We work personally with thousands of business owners (and interact with tens of thousands online) to help people build business credit and improve their credit scores so they can obtain substantial lines of credit to grow their companies.

Over the years, we’ve answered and kept records of the top questions people ask when embarking on their business credit-building journey. Today, we’ve decided to share our exclusive insights here, so anyone can access them.

First, we will share the most interesting takeaways from 3,988 surveyed business owners, and explain how we respond to their queries. We’ll answer the top questions entrepreneurs have about business credit. Keep in mind, we always recommend that you consult with an attorney and a CPA before making legal or financial decisions regarding your business.

Here’s your in-depth exploration into the realm of business credit:

Now, let’s dive in!

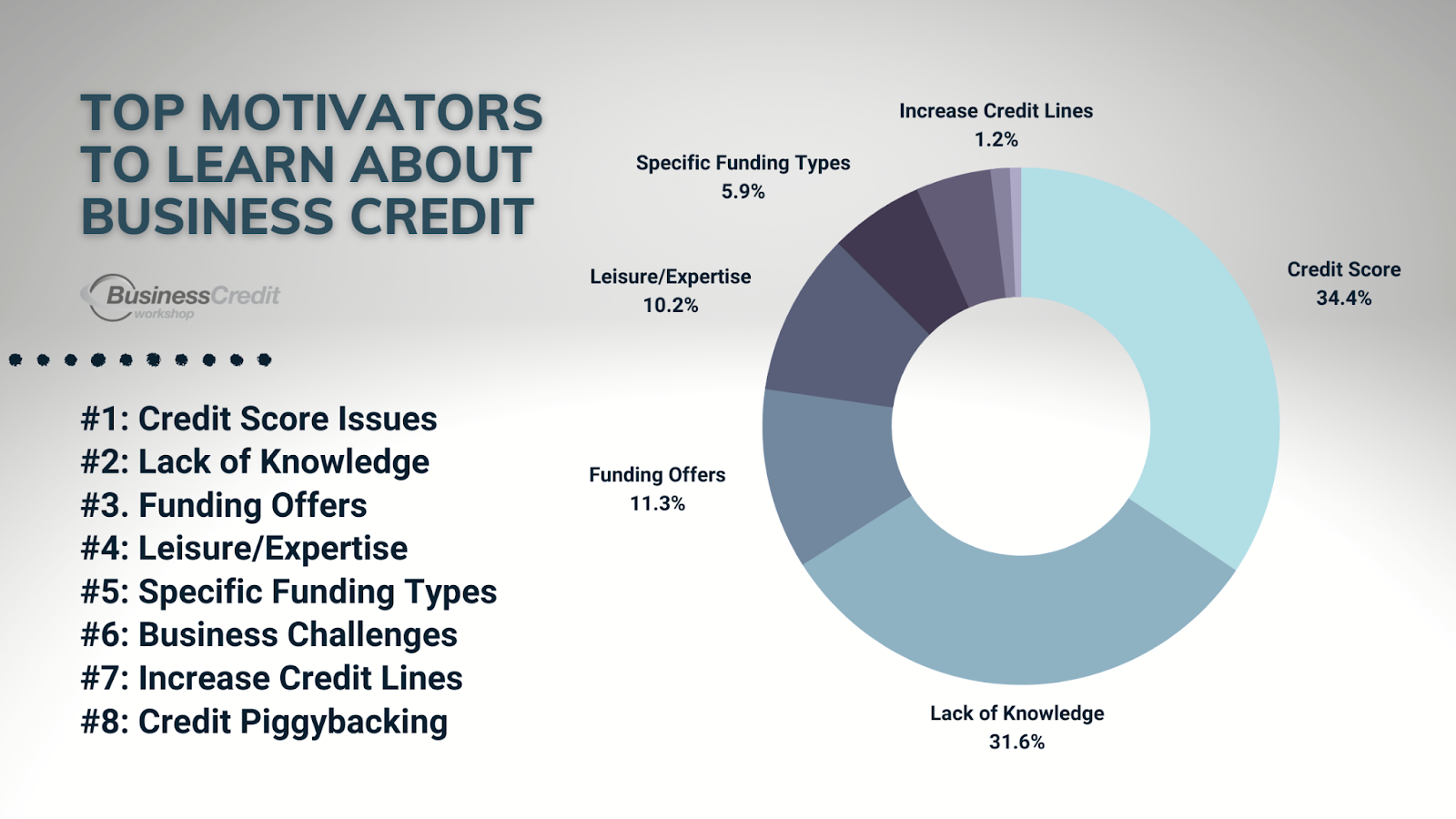

What Motivates People to Seek Out Business Credit Education?

Credit is a crucial factor that lenders, suppliers, and other businesses consider when evaluating a company’s creditworthiness and financial stability. A strong business credit score can help a small business or larger company secure favorable loan terms, negotiate better payment terms with suppliers, and potentially even attract new customers. On the other hand, a poor credit score can make it difficult for a business to secure the funding it needs to operate and grow.

While each situation is unique, business owners have various reasons for seeking business credit education that I’ve broken down into eight categories: credit scores, general business credit knowledge, interest in current offers, curiosity, information about specific funding types, business-related challenges, increasing existing credit lines, and even selling credit.

Here, we examine the top questions people have about business credit, then read answers to those queries.

