So, you’re looking for the best way to manage your finances with the help of an app. Whether you want an option that’s free and fully customizable, or a paid offer with all the bells and whistles, I’m sure you’ll find something you like in this list.

Let’s explore the best personal finance management software for all budgets, skill levels, and needs.

This is what’s in store:

- What is Personal Finance Software?

- What is the Best Personal Finance Software?

- Frequently Asked Questions

- Final Thoughts

Now, let’s roll!

What is Personal Finance Software?

Personal finance software is a computer or mobile app designed to help individuals manage their personal finances more effectively. These tools provide a range of features to assist with budgeting, tracking expenses, managing investments, and planning for financial goals.

Some features that personal finance software might offer are:

- Budgeting

- Expense tracking

- Investment management

- Financial planning

- Reporting

- Bill payment

- Credit monitoring

Overall, personal finance software makes managing your money easier and more organized, and gives you better control over your financial life.

You might also like: Cred AI Review: Are You Really Better Than Your Bank?

Is There Something Like Quickbooks for Personal Use?

There are several personal finance tools that work like QuickBooks but are designed for personal use. For example, Quicken™ is a solid all-rounder, offering budgeting, expense tracking, investment management, and bill payment. In contrast, Mint™ is great for easy budgeting and expense tracking but doesn’t handle investments.

Meanwhile, YNAB™ (You Need A Budget) is all about zero-based budgeting and tracking expenses, without investment features. On the other hand, Personal Capital™ covers budgeting, expense tracking, and investment management, though it doesn’t focus much on bill payment.

Additionally, Moneydance™ offers budgeting, expense tracking, investment management, reporting, and bill payment. However, PocketGuard™ is useful for budgeting and expense tracking but doesn’t dive deeply into investments or bill payment.

You might also like: 6 Best Fintech Credit Cards to Apply for (Consumer & Business)

How to Choose a New Finance System

To choose the right personal finance management system, start by identifying your specific needs, such as budgeting, expense tracking, investment management, or bill payment. Consider how comfortable you are with technology; some tools offer advanced features that might require a steeper learning curve.

Next, compare the features of various options to find one that matches your needs while staying within your budget. For example, if you need comprehensive financial management and are willing to invest in a subscription, tools like Quicken™ or Personal Capital™ might be suitable.

If you prefer a free or lower-cost solution, options like Mint™ or PocketGuard™ could be better. Ultimately, select a system that balances functionality with ease of use and affordability to best support your financial goals.

You might also like: Meet the Ava Card: An Uncut Credit Builder Review

What is the Best Personal Finance Software?

We could try to rate the best personal finance software based on how many people use it or how many stars each is rated on G2. But, that’s not the best way to choose. You need software that meets your needs and fits your budget and skillset.

Here, I’ll give you a rundown of my top picks. But, first, here’s a quick overview.

- ✅ = Available

- ❌ = Not Available

Now, let’s take a closer look at each—Be sure to check the brand websites for up-to-date features and pricing, as these can change.

You might also like: Credit Secrets Book Review: Can You Erase Bad Credit History?

