Key Takeaways

- The Verve Mastercard® helps rebuild credit by reporting to all three major bureaus.

- It is designed for people with less-than-perfect credit.

- The card has high fees, including up to $125 annually and monthly fees.

- It also has a 35.90% APR and potential monthly fees after the first year.

- You need a pre-qualification letter and reservation number to apply.

- The card is issued by The Bank of Missouri and serviced by Continental Finance.

Tens of thousands of people search for more info about the Verve credit card each month. And, the readily-available details from the issuing bank aren’t super easy to navigate. So, here, I want to lay it all out to let you know exactly what you could be getting into if you apply for this card.

Find out more about the terms and fees, learn how to apply, and look behind the curtain at the company that offers the card. Then, explore a breakdown of Verve credit card reviews from cardholders, a list of features, and answers to frequently asked questions.

This is what’s in store:

Now, let’s dive in!

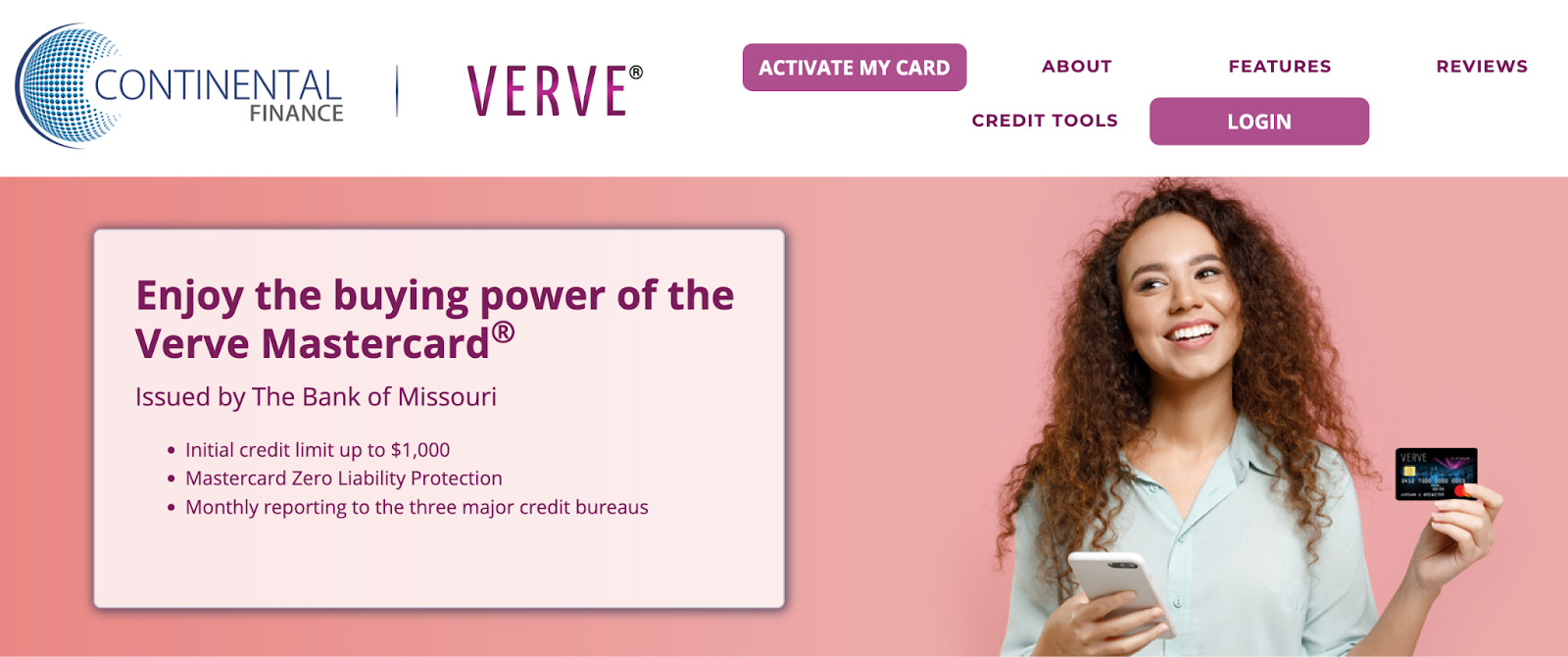

What is Verve Credit Card?