1. Most Business Owners Need Help With Their Credit Scores

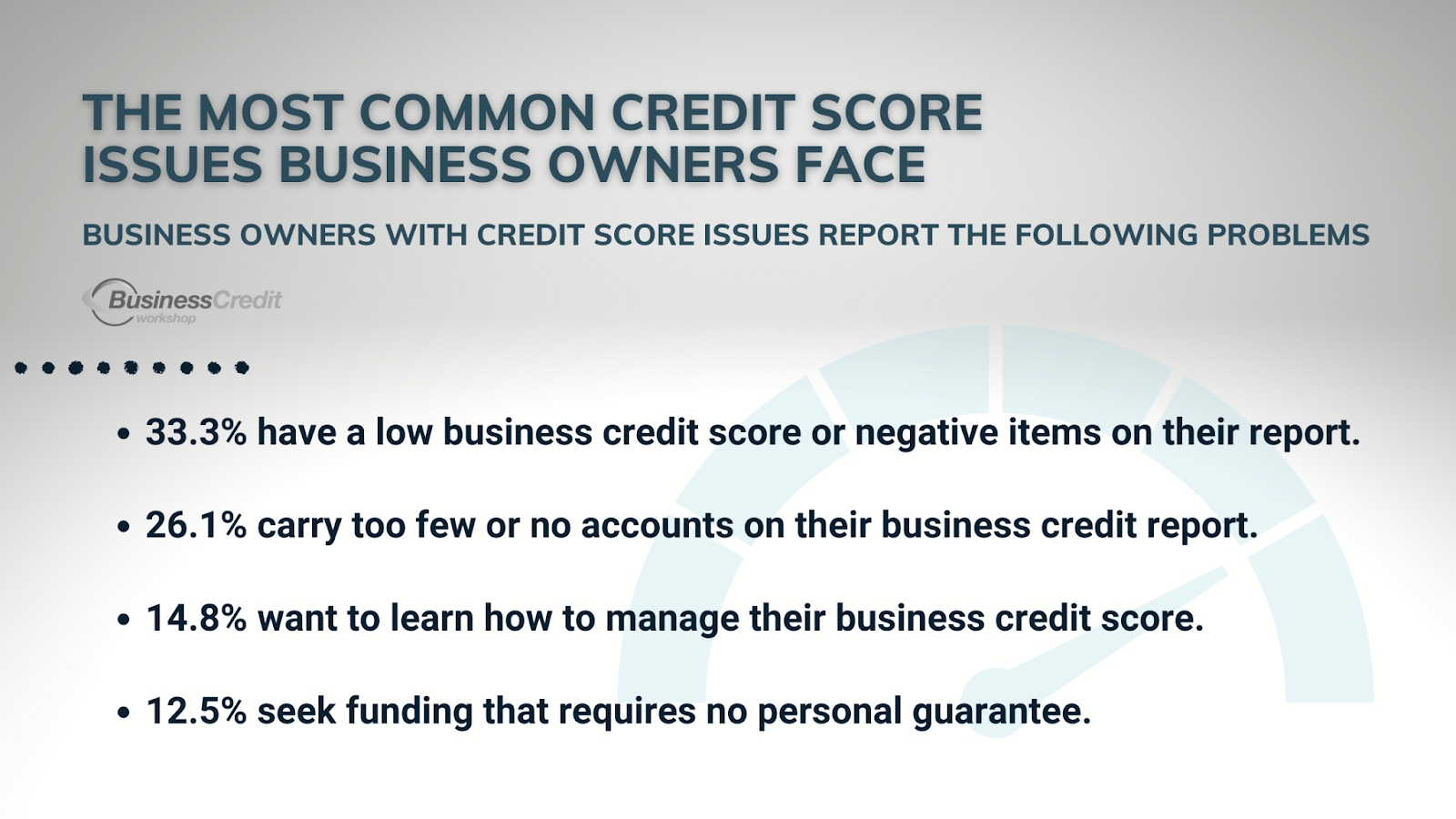

The top reason people come to us is for help with their credit scores. Sometimes this pertains to business credit, while other times there are issues with personal FICO scores. 34.4% of business owners need help with their credit scores when they begin their business credit-building journey. Whether it’s personal or business credit that people need to build or repair, credit score queries are our number one issue. This topic is where we exert most of our energy.

First of all, there are things you can do to improve your credit score:

- Pay your bills on time to prevent negative marks on your report

- Keep your credit utilization below 30% to optimize your credit score

- Don’t open too many new accounts at one time to minimize the negative impact of credit inquiries

- Monitor your credit score so you can catch and dispute errors right away

- Focus on one area at a time, so as not to overwhelm yourself (sometimes, patience is key)

Here are answers to common questions about general credit score issues:

What is the fastest way to fix your credit score?

The quickest way to fix your credit score is to pay off any outstanding debts right away, to make sure that all of your accounts are current. Moreover, you can try to dispute any errors or inaccuracies on your credit report, as these can negatively impact your credit score. I recommend the Credit Secrets system to anyone with a low credit score.

Who can I talk to to help me with my credit score?

For help with your credit score, you can talk to a financial advisor, credit counselor, or credit coach for help with improving your credit score. They can provide you with advice and resources to help you pay off your debts and manage your finances in a way that will positively impact your score. In some circumstances, you may also be able to find free or low-cost credit counseling services through non-profit organizations or your local government.

Can I pay someone to clean up my credit report?

I generally advise against paying someone to “clean up” your credit report. The truth is, companies that offer services like this are generally expensive while the industry is flooded with scammers. If you do decide to pay for a service like this, check with the Better Business Bureau, read company reviews, and do your due diligence before you proceed, as paid credit clean-up is a high-risk solution for poor credit.

Is it easier to qualify for a business credit card?

A business credit card is not easier to qualify for than a personal credit card because it requires that the applicant submit business financial documents, sometimes in addition to personal credit information. However, if they take the right steps, a business may be able to build credit faster than an individual.

Relative to general credit score challenges, a number of people we interact with have problems specifically related to business credit. Of those that need help with their business credit scores, ⅓ of them have an existing, low business credit score or negative items on their report that they want to clean up. These issues need to be handled on a case-by-case basis since there are so many possibilities, and what works for someone with too many inquiries won’t work for someone whose utilization is too high.

In many ways, business credit is similar to personal credit, and some of the same strategies that help boost an individual’s FICO score can help increase a company’s Paydex score and other business credit scores.

Let’s look at the usual queries people have about business credit problems:

How can I fix my business credit score?

To fix your business credit, you can start by paying all bills and debts on time, as agreed. Next, keep your balances low on credit cards and lines of credit. Furthermore, you should regularly review your credit reports for errors. In some cases, it can also be helpful to build a positive credit history by taking out small loans or credit cards and using them responsibly.

How do I remove negative items from my business credit?

To remove negative items from your business credit, you can try disputing the errors with the credit bureaus or negotiating with the creditor to have the item removed in exchange for payment. It is also a good idea to regularly review your credit reports and address any errors or issues as soon as possible. You may also try a goodwill request for the deletion of valid negative marks on your report.

What is a goodwill request for deletion?

A goodwill request for deletion is a letter or email that you can send to a creditor (not a credit bureau), asking them to remove a negative item from your credit report as a gesture of “goodwill.” These requests are typically made when the negative item on your credit report is the result of a one-time mistake or misunderstanding, and you have an otherwise good credit history.

Do goodwill deletion letters work?

Yes, goodwill deletion letters can work to mitigate accurate, negative marks on a credit report, though usually only when the individual or entity making the request has a history of otherwise positive records.

Much of the time, credit score problems are based on a scarce number of accounts on a business credit report. 26.1% of the businesses with credit score issues report too few or no accounts listed on their business credit report. This can occur when the company utilizes tradelines that don’t report to D&B, a new credit line hasn’t been reported yet, or when the business hasn’t applied for credit. Again, these problems need to be resolved on a case-by-case basis.

Having a limited credit history can make it difficult for businesses to establish a strong credit score, which is based on a variety of factors, including payment history, credit utilization, and the length of credit history. If a business has a limited credit history, it is impossible for any credit scoring algorithm to accurately assess a business’s creditworthiness and financial stability.