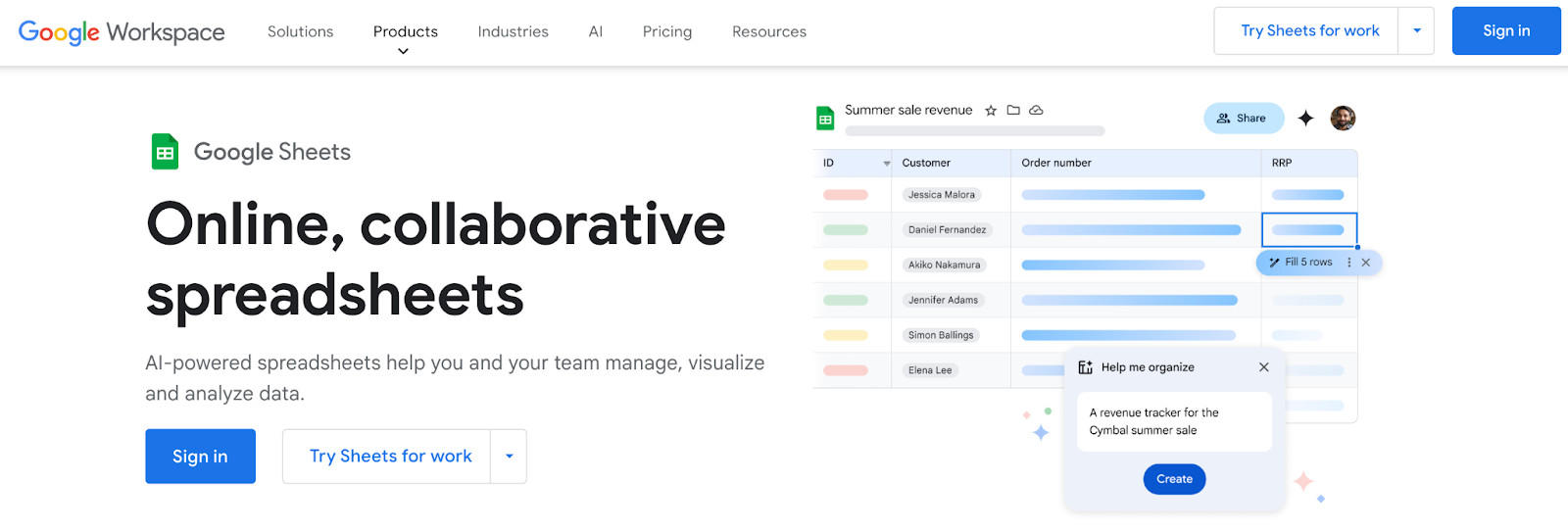

1. Google Sheets

Google Sheets is a free tool from Google that lets you create custom spreadsheets for managing your finances. It’s one of the best free personal finance software choices because it’s completely customizable.

You can use it for:

- Budgeting

- Expense tracking

- Setting financial goals

- Nearly anything else

Google Sheets is fantastic if you like customizing your financial tracking and are comfortable working with spreadsheets. The more you know about the platform, the more robust your system can be. See Google’s cheat sheets and other resources to get the most from this tool.

However, Google Sheets doesn’t come with built-in financial analysis tools, so you would need to set those up yourself—This can be time-consuming if you’re not familiar with creating formulas and templates.

2. GnuCash

GnuCash is a free, open-source accounting software that’s suitable for both personal and small business finances.

It includes features like:

- Double-entry accounting

- Budgeting

- Financial reporting

This makes it a powerful tool to comprehensively manage your finances. It’s ideal if you need a detailed, customizable tool without the cost of commercial software. If you’re the tech-savvy type, check out GnuCash’s documentation to see what all you can do.

On the downside, GnuCash can be complex and may have a steeper learning curve than more user-friendly paid options, which might be a drawback if you prefer a simpler interface.