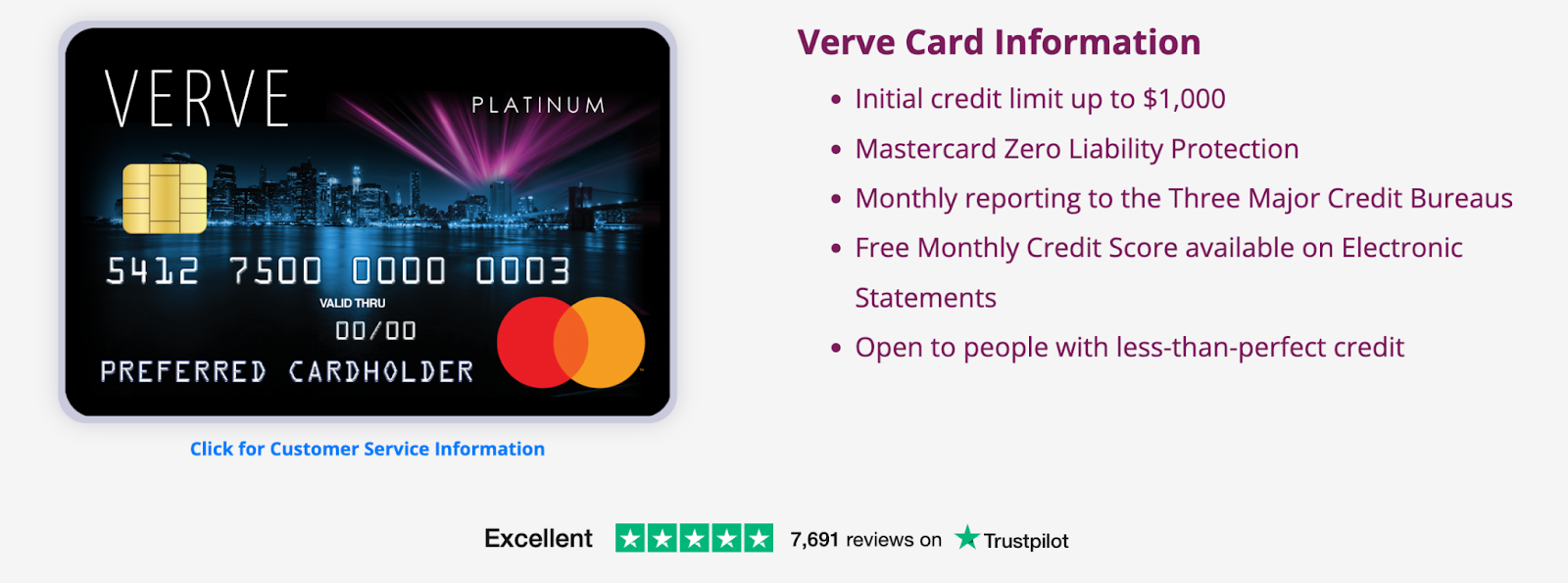

The Verve Mastercard® is a credit card designed for people with less-than-perfect credit. It offers an initial credit limit of up to $1,000 and includes Mastercard Zero Liability Protection, which helps protect you from unauthorized charges.

This card also reports payment history to all three major credit bureaus:

- Experian

- Equifax

- TransUnion

Regularly-reported on-time payments can help you build or improve your credit over time. So, a Verve card can be an option to consider if you want to establish or rebuild credit. But, as with any financial product, you need to know the terms and fees before you apply.

