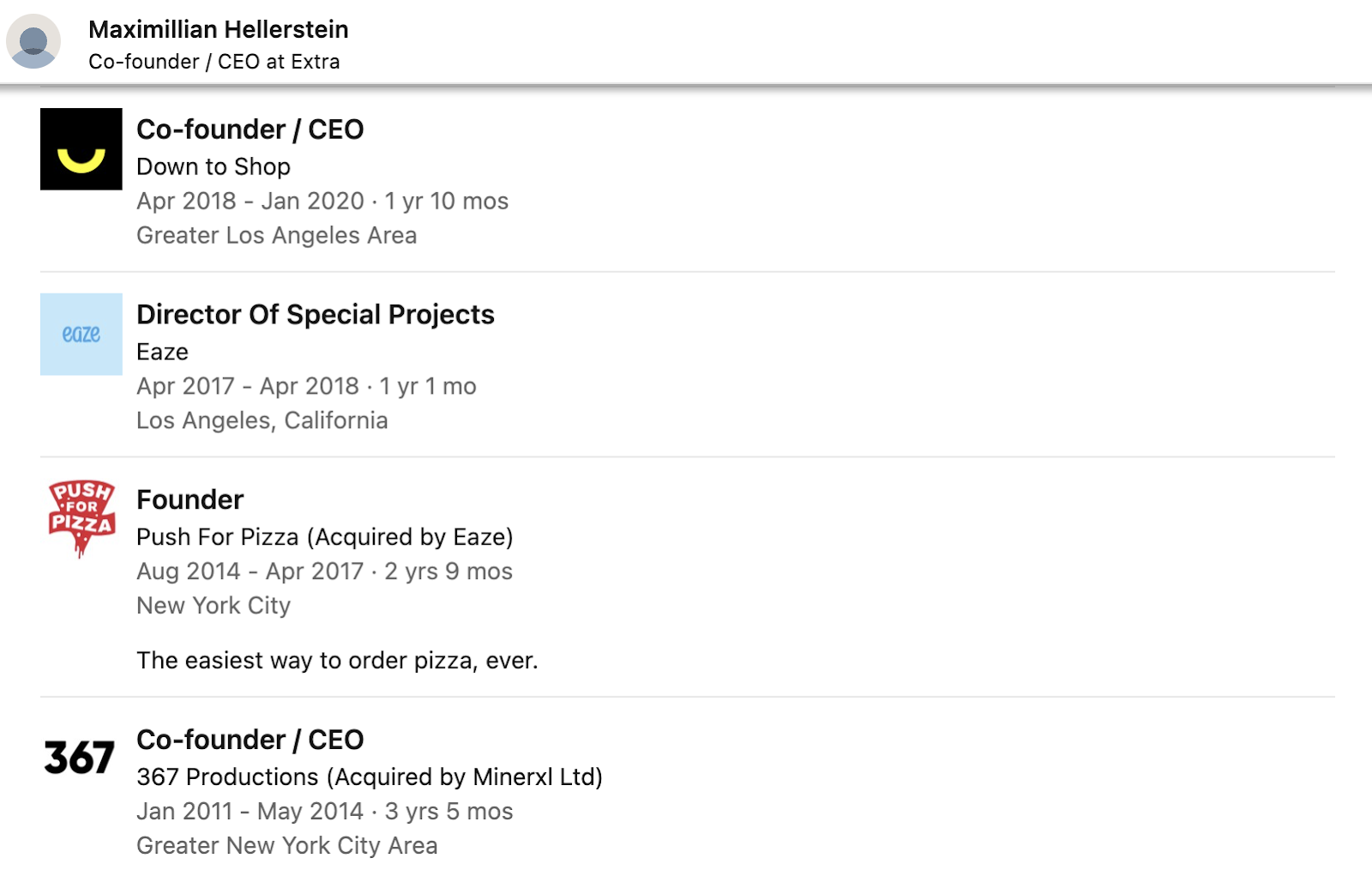

Extra’s co-founders are Biren Shah, Cyrus Summerlin, Maximillian Hellerstein. Shah held executive roles at Extra for a few years and is now with Scanit Technologies. Summerlin is the current Head of Product and Brand. Hellerstein is a serial entrepreneur and Extra’s CEO at present.