Here’s what business owners want to know about a limited number of accounts on a business credit report:

How many business credit accounts should I have?

Prior to applying for business funding, you should establish tradeline accounts to establish credit. You first need to set up your business so that it’s optimized for obtaining business credit. To build credit fast, you need a minimum of three tradelines reporting to business credit bureaus, before your score is adequate for lenders; A perfect score requires more.

Can I self-report business credit?

As an individual or entity, you cannot simply report your payments to business credit bureaus. However, there are steps you can take to have certain bills reported. For example, eCredable has options to link utility payments to users’ accounts to have them reported. And, you can apply for certain types of funding that report on-time payments to business credit bureaus.

Why does my business credit card not show on my credit report?

Many business credit cards report on the cardholders’ personal credit reports, not the business credit reports. In a case where you know that your business credit card should be reporting, you may have to wait, as it takes some lenders longer to report than others.

How long does it take business credit to report?

The length of time it takes lenders to send payment activity to business credit bureaus varies from bank to bank. In many cases, it can take over 30 days before payment history shows on a report. Some lenders do not report until after the second billing cycle.

Does Amex report to Dun & Bradstreet?

As a rule, Amex reports all business credit history to the Small Business Financial Exchange (SBFE). Only negative payment activity is reported by Amex to Dun & Bradstreet.

Does Chase report to Dun & Bradstreet?

Yes. Chase does report business credit payment history to Dun & Bradstreet.

In the segment of those whose credit score motivates them to seek more information, 26.1% of business owners express that their personal credit prohibits them from obtaining business credit. From this, I gather that these people are in need of personal credit repair. When a FICO score requires a lot of work, it can take a while to repair it. In the meantime, these individuals might not be quite ready to build business credit.

Nonetheless, we are here to answer everyone’s questions, and try to help them get where they need to be to obtain substantial lines of business credit. Personal credit, after all, can have an impact on business creditworthiness.

See the answers to the most frequently asked questions people have when their personal credit holds them back from obtaining business credit:

Can personal credit affect business credit?

Yes. For most lenders, personal guarantees are required for business loans and business credit cards. This means that your personal credit will usually be considered when you apply for business credit.

Does personal credit affect LLC credit?

Personal credit may impact an LLC’s credit score. On the contrary, an LLC’s credit score will not impact the owner’s personal credit score.

What is the minimum credit score for a small business loan?

Underwriting terms for all banks vary. This means that each bank looks at personal credit scores differently. Still, to obtain business credit, the owner should have a FICO score of at least 640 as a rule.

Do all banks check personal credit for business credit funding?

No. While banks that do not require a personal guarantee for business credit funding are rare, they do exist. With that said, most corporate cards do not require a personal guarantee since they are backed by a business’ revenue as opposed to its credit score.

Of those that come to us with credit score issues, 14.8% of business owners just want to learn how to manage their business credit score. Some business owners need to clean up their personal credit reports, while others want to know how to find and manage their DUNS number or find a business credit monitoring solution.

For these people, we offer education about the major business credit bureaus, credit scores, and credit monitoring tools. While there are a plethora of business credit services out there, we only recommend those that we have vetted and that we know will impact credit decisions from legitimate lenders.

Here are answers to the business credit score management questions we hear most:

What credit bureau is used for business loans?

There are three major business credit bureaus that we recommend business owners keep an eye on: Dun & Bradstreet, Experian Business, Equifax Small Business. CreditSafe, LexisNexis Risk Solutions, and other specialty bureaus are also used by some lenders to determine a company’s creditworthiness.

Where can I check my business credit score?

There are tons of credit monitoring tools available to business owners, the most trusted being Nav. The platform is free to use and helps businesses manage and get more from their financial data.

How do I access my company DUNS number?

Any business can look up their DUNS number by visiting Dun & Bradstreet’s website and searching for their business. For established businesses, the owner can claim an existing profile to access their DUNS number. In some cases, a business owner may need to add their business to the directory to establish a profile.

Is a DUNS number the same as an EIN?

No, a DUNS number is not an EIN. A DUNS number is assigned by Dun & Bradstreet, which is a business credit bureau. An EIN is assigned by the United States Internal Revenue Service (IRS) and is designated for tax purposes.

What is a DUNS number used for?

A DUNS number distinguishes businesses from one another and is used by lenders to look up a company’s PAYDEX score (D&B business credit score). The PAYDEX score is used by lenders to determine a company’s creditworthiness.

Does my LLC have a credit score?

If you have established business credit through tradelines, business loans, or business lines of credit that are reported to business credit bureaus, your LLC likely has a credit score. But, if you have no business credit, your company may not have an established profile with any bureaus.

Relative to personal credit scores, 12.5% of business owners sought funding that requires no personal guarantee (No PG). While such funding is scarce, it does exist. We do our best to help people understand that this type of funding is rare, but that it does exist (and how to get it if they so choose).

It’s very possible — though not always ideal — to obtain loans and credit cards without sharing a social security number. On our blog and in our workshops, we’ve explained how to get business credit with no personal guarantee, which is essentially what this group wants to know.

Most often, people who want to know about “no PG” funding have the following queries:

Can I get a business loan without using my personal credit?

Most business credit is backed by a personal guarantee, which requires you to use your social security number to obtain funding. There are some lenders and loans that do not require personal guarantees, the most common type of funding being merchant cash advances (these usually come with excessively high interest rates).

Can I use my EIN to get a credit card?

In most cases, business credit cards and lines of credit require a personal guarantee, which means that, even if you apply using an EIN, your social security number is also required. With that said, yes, there are ways that you can obtain credit with just an EIN.

Can I use my EIN to get a loan?

As with credit cards, most lenders require a personal guarantee. In this case, even with an EIN, you will still need to share your social security number. But, in limited scenarios, you can get a loan with just an EIN.

2. Many People Have a General Lack of Business Credit Knowledge

After those with credit score issues, the next most common reason people come to us is that they simply don’t have a strong understanding of business credit. We help people who want to move into the first phase of building business credit, those who have no idea what they need, others who want to know why they’re getting rejections, and even some who want to learn so they can help others.