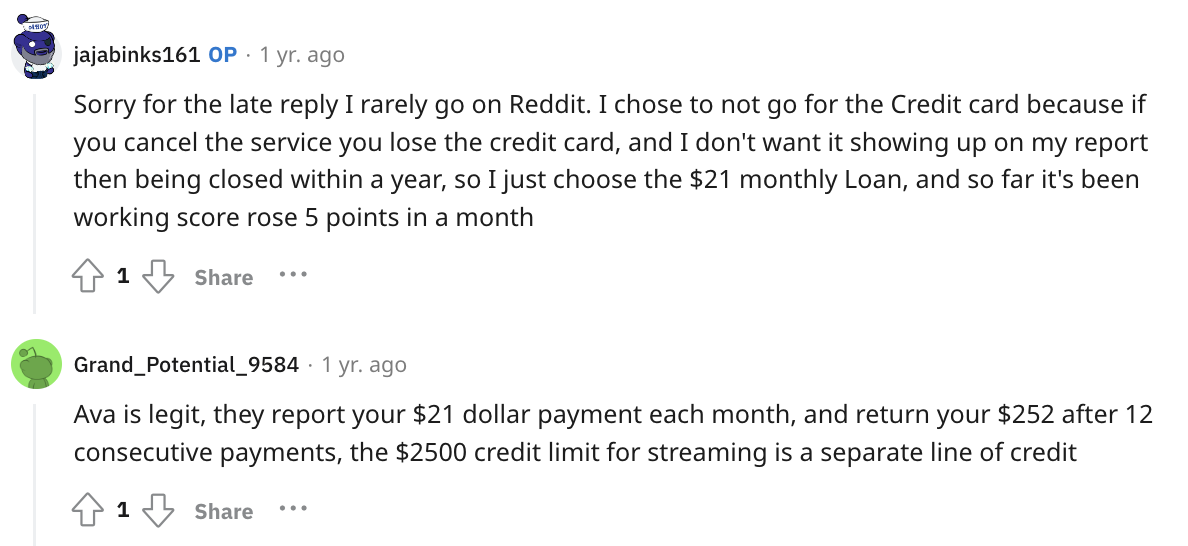

You might also like: Meet the Ava Card: An Uncut Credit Builder Review

Verve Credit Card Requirements

To qualify for the Verve Mastercard®, you must:

- Be at least 18 years old (19 in some states).

- Provide a valid SSN and government-issued ID.

- Show proof of a stable income.

- Be a U.S. resident.

- Have a credit score of at least 500.

The card is available to individuals with fair, poor, or limited credit. Approval and interest rate depend on your credit history and income.

Recommended: Credit Secrets Book Review: Can You Erase Bad Credit History?

Verve Credit Card Fees

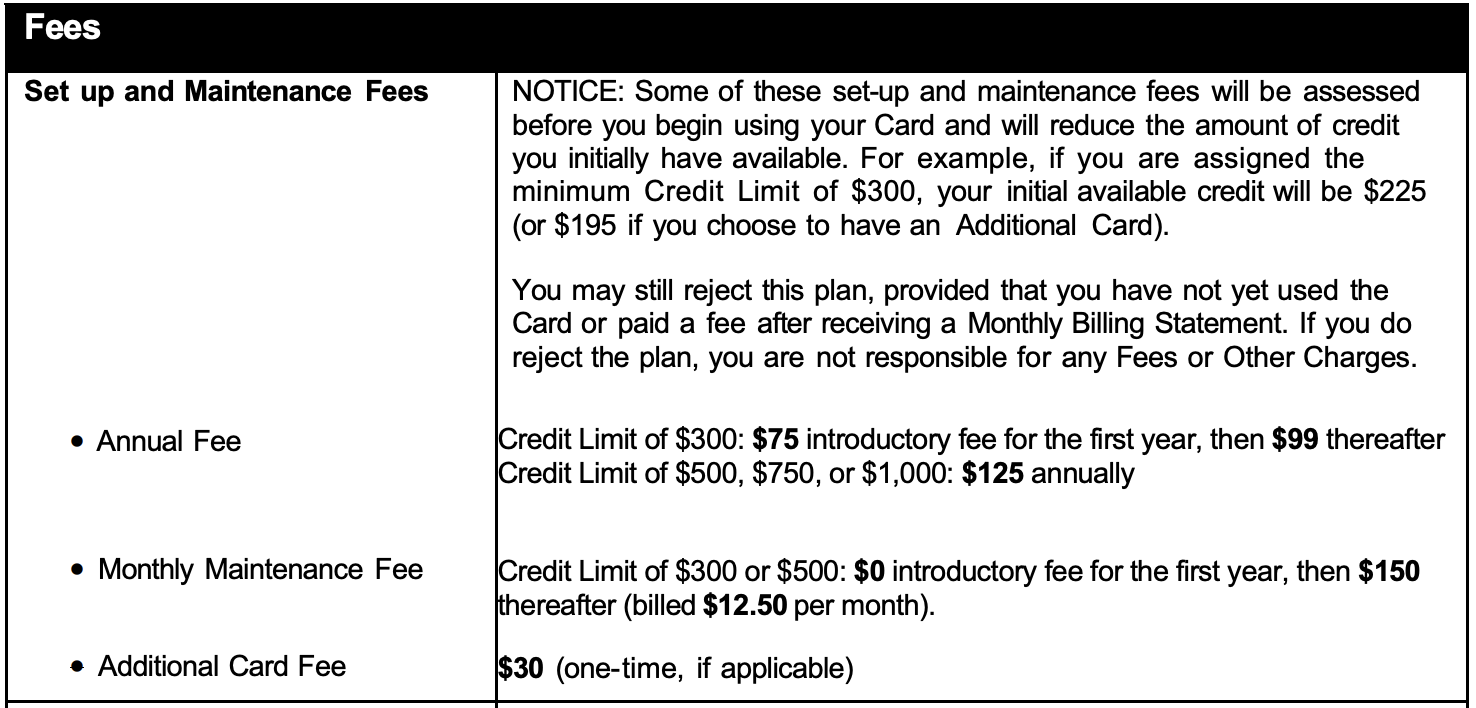

According to the Verve cardholder agreement, the Verve Mastercard® has specific fees and interest rates based on your credit limit:

- $75 annual fee for the first year; $99 annually thereafter for a $300 credit limit.