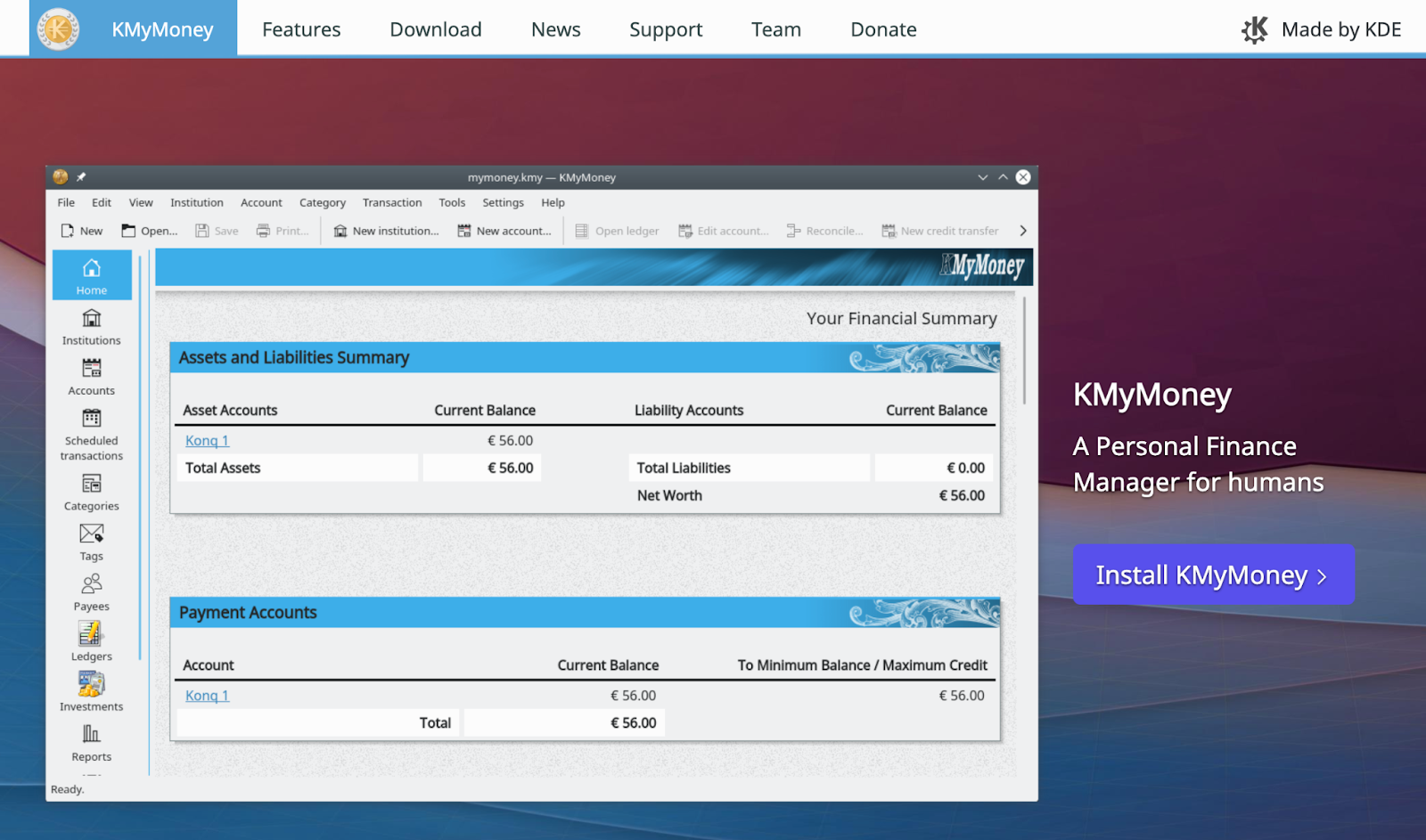

3. KMyMoney

KMyMoney is a free, open-source personal finance manager that supports:

- Multiple accounts

- Budgeting

- Investment tracking

It’s a good choice if you prefer a desktop app with advanced features similar to paid software. Use this offline personal finance software with Linux, Windows, or Mac.

KMyMoney offers robust tools to manage finances but can be overwhelming for beginners due to its extensive feature set—Additionally, its user interface might feel less intuitive compared to more modern financial tools.

4. Mint (Now in CreditKarma)

Mint, now part of Credit Karma by Intuit™, is a free tool that consolidates all your financial accounts into one platform.

You can use Mint to:

- Track spending

- Create budgets

- Receive personalized financial tips

Credit Karma adds value with:

- Free credit score monitoring

- Financial tracking

- Personalized recommendations based on your credit profile

It’s awesome if you want to manage your finances and monitor your credit in one place.

However, both platforms generate revenue through targeted financial product offers, which can feel pushy or intrusive.