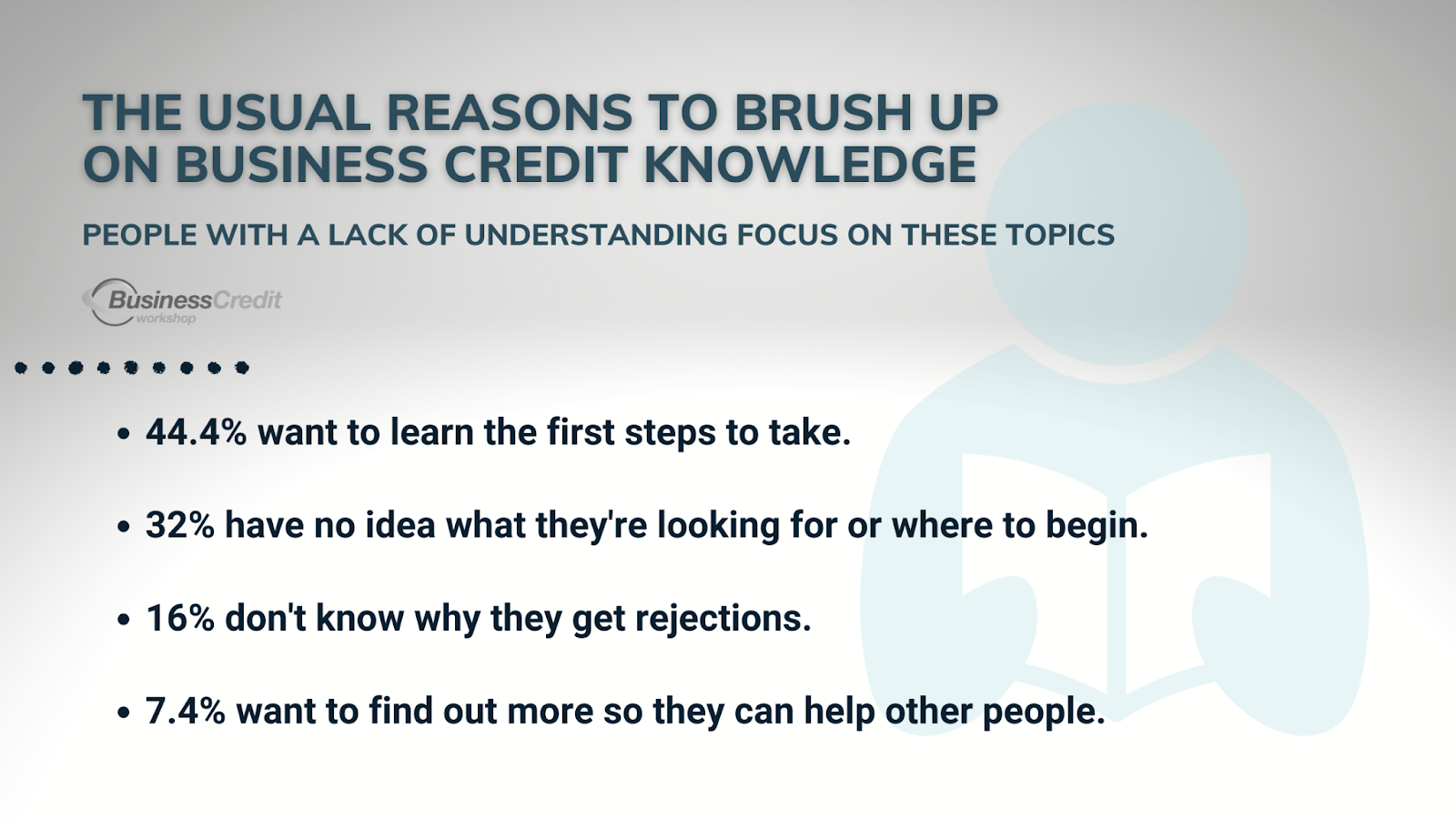

31.6% of business people have a general lack of business credit knowledge that drives their decision to learn about the subject. In a nutshell, our core offer is business credit education. Those with a lack of understanding are in the right place when they stumble onto our materials. Some of them want to know why they keep getting denied, how to qualify for substantial credit lines, or just want to learn as much as they can so they can help others.

We have a five-step process that is especially helpful for this group:

- Form your company in a way that optimizes your business credit potential

- Take the steps to get your company “business credit-ready”

- Network with local banks to understand underwriting requirements

- Set up your business credit profiles with the three main bureaus

- Build your first, small tradelines (lines of credit) to officially establish your credit score

Our advanced process is available to business credit workshop coaching students.

From this segment, here are the top questions we’ve been asked:

How do I obtain business credit as a beginner?

The very first step you must take to obtain business credit is to establish a business in a way that it is likely to be worthy of business credit: Choose a neutral name and business category. The same company name over a long period shows dependability. You can get your articles of organization from your Secretary of State.

How do you explain business credit?

Business credit is your company’s ability to borrow from banks and other lenders. In most cases, your business credit score is central to a bank’s perception of your company’s creditworthiness.

What can I use business credit for?

You can use business credit for almost anything you need to grow and scale your company. Business credit can be used to replace or repair equipment, make investments, and pay vendors or utilities. You can even use business credit to pay rent.

Does my EIN have a credit score?

In a word, no. An EIN assignment does not automatically establish a business in any credit bureau databases. However, there are credit scores attached to EINs separately from SSNs.

Why is my business credit card on my personal credit report?

If your SSN was used to obtain a credit card, then it will report to consumer credit bureaus. The same credit card may or may not report to business credit bureaus.

Will a business credit card build my credit score?

With responsible payment history, a business credit card can serve to boost a business credit score. However, aside from secured credit accounts, most business credit cards require some sort of credit history before a company is considered creditworthy.

Should I pay off my business credit card in full?

Paying off your business credit card in full each billing cycle will help you avoid interest accrual. In most cases, yes, this would be beneficial and the cost of using the card would be less.

Most of those who with a lack of business credit knowledge just want to know where to start. 44.4% of business owners with a lack of knowledge specifically seek how to establish business credit or want to know the first steps of the process. Once they get the early training, many of them are surprised that the way they establish their business itself plays a major role in obtaining business credit. Sometimes, people need to make changes to their business structure through their state or establish a new business.

In a nutshell, you need to incorporate your business, establish an EIN, register with the right state and local government agencies, and open a business bank account before you can move on to what people tend to think of as the early steps.

For those who want to learn how to navigate the early stage of establishing business credit, here are the most common questions we answer:

How long do you have to have an LLC to get business credit?

Banks look at your time in business to determine creditworthiness, but not all banks are the same. Since some lenders will extend credit to new businesses when they can show a certain amount of revenue. To determine your odds of qualifying for credit, check the bank’s underwriter for the time in business requirements.

Do you need an EIN to build business credit?

Yes. To obtain business credit that is based on your business credit score, your company must have an EIN.

What is an EIN?

An EIN is a nine-digit employer identification number, assigned by the IRS that acts as a tax ID for a business. An EIN is required to establish a business bank account.

How do I find my EIN?

Your business is not automatically assigned an EIN when it is established. You need to apply for an EIN with the IRS. Note: if you accidentally apply for a state tax ID instead of an EIN, and you do not have employees, your state may send undue tax invoices throughout the year. So, be sure to apply for your EIN on the IRS website.