- $125 annual fee for credit limits of $500, $750, or $1,000.

- $0 monthly maintenance for the first year; $10 per month thereafter for credit limits of $300 or $500.

- No monthly maintenance fee for credit limits of $750 or $1,000.

- 35.90%+ APR for purchases and cash advances.

So, if you get a $1,000 Verve Mastercard limit and carry a $400 balance for two years without additional charges, it will cost you about $537 in fees and interest. This includes $250 in annual fees ($125 per year) and approximately $287 in interest, assuming the 35.90% APR and no payments beyond the minimum to reduce the balance.

35.90% APR and a $125 annual fee are high compared to average cards, which have APRs of 16%-24% and lower or no annual fees. It’s costly but aimed at those with poor credit.

You might also like: Can an Extra Card Help You Build Credit Without a Credit Card?

How to Apply for a Verve Credit Card

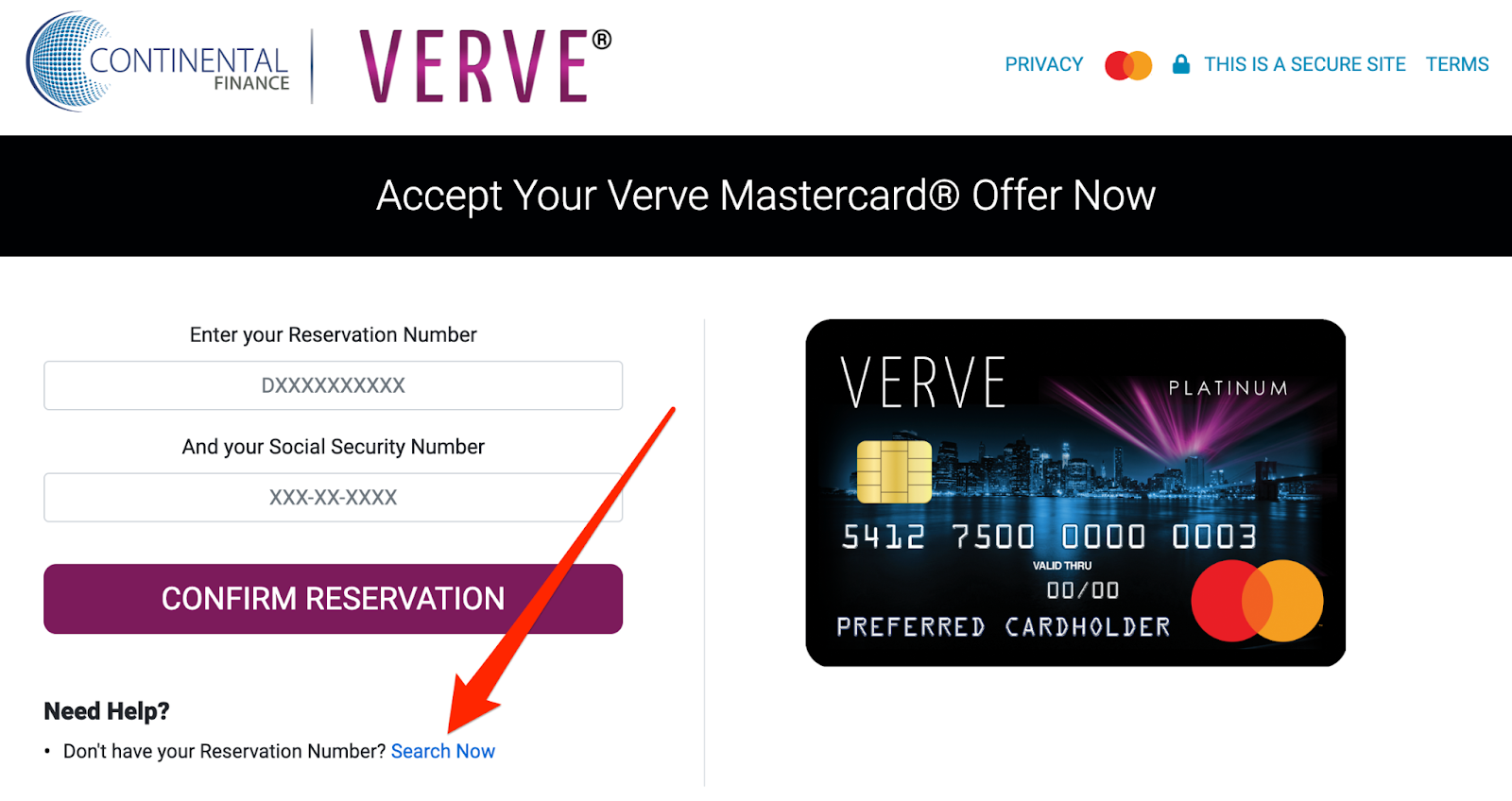

When I first visited the Verve card’s landing page, it took me a minute to figure out how to access the application. The website’s instructions, which start with, “Applying for a Verve card has never been easier,” is extremely misleading.