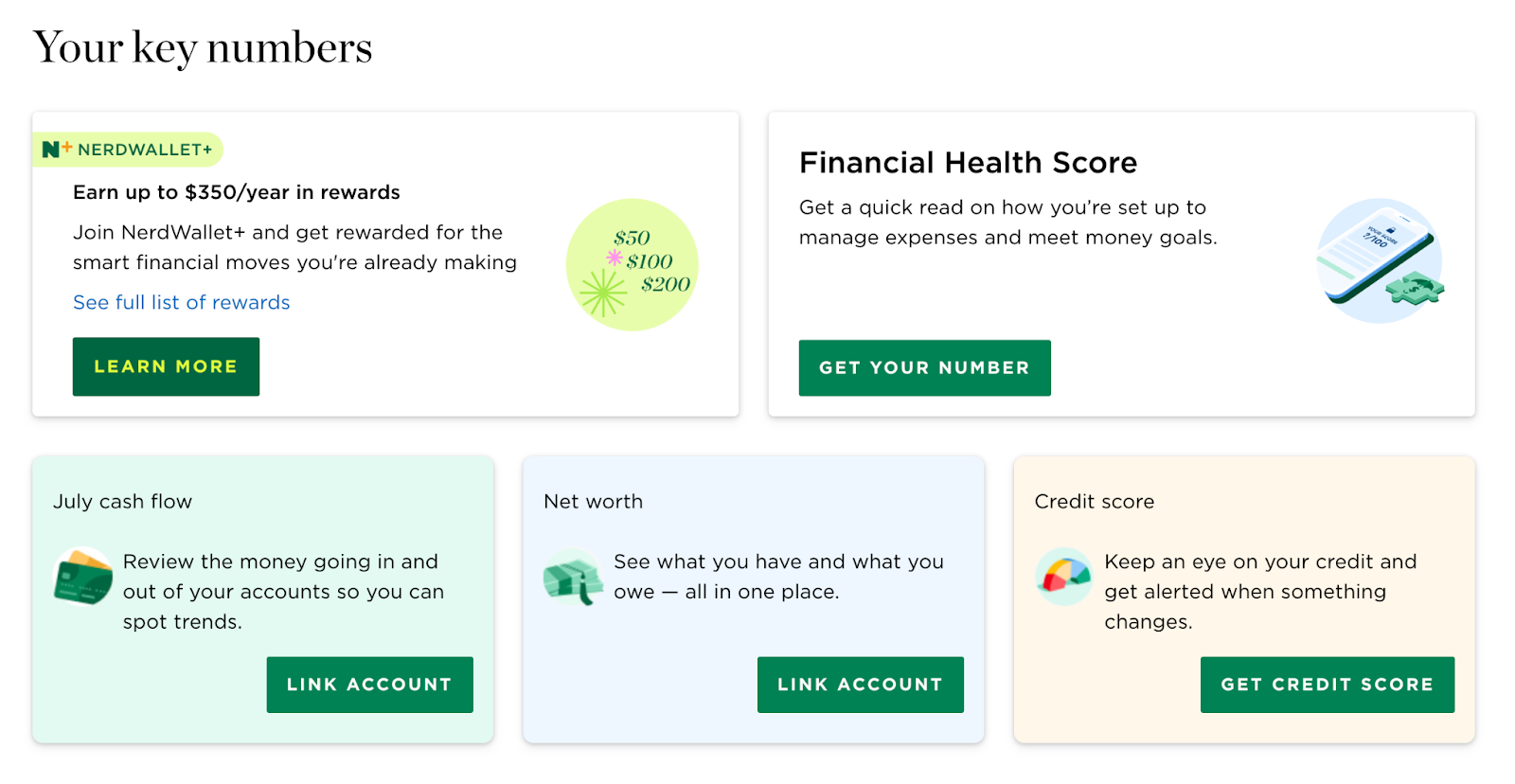

5. NerdWallet

NerdWallet offers free personal finance tools, including:

- Budgeting

- Credit score tracking

- Cash flow management

- Net worth reporting

- Financial product comparisons

It’s helpful if you’re looking for advice on financial products like credit cards and loans, as it provides recommendations based on your financial situation. Plus, their educational resources are vast. And, you’ll get the best experience with the software portion of Nerdwallet’s offer through their mobile app.

However, the focus on product recommendations can sometimes overshadow its budgeting features, and you might encounter frequent prompts to apply for financial products, which can be overwhelming.