Of those who lack business credit knowledge, many of them are clueless when they begin. 32% of individuals don’t know where to begin or what they’re looking for. For this group, I lay out the basics of building credit. Again, this involves establishing your business the right way. Before we explore that, this group requires a more fundamental understanding.

In general, these people are asking broad questions, which usually requires that we start asking questions about their business so that we can steer them in the right direction. For the most part, this group is the most eager to learn.

Here are the questions we hear most from those who don’t know where to begin:

How do small business owners build credit?

First, small business owners looking to build credit should establish their business in such a way that their company is likely to be considered creditworthy. They then need to network with local banks to learn about business credit requirements and establish an EIN and a business bank account. Finally, they must establish their first tradelines or net 30 accounts.

What is the minimum business credit score?

Business credit scores range from 0 to 100. Most business credit lenders require a minimum business credit score of 70 to deem a company creditworthy.

What should I look for when building business credit?

Depending on whether or not your business is properly established to obtain business credit, you may need to look at your business structure and whether or not your company name and category are neutral. Next, you should research the underwriting requirements of the banks you would like to obtain funding from.

From the group with little business credit understanding, some of them need to understand what factors lead to business credit denials from banks. 16% of people who cite a lack of business credit knowledge have no idea why they get rejections from lenders. This fact reinforces the significance of learning as much as you can about business credit before applying for new credit lines.

There are a variety of reasons that a business might be denied credit. A lack of credit history, poor credit history, insufficient collateral or income, and excessive debt might lead to the inability to obtain business credit.

Here’s what this group tends to ask, and how we generally respond:

Why do I keep getting denied business credit?

Requirements for any type of credit vary from lender to lender. You might be denied business credit when you have a poor credit history or a low personal or business credit score, not enough collateral or revenue, a lack of time in business, or limited financial resources among other things.

How many times can you apply for business credit?

There is no set limit to the number of times you can apply for business credit. With that said, hard inquiries on your credit report can have a negative, albeit temporary impact on your personal and/or business credit score. So, too many applications in a short timeframe can damage your capacity to qualify for business credit.

How long after being refused business credit can I reapply?

There is no set limit to the time you should wait before reapplying for business credit. However, you should take enough time to find out why you were denied, assess your creditworthiness, and remedy any issues with your credit before you file a consecutive business credit application.

Does it hurt your business credit score if you are denied a line of credit?

A turndown for funding is not damaging to your business credit score, but a hard inquiry for business credit can lead to a slight, temporary decline in your credit score. Depending on which credit reports are pulled during the application process, applying can affect your personal and business credit scores.

What rights do you have when you are denied credit?

When you are denied a line of credit, you have the right to receive a notice of the action taken, to request a free copy of your credit report that was provided to the lender, to dispute incorrect information, and to file a complaint with the Consumer Financial Protection Bureau (CFPB).

Maybe the most intriguing statistic from these findings — for me anyway — is the fact that 7.4% of people seeking business credit knowledge want it so that they can help others. Some of them even cited spiritual reasons for learning more about the topic. While I have always genuinely been driven to help others by teaching business credit topics, before these instances I had never considered the opportunities might be considered sacred to some people.

The group that wants to learn so they can help people is highly inquisitive and asks questions all over the board. They tend to ask almost every query on this page, and we love it!