So, to apply, you need to:

- Head over to yourvervecard.com.

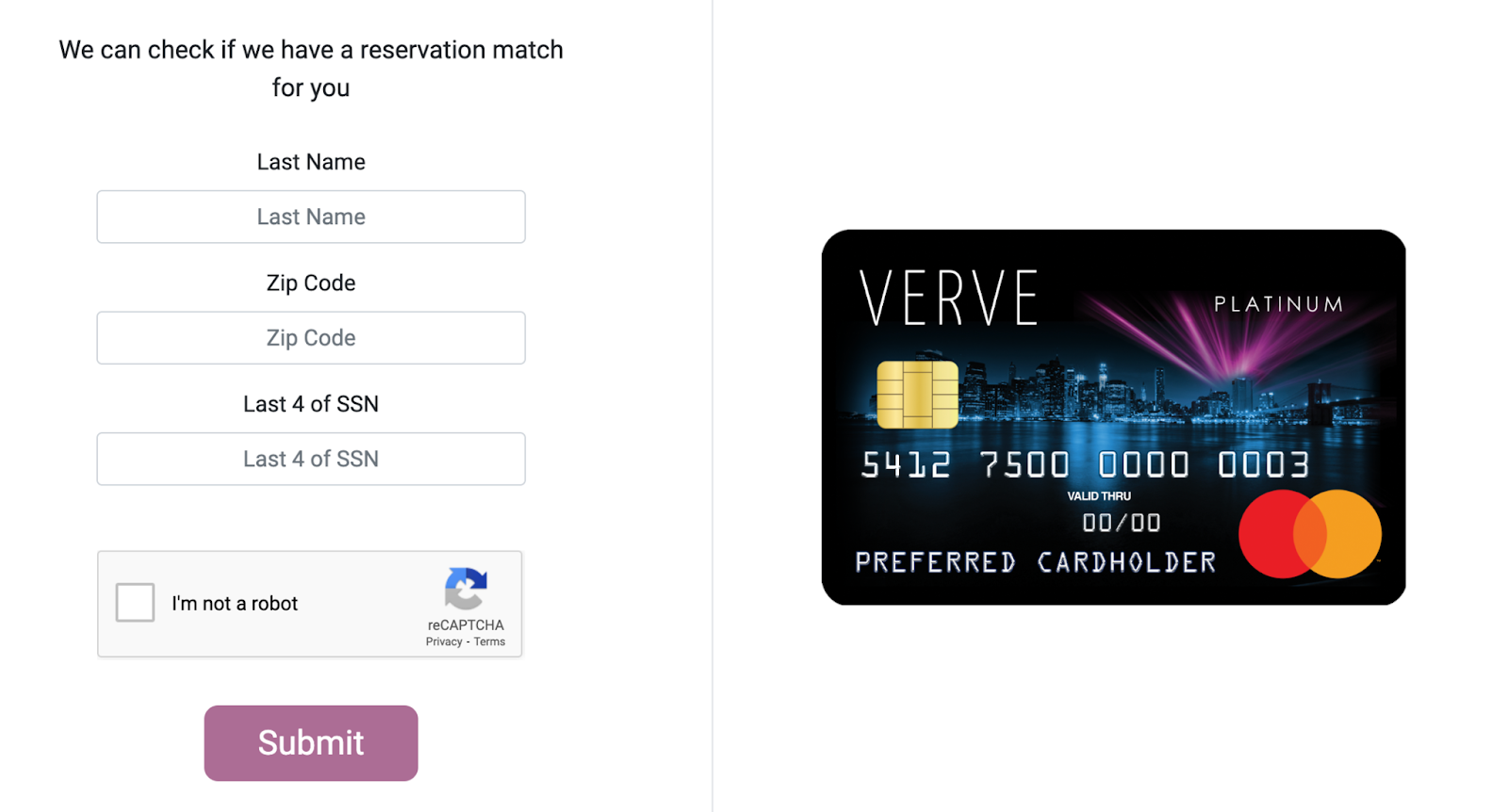

- If you have your reservation, you can follow the prompts on the page. Otherwise, you need to click “Search Now” at the bottom of the page.