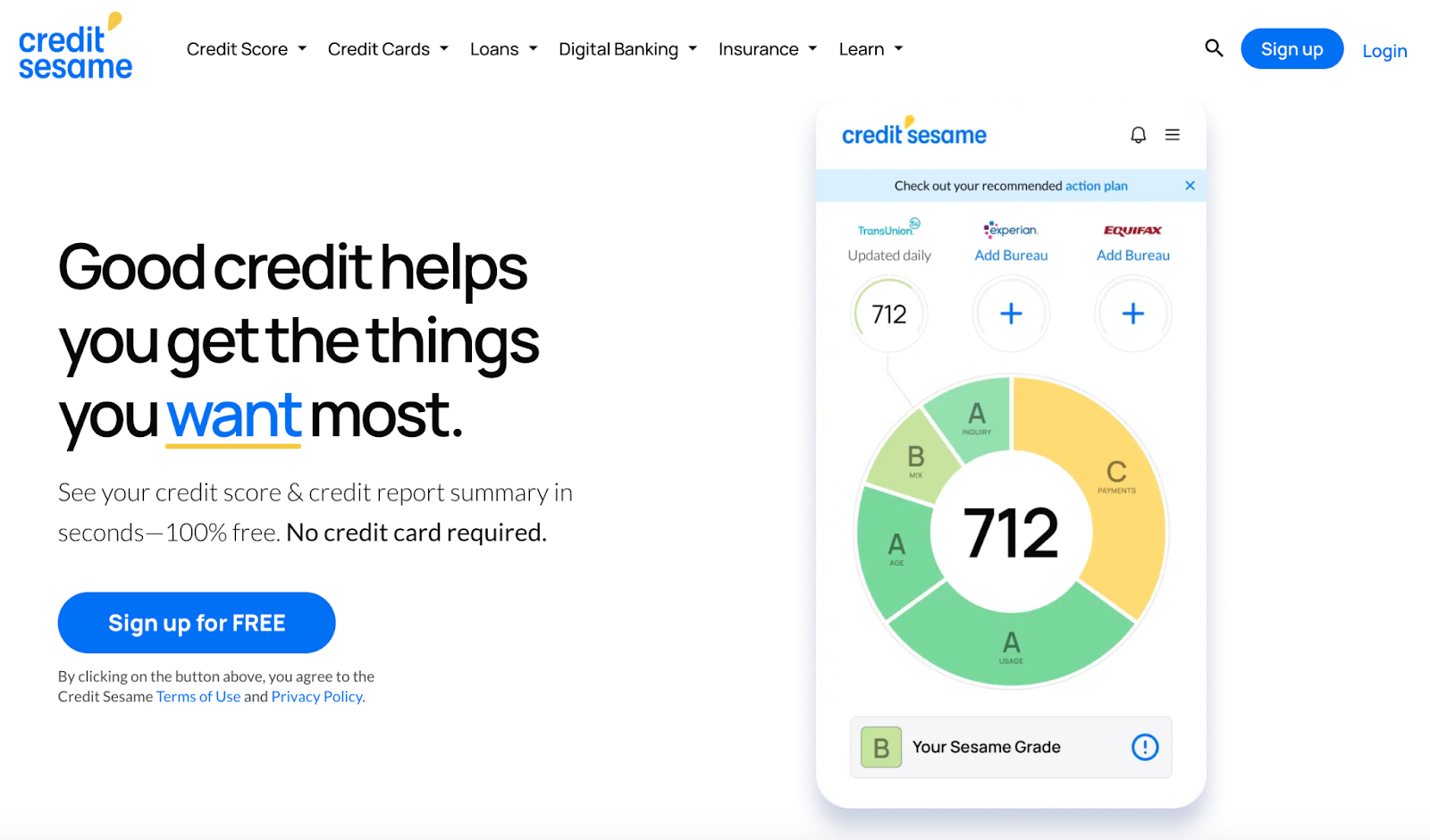

6. Credit Sesame

Credit Sesame offers free credit score monitoring and financial tracking with personalized tips. It’s a good option if you want to monitor your credit score and receive financial insights without paying for a service.

The free version provides basic features, but if you need more advanced tools or additional support, the premium version might be more suitable.