Prior to Extra’s launch, Hellerstein founded and co-founded a handful of other businesses in the new tech and marketing arena.

With the Better Business Bureau, Extra maintains an A- rating and 4.8 stars from user reviews. The most common complaint seems to be that Extra will report unpaid membership fees to credit bureaus. So, that’s something to note—If you sign up for a monthly recurring plan and don’t pay, it could impact your credit.

On Trustpilot, the reviews are pretty much raving. Extra’s TrustScore™ is 4.5, which is great for any financial offer. Most of the poor reviews are from a couple years ago, and it seems like the company may have worked out whatever tech issues were causing users stress.

Finally, Redditors have mixed sentiments, which is expected. While some people claim that the card is helping them build credit, others point out that this is not, technically, a debit card. I would agree with them.

Overall, the company seems legit to me. I see no glaring red flags that would lead me to advise you to run away from this offer. However, I would still tell you to keep reading so you can understand the offer and make the best choice for you.

Extra Card Features & Benefits

Discover the standout features of the Extra Card that could make it a game-changer to build credit and manage your finances. From earning rewards to partnering opportunities, here’s what sets Extra apart.

1. Build Credit Without a Traditional Credit Card

The Extra Card helps you improve your credit score without relying on a credit card. Transactions are reported to credit bureaus as credit-worthy payments, allowing you to build credit while avoiding interest rates and credit checks.

2. “Spend Power” Based on Your Bank Balance

Your spending limit, known as “Spend Power,” is determined by your bank balance and other factors. Extra fronts the cost of your purchases and automatically pays itself back, making it a budget-friendly way to manage credit.

3. Earn Reward Points for Everyday Purchases

With an upgraded plan, you can earn up to 1% in points on everyday purchases like gas, groceries, or coffee. Redeem these points for products or gift cards in the Extra Rewards Store, adding value to your spending.

4. No Interest or Hidden Fees

Extra operates on a simple membership model with no interest charges or hidden fees. You get clear and predictable costs, making it an accessible and straightforward tool for credit building.

5. Real-Time Credit Tracking

The Extra App allows you to monitor your spending and track your credit-building progress. It also provides access to your credit score, helping you stay on top of your financial goals.

Extra Card VS Chime: Side-by-Side Comparison

When researching Extra, the most-compared card I saw was Chime. Chime has been around a bit longer, and is set up more like a traditional secured card. Plus, Chime offers fee-free checking accounts.

Here are the main features of both Extra and Chime cards.

| Credit Check | Rewards | Reports to | Card Type | Monthly Cost | |

| No | Up to 1% | Equifax Experian | “Debit” | $20 – $25 |

| No | Chime “Deals” | Transunion Equifax Experian | Secured | $0 |

Neither an Extra nor a Chime card require a credit check—both are issued based on income. And, Chime doesn’t offer 1% rewards points, but they do have Chime Deals, which are essentially discounts on partner offers. And, extra calls their card a “Debit card with superpowers,” rather than a secured card, but some people think this is debatable.

Where Chime stands out is with their three-bureau reporting and $0 monthly membership vs $20+. However, to be fair, if data is reported to Equifax and Experian, it is likely to be picked up by Transunion as well.

On this front, you will have to decide what’s best for you.