- You’ll be taken to a new screen where you can enter your last name, zip code, and the last four digits of your social security number to look-up your “reservation.”

While the advertising says otherwise, the only way to apply for a Verve card online is with a pre-qualification letter and reservation number (I don’t love confusing information from the companies I do business with or recommend.).

You might also like: Is Credit Strong Legit? A Complete Credit Builder Review

Company Overview

The Verve Mastercard is issued by The Bank of Missouri and serviced by Continental Finance Company. Continental Finance specializes in credit cards for individuals who may not qualify for traditional options.

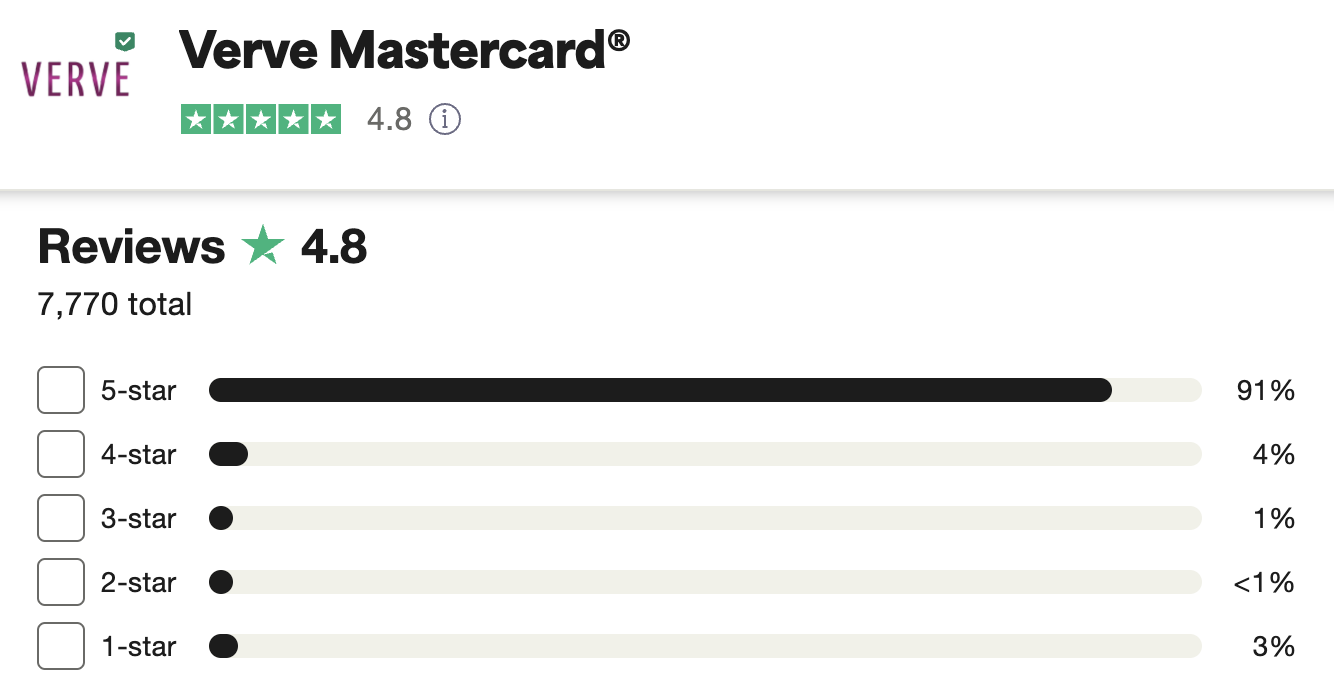

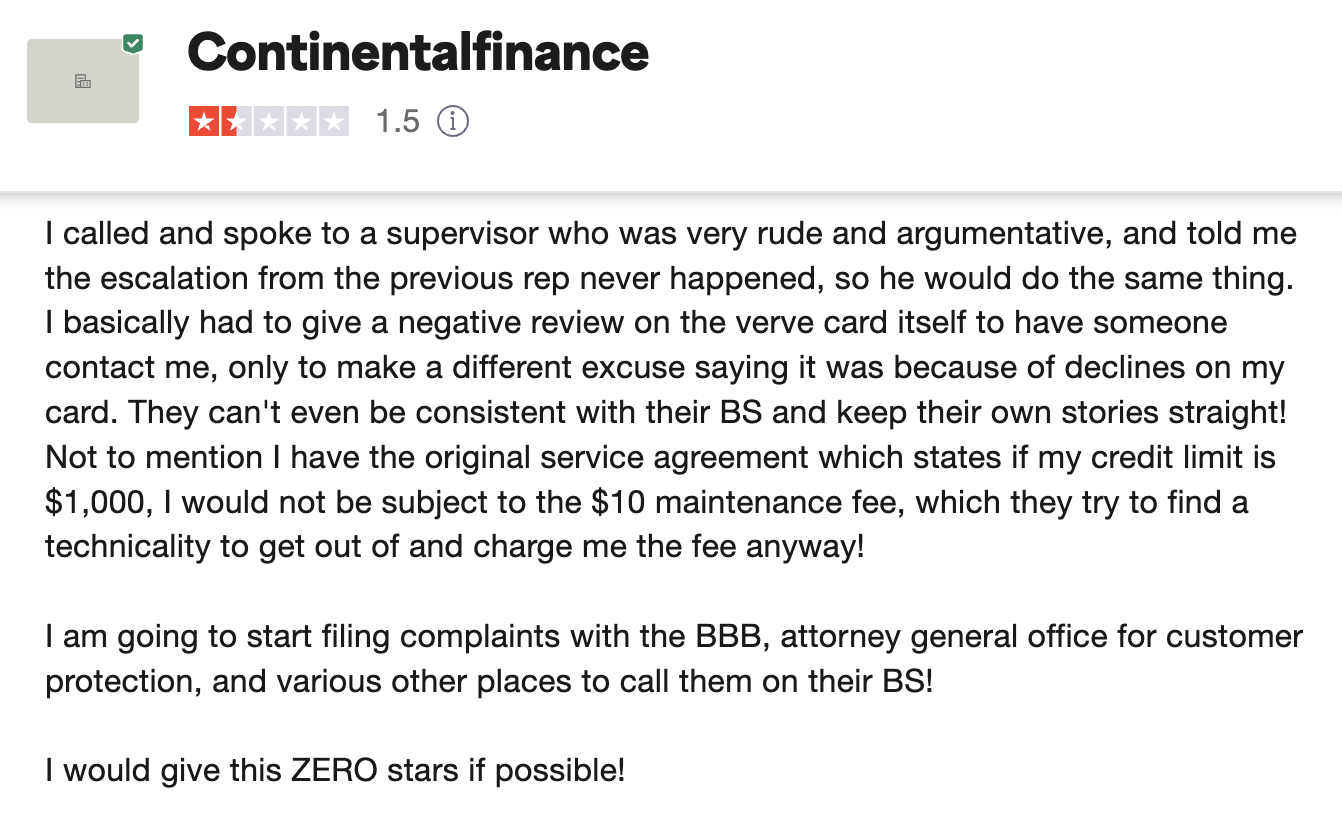

And, the first thing I need to say is that the 5-Star Trustpilot reviews advertised on the Verve website are, again, super deceiving. While the Verve Mastercard reviews—which date back to 2019—are mostly positive, Continental Finance reviews aren’t so shiny.

The Verve card reviews show an overall TrustScore of 4.8 out of 5, which is good. But, the company asks for reviews, pays for extra Trustpilot features, and allegedly uses AI to help with replies.

In the meantime, Continental Finance has almost exclusively poor reviews, several of them related specifically to Verve card services. And Continental Finance hasn’t replied to ANY of these reviews, despite the fact that they did claim the profile.

However, before we burn them at the stake, they are Better Business Bureau (BBB) accredited with an A+ rating. This is despite the fact that they get a couple hundred complaints on the BBB platform each year.