The limitations of the free plan can sometimes make it less comprehensive compared to paid services.

7. WalletHub

WalletHub provides free:

- Credit score & monitoring

- Budgeting tools

- Savings monitoring

- Credit improvement

- Personalized financial advice

It’s useful to get a comprehensive view of your financial health, monitor your credit scores, and get more financially fit.

One downside is that the free version includes ads and frequently promotes credit card offers, which can be distracting and might detract from the overall user experience.

8. Rocket Money

Rocket Money, formerly known as Truebill, starts at about $3.99 per month (though you can access some features for free). It’s best known for deleting duplicate subscriptions, but does so much more.

This app helps with:

- Budgeting

- Credit score & monitoring

- Subscription management

- Expense tracking

This tool is useful if you want to keep track of your subscriptions and manage your spending more effectively (I’m a fan, fyi).

However, some features might be limited to higher-tier plans, and the basic version might not offer all the tools needed for comprehensive financial management.

9. Simplifi

Simplifi by Quicken costs around $3.99 per month.

It offers features like:

- Budgeting

- Expense management

- Financial goal setting

This tool is great if you want a straightforward, user-friendly way to manage your finances.

But, it may lack some of the more advanced features found in higher-priced financial management solutions—This might be a drawback if you need more extensive tools.

10. YNAB (You Need A Budget)

YNAB costs up to $14.99 per month or $99 per year and focuses on zero-based budgeting, where every dollar is allocated to a specific goal. This method helps you actively manage your budget and develop better financial habits.

YNAB is ideal if you want a structured approach to budgeting and are committed to following its principles.

The cost might be a barrier for some, and its budgeting methodology can take some time to get used to.

11. Empower Personal Wealth

Empower Personal Wealth (previously Personal Capital) offers free financial tracking tools along with optional paid advisory services through Empower. The platform is designed for retirement savings and investments.

The free version includes:

- Net worth calculation

- Investment tracking

- Budgeting

It gives you a broad view of your financial health. If you’re interested in professional investment advice, the paid advisory service starts at $100K in investments, with a fee of about 0.89% of assets under management. The fee decreases as your investment balance goes up.

This service is useful for in-depth financial planning, but the cost might be high if you’re looking for lower fees or if you don’t have a significant investment portfolio.

12. Quicken Classic Deluxe

Quicken Classic Deluxe starts at $2.99 per month and offers features like:

- Expense tracking

- Budgeting

- Bill management

It provides a comprehensive set of tools for managing your finances in one place. Quicken Deluxe is a solid option if you need a robust personal finance tool with various features.

However, it requires an annual subscription, which might not be ideal if you’re seeking a free or one-time payment solution.

Frequently Asked Questions

What is the best way to keep track of personal finances?

Use a tool that fits your needs. Mint™ is good for budgeting, Quicken™ and Personal Capital™ offer more features. Pick one that matches your goals and comfort level.

Is there a better financial program than Quicken?

Yes, depending on your needs. Personal Capital™ is strong in investment management, YNAB™ focuses on budgeting, and Mint™ is a solid free option. Choose based on required features.

Can you use accounting software for personal use?

Yes, software like GnuCash and Moneydance can manage personal finances. They offer budgeting and tracking but might be complex.

What is the best tool for financial analysis?

Personal Capital™ and Quicken™ are great for financial analysis due to their robust reporting features. Look for tools with strong reporting capabilities.

Do finance people use Excel?

Yes, finance professionals use Excel, Google Sheets, or similar spreadsheets, often alongside other financial software, based on their needs.

Final Thoughts

Choosing the best personal finance software depends on your needs, budget, and comfort level with technology. From free tools like Google Sheets and Mint to more advanced options like Quicken Deluxe and Personal Capital, there’s something for everyone.

Consider what features are most important to you, whether it’s budgeting, expense tracking, investment management, or credit monitoring. Remember, the right tool will help you stay organized, manage your money more effectively, and achieve your financial goals.

Explore the options, and pick the one that fits best with your personal financial strategy.

Do you want to learn how to obtain up to $100K in business credit in as few as 30 days? Join Business Credit Workshop today!