3. More Than One Out of Ten Want to Locate Business Credit Offers

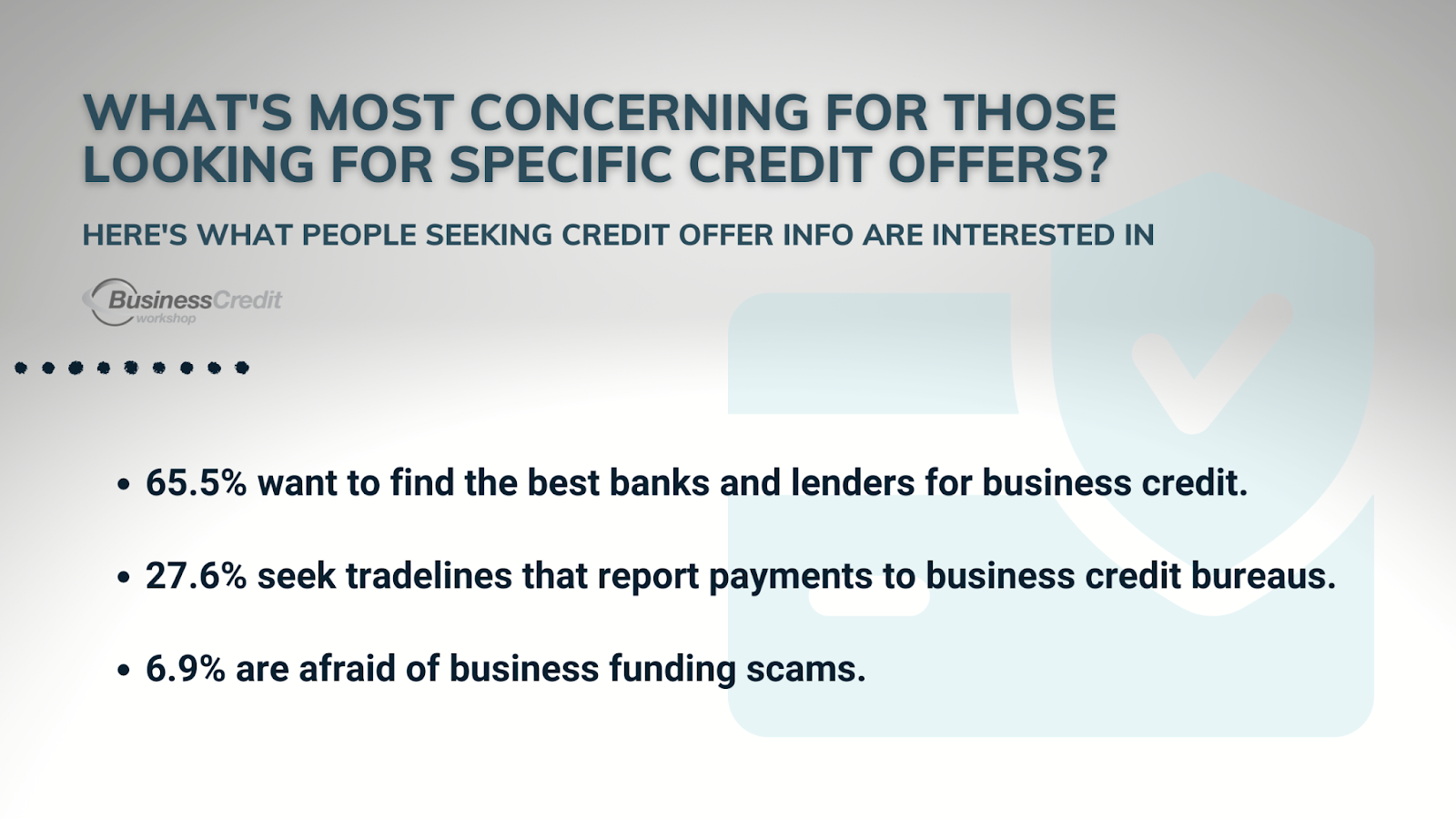

Many people want to stay in the loop about legitimate banks and lenders, tradelines that report to business credit bureaus, and weed out scammers. 11.3% of business leaders want to know more about the business credit offers that are currently available. Though not the majority, there are many people who come to me because they want to know more about banks and lenders that offer the right of financing for their needs. More than one out of ten people who come to Business Credit Workshop are interested in learning about specific business credit offers!

The most common general questions about business credit offers are below:

What is the best business credit card?

The “best” credit card for a business depends on the company’s financial status, its credit standing, and its funding goals. We don’t have a favorite business credit card, but the offer that we most often refer business owners to is Divvy.

What bank is best for a business account?

In general, for a business bank account, we recommend business owners research local community banks and credit unions to see what offers are available for business. This way, they can determine which is best suited to their needs. We continually review banks and business credit offers on our website and YouTube channel to try to keep people informed.

What is the best credit union for a small business?

We recommend that business owners first turn to their local community banks and credit unions when starting on the business credit-building journey. We do have a list of our favorite nationwide credit unions that we sometimes refer people to.

While anyone can do the research online to see relevant offers for their business, it’s not always easy to find, especially when you don’t know exactly what you’re looking for. Of the business leaders who want to find out about specific offers, 65.5% are looking to find out which lenders and banks offer the best funding options. We regularly cover the most popular business credit offers on our blog and our YouTube channel.

One-on-one, here are the top questions people ask us about banks and funding options:

What bank has the best business credit offers?

Of course, offers from Amex, Discover, Chase, and the like are legitimate. Most major banks have a plethora of business credit offers. However, we recommend a local community bank or credit union for the highest business credit limits and best interest rates — this is the core of what we teach.

Is it better for a business to bank with a credit union?

While it’s impossible to answer this question for every possible scenario, at Business Credit Workshop, we do typically recommend small community banks and credit unions over traditional, big banks for small business owners.

What is the safest bank to do business with?

Most banks in the United States are FDIC insured, which covers deposits, dollar-for-dollar, and any accrued interest. So, they’re pretty safe. One bank that comes up (a lot) as a servicer for some of our favorite business credit offers is Celtic Bank. And, we often recommend people look into offers from Navy Federal Credit Union.

Is Chase a good bank for a small business?

For business owners who want a traditional offer from a big bank, yes, Chase has a full suite of options for business owners. They provide robust online banking features, credit cards, loans, and lines of credit. But, our general advice is to check with local credit unions and community banks to learn what’s available for small businesses.

One of the early steps to building business credit is to establish tradelines that report on-time payments to business credit bureaus. Without net 30 vendors and gas cards, the path to a substantial business credit line is long and difficult. 27.6% of entrepreneurs in this group are seeking a list of vendors or tradelines to establish their reporting accounts. We cover tradelines all the time on our blog and YouTube channel and share a list of 30+ reporting vendors to Business Credit Workshop participants.

The following tradeline-related questions are commonplace:

What is the best tradeline for a small business building credit?

You should choose a tradeline that offers something you actually need and reports payment history to business credit bureaus. A couple of vendors that we often recommend are Summa Office Supplies and Crown Office Supplies, though many others also report.

How many tradelines do I need to build business credit?

After your business credit profiles are established, you should have a minimum of three tradelines reporting, and more for a perfect business credit score (which you need to obtain substantial credit lines).

Which net 30 vendors report to business credit bureaus?

Quill, Lowe’s, Uline, and SupplyWorks are just a few of the many net 30 vendors that report on-time payments to business credit vendors. Business fuel cards can also be a great option for business credit.

What is the easiest business gas card to get?

Business fuel cards are not difficult to get, because they typically have net terms (you pay in full as you spend). This means that a credit score is not required to obtain a card. Most recently, we reviewed AtoB’s gas card offer, and we pretty much love it.

With so many ads coming at us from all directions, it’s smart to be aware of fraud. I was not at all surprised to learn that fear of scammers kept 6.9% of these business owners from applying for business funding. People want to know that they’re not being scammed before they sign up for an offer, especially when it involves their business.

Here’s what people want to know about business funding scams:

How do you know if something is a financial scam?

Most of the time, if something seems too good to be true, it is. If a so-called business pressures you to make a decision quickly, this is a huge red flag. And, in most cases, a legitimate financial offer won’t require money upfront to apply. Before you sign up for any offer, do your due diligence: read reviews and make sure funding offers are upfront about the banks backing them.

Can you get money back from a fraudulent funding offer?

If you can catch the scammer, you may be able to get your money back. But, in most cases, fake funding offers are gone before you know what hit you. If you use your credit card or debit card to pay for any upfront fees, the bank may be able to help you recover what you’ve lost.

Is business credit a real thing?

Yes! Business credit is real, and it doesn’t impact your personal credit. In general, business lines of credit are typically larger than personal lines of credit, and you can build business credit in as few as 30 days.

4. Plenty of Entrepreneurs Simply Enjoy Honing Their Expertise

Of the thousands of people who came to us to learn about business credit education, hundreds were just learning for leisure or to sharpen their mastery. 10.2% of small business entrepreneurs reported that they enjoy brushing up on the subject of business credit. Some of the people who were casually learning are credit repair specialists (of course, not all of them told us so). Whether they had no problems or just wanted to make sure they were up-to-date, they signed on to find out just what we were teaching — their questions were mostly procedural and unrelated to what we teach.

Of the leisurely learners, 76.9% of people in this segment cited no problems with or questions about business credit. I gather that they were either just learning for leisure, or they were researching for a personal or professional project. As you might guess, they weren’t super inquisitive about the process.

However, they weren’t the only ones enjoying themselves while learning, and the other portion of this segment wasn’t so quiet. 23.1% of the business owners in this group admitted that they already knew about business credit, but were updating their understanding. And, they wanted to ask about …

Here are the queries we heard most from those who wanted the skinny on modern business credit concepts:

What’s the fastest way to build credit for an LLC?

The fastest tactic for building business credit, after your business is established in an optimal way, is to use tradelines and gas cards that report to business credit cards. Of course, you need to pay these accounts as agreed to avoid negative marks on your business credit report.