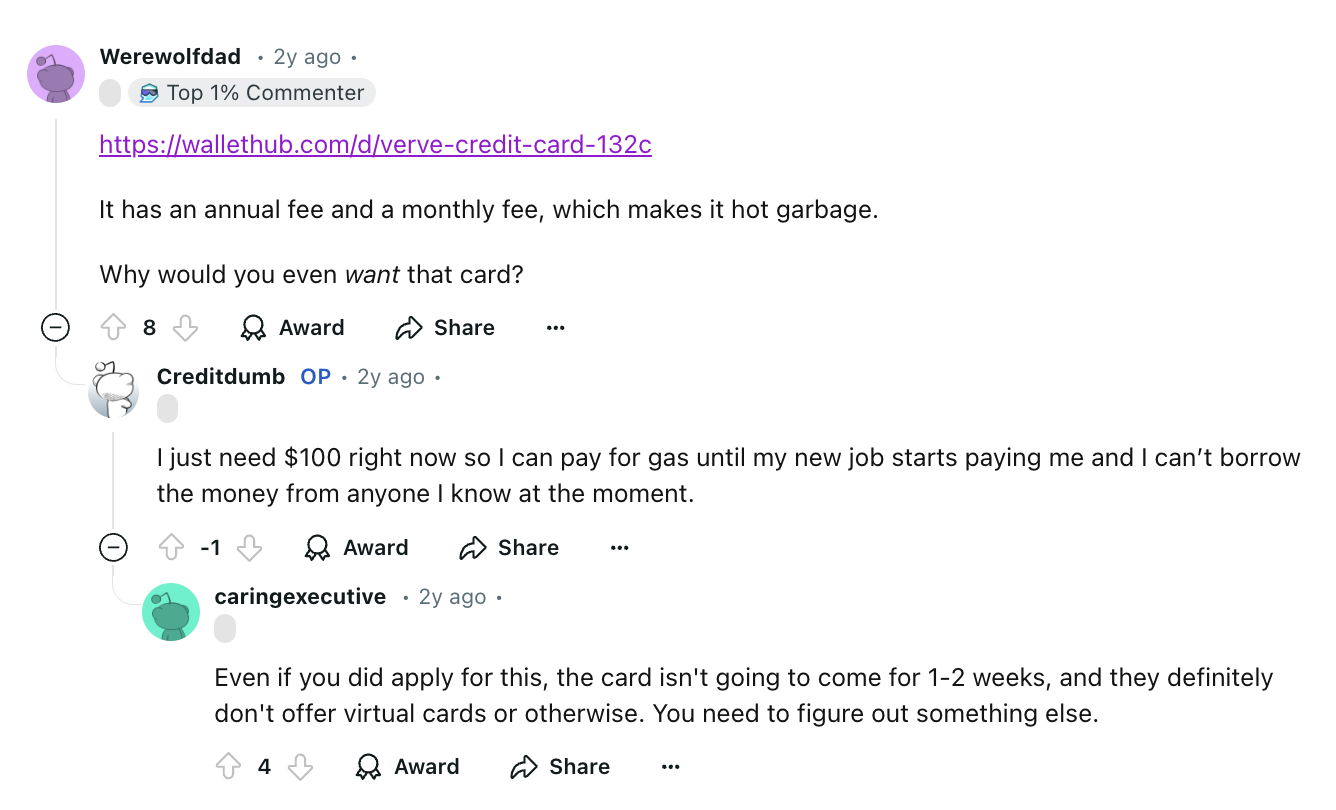

For anonymous reviews and input, I always like to see what Redditors have to say (with the understanding that they can be especially critical over there). As expected, Reddit reviews tend to note the coinciding annual and monthly fees, and say this is “hot garbage.”

Keep in mind that most financial offers get a lot of poor reviews. In most cases, this boils down to people not understanding an offer before they apply.

But, in this case, Continental Finance isn’t known for following the rules. In 2015, the company faced a CFPB order to refund $2.7 million and pay a $250,000 penalty for illegal credit card fees. In 2023, a federal case questioned their arbitration terms, highlighting ongoing legal scrutiny but no recent major penalties reported.

You might also like: A Credit Stacking Breakdown: What it is & How it Works

Frequently Asked Questions

What is the disadvantage of a Verve card?

A key disadvantage is that the Verve card may come with high fees, which can reduce the effective credit limit available to you. And, the card’s interest rates may be higher than those on traditional credit cards, which could make carrying a balance more expensive.

How do I check my Verve credit card balance?

You can check your Verve credit card balance by logging into your online account through the Continental Finance website or mobile app. You can also contact the customer service team using the phone number provided on the back of your card for help.

What bank issues the Verve credit card?

The Verve credit card is issued by The Bank of Missouri, a member of the FDIC, under a license from Mastercard International.

Is Verve credit card for bad credit?

Yes, the Verve credit card is designed for people with less-than-perfect credit. It can be a helpful tool to rebuild or improve your credit, since it reports payment activity to all three major credit bureaus monthly. However, you would need to use it responsibly for a positive impact.

Conclusion: Is Verve a Good Credit Card?

In a word, yeah, the Verve card is a genuine financial tool from an established institution. However, the fees and APR are high, the company offers unclear and deceptive advertising, plus they have a tendency to operate in legally gray areas. So, I’m not comfortable recommending this card as an optimal credit builder…unless you have no other choice and don’t mind paying steep fees.

So, consider all your options and do your research before you commit to any financial offer. With that said, once your credit score is on track, if you’re entrepreneurial, you might be able to get business credit that doesn’t impact your personal credit score.

To learn how to obtain up to $100K in business credit in as few as 30 days, join Business Credit Workshop today.