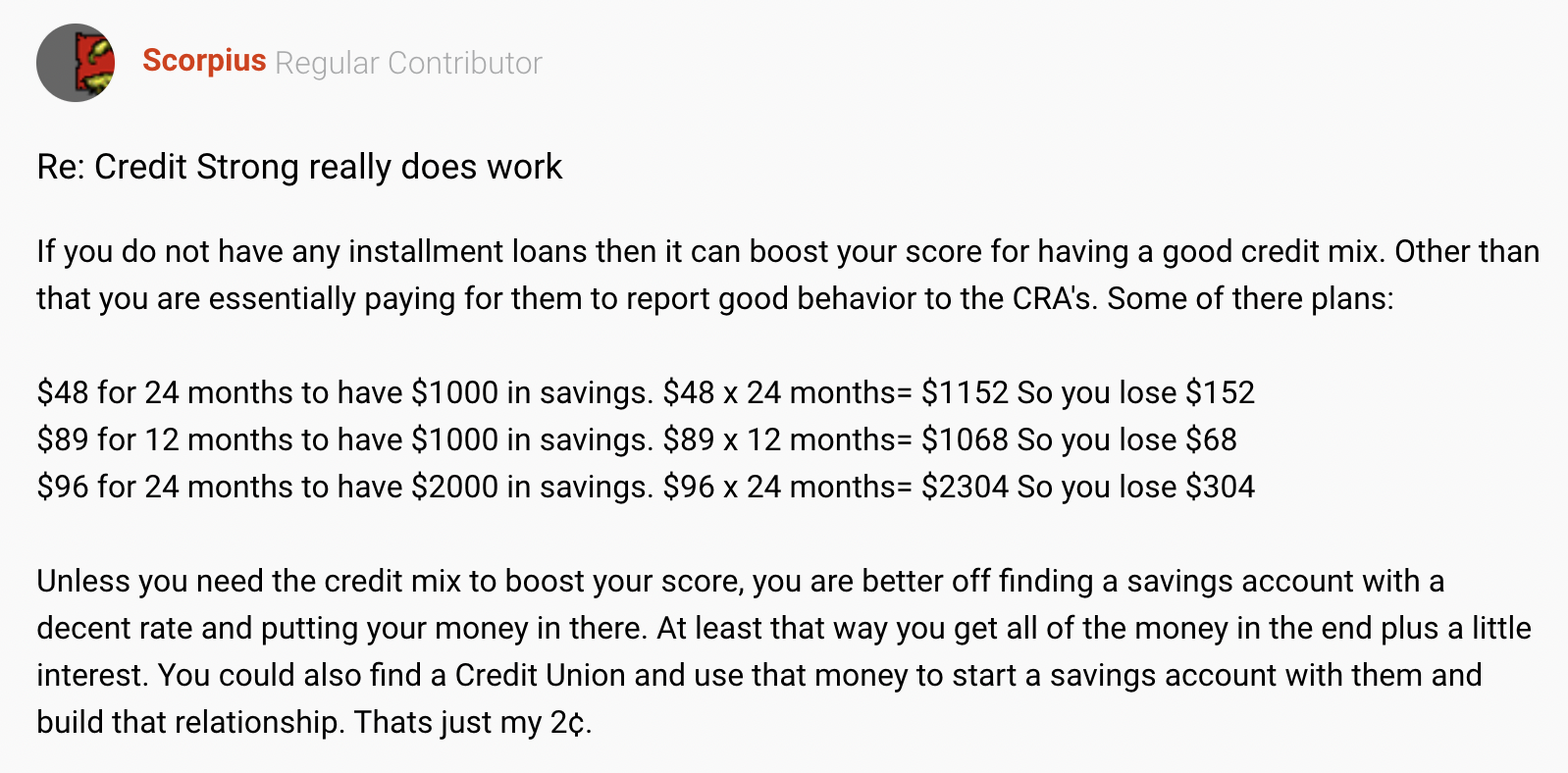

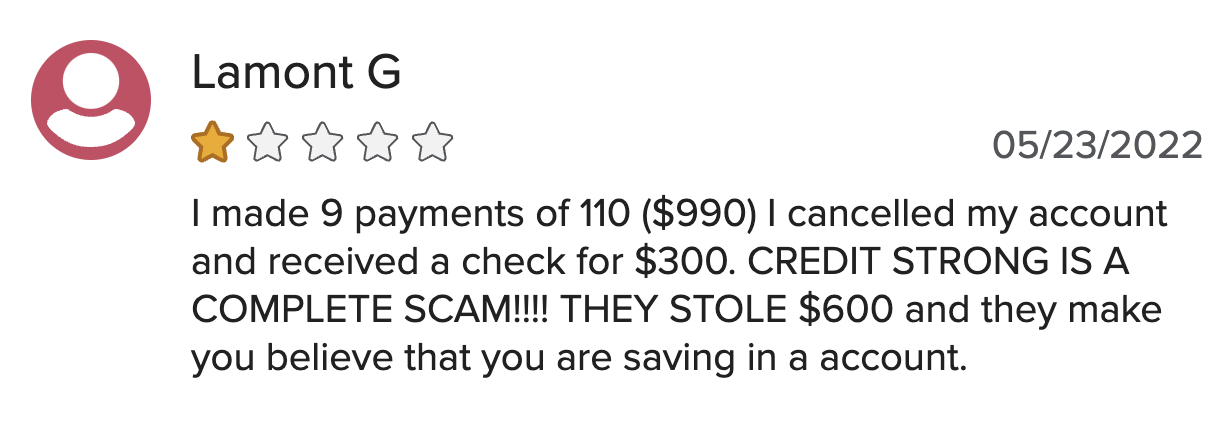

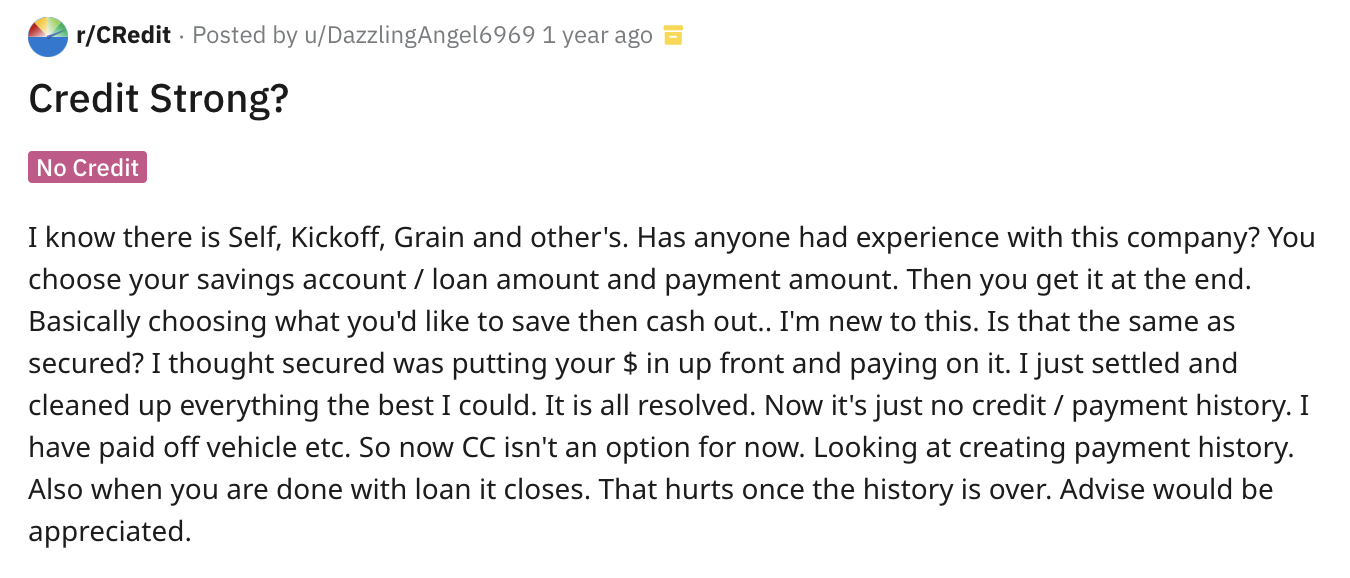

You might also like: Is Credit Strong Legit? A Complete Credit Builder Review

Frequently Asked Questions

Is Extra a real credit card?

No, an Extra card is not a credit card, as it does not have a revolving credit limit. Instead, the funds you spend on an Extra card are immediately paid back out of your checking account. In this way, it’s more like a debit card.

Can you withdraw money from an extra card?

No, the Extra Card does not support cash withdrawals. It is designed for purchases only and helps build credit by reporting those transactions to credit bureaus.

How does an Extra card work?

The Extra Card links to your bank, fronts purchases based on your balance, and reports them to credit bureaus (Experian and Equifax) to help build your credit.

Does Extra help your credit?

Extra can help your credit by reporting your purchases as payments to Experian and Equifax. Many users see credit score improvements when they use the card responsibly and maintain good financial habits.

Conclusion: Does Extra Work to Build Credit?

The Extra Card offers a different way to build credit without relying on traditional credit cards. By linking directly to your bank account and reporting your transactions to credit bureaus, it may help you improve your credit score with responsible use.

While the card comes with a monthly membership fee, its no-interest model and rewards options might provide some value if you want to build credit while sticking to a budget. Whether the Extra Card is the right choice depends on your financial goals and priorities, but it stands out as a flexible option for credit-building.

Do you want to learn how to obtain up to $100K in business credit in as few as 30 days? Join Business Credit Workshop today!