How can I get a business credit card for a new business?

The first step is to establish your business the right way. There are many factors that contribute to a company’s creditworthiness. Many people who obtained business credit on behalf a prior, established company don’t realize that, in the past, their tradelines reported to business credit bureaus, which boosted their business credit score.

Should I use my SSN for business credit?

Most business credit cards are backed by a personal guarantee (PG), so yes, it’s most likely that you will include your social security number in a business credit application. However, no PG business credit lines do exist.

What gas card can I get with a 600 credit score?

You can get most gas cards with a 600 credit score. In fact, fuel cards usually come with net terms, which means that you pay in full each billing cycle. So, most of these offers are not based on FICO scores at all.

What credit score do you need to get a gas card for your business?

You do not need a certain credit score to qualify for a gas card. Because most gas cards have net terms, you pay in full each billing cycle. The credit lines for a fuel card are based on income, not credit scores — increased spending limits are usually offered over time.

5. Some Business Owners Want Help Obtaining Specific Types of Funding

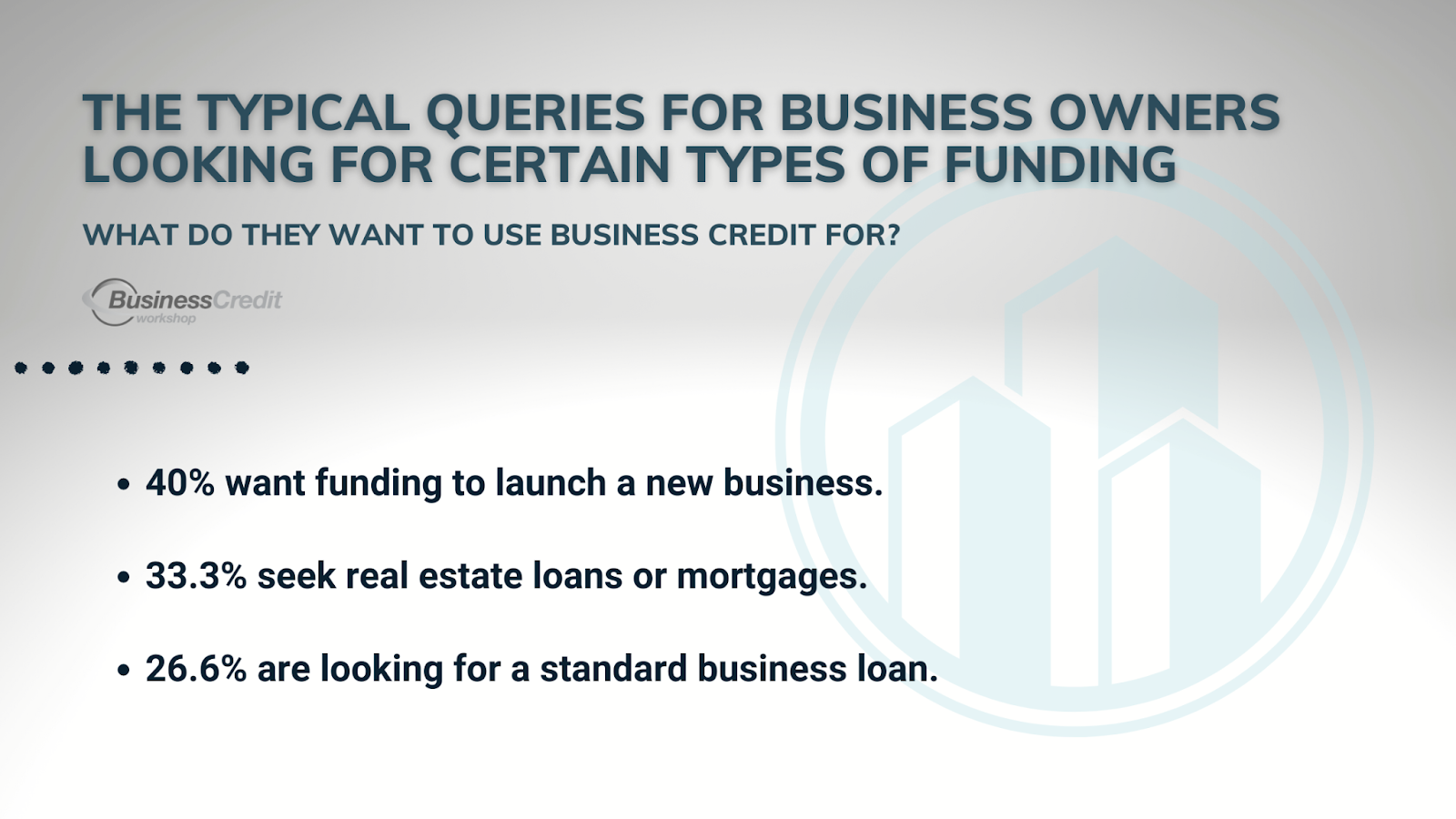

While they’re not the majority, there are quite a few people who ask us about funding for specific uses. 5.9% of business owners want to learn how to find and obtain a specific type of business credit or funding. They might ask about startup funds, real estate loans & mortgages, or business loans.

In general, here’s how we address this group’s top issues:

Can I get a business loan without business credit?

There are types of funding that business owners can get using their personal credit. And, there are income-based business lines of credit. Aside from corporate cards, however, business funding for a company with no credit score tends to come with high-interest rates.

What are the main types of credit businesses can get?

Businesses can obtain secured and unsecured credit cards, term loans, SBA loans, equipment loans, corporate cards, mortgages & real estate lines of credit, gas cards, as well as invoice factoring & merchant cash advances (not recommended).

Within this segment, most often, individuals seek startup funds. In most cases, they’re looking for a way to fund and launch a new business idea. In fact, 40% of individuals looking for a specific type of business funding want startup funds. Some of them are under the wrong impression — they tend to think that there might be a way to get funding with no revenue or positive credit history to back it. This group benefits tremendously from learning the fundamentals.

Here’s what they ask:

How much can I get for a startup business loan?

That number ranges from $0 to $500K but depends on what you have to prove your creditworthiness. In a nutshell, you need a credit score and some proof of your ability to repay the funds. We teach businesses how to obtain up to $100K in business credit, which they can use as startup funds or for any other business purpose.

How do I get startup credit for my business?

The first step is to incorporate your business. Next, you must apply for an EIN and set up business banking. You’ll need to get your business set up in such a way that it appears trustworthy to lenders and open a business credit file. Then, you need to establish a number of tradelines that report on-time payments to business credit bureaus.

What is your business credit score when you first start?

If you have not established any tradelines, your business credit score starts at zero.

Is business credit better than private funding?

Many people would say that they prefer business credit over VC and private equity funding because they do not want investors in control of their business operations. Others would prefer private capital because they are interested in expert guidance, and eventually exiting their business for a profit.

Of those who seek a specific type of funding, 33.3% want business real estate loans or mortgages. While we don’t focus a ton on mortgage options, we do share what we know — We share information about various commercial mortgages and the BRRRR method of real estate investing, as well as alternative options for purchasing homes and real estate.

These are the questions we most commonly answer:

What is a mortgage for a business called?

A business mortgage is called a commercial mortgage. Another type of funding that businesses can consider when purchasing property is a real estate investor line of credit. In some cases, business owners have paid for homes with credit cards or revolving lines of credit.

Can a business get a 30-year mortgage?

Business property loans typically have 7-20 year terms rather than 30. And, the amortization period for a commercial mortgage can last up to 30 years, which means that payments may still be required after the terms are up.

Are business mortgages cheaper?

As a rule, no. The APR is typically higher on a business mortgage than on a consumer mortgage. However, businesses have some funding options that are not available to individuals.

Of the group looking for a specific type of funding when they come to us, 26.6% want a business loan. These people are pretty quick to the gun, ready to do what they need to get funding.

Most often, here are their queries:

What do I need to get a business loan?

You’ll need a business that has been established properly, an EIN, good personal and business credit, a number of tradelines reporting on your business credit report, substantial business revenue (this will vary based on the credit line you want), and documentation to provide lenders.

What is the minimum income for a business loan?

There is no minimum income required for a business loan because offers vary from lender to lender. For a smaller line of credit, $5K or less monthly income may suffice. For larger business loans, there may be higher income requirements, but there are banks with underwriting requirements that are easier to meet.

What is the best loan for a business?

The best loan for a business can vary tremendously based on the company’s needs. We often share in-depth reviews for popular and recommended business loans and credit cards after learning more about an individual’s goals and requirements.

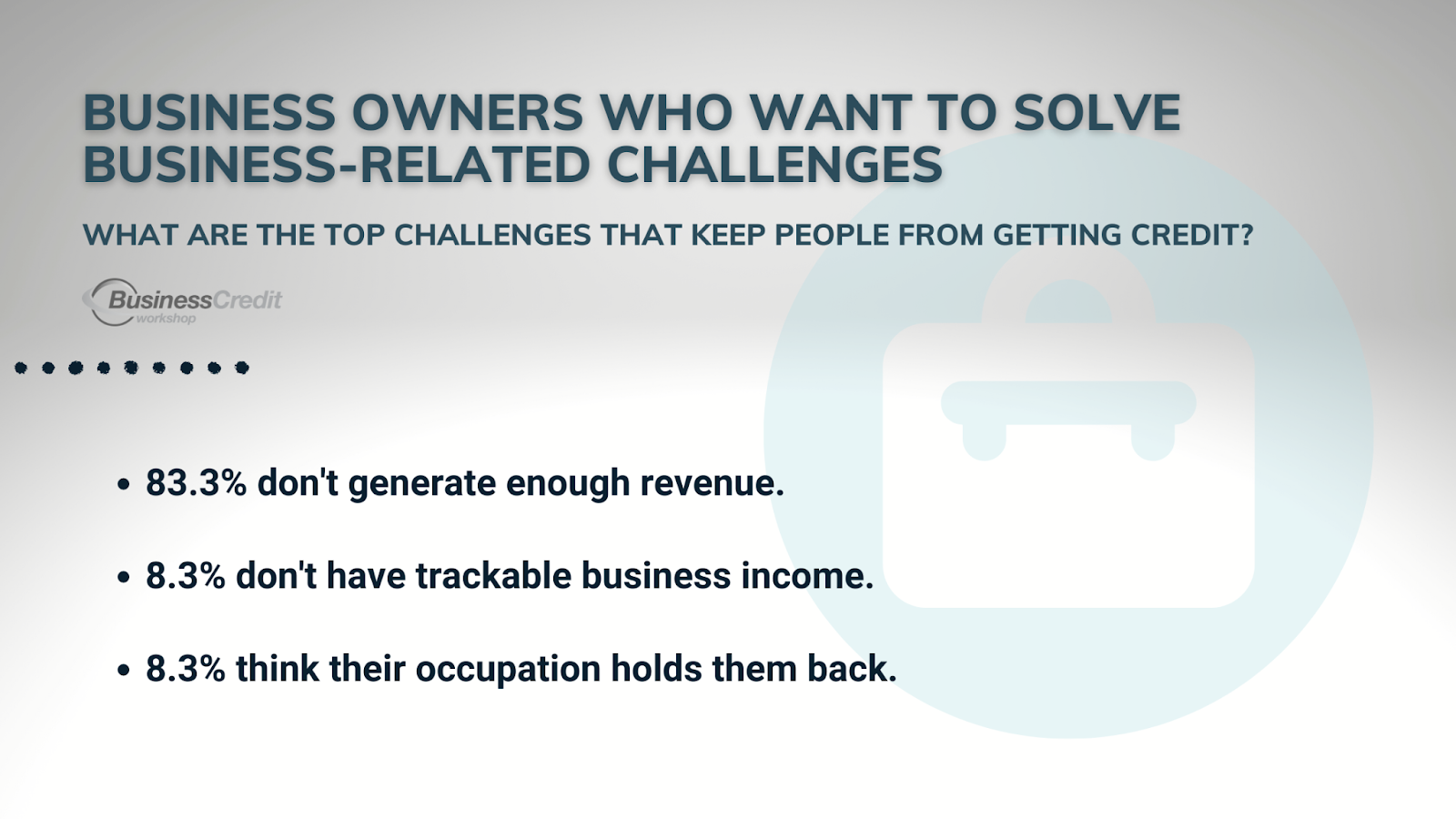

6. Numerous People Want Business Credit to Solve Work-Related Challenges

Whether it’s their occupation or industry, the fact that they run a cash business, or a lack of revenue, 4.7% of business owners have a business-related challenge they need to learn how to overcome when they seek out business credit knowledge. Establishing business credit can give this group a way to access financing, secure loans, and get better terms on credit offers. The funds that they obtain can then help them grow their business.

In general, we answer the following for this segment:

How can I use credit to grow my business?

Once you establish a strong credit profile, you can obtain substantial credit lines. If you use your funding responsibly, you can make investments that improve your profitability.

How fast does business credit grow?

If you make all the right moves, you can have an established business credit profile with an excellent credit score in as little as one billing cycle, or as soon as your accounts are reported to business credit bureaus.

In the group with work-related challenges, 83.3% of business owners say that they don’t generate enough revenue. They might be looking for an income-generating investment: equipment, staff, advertising, you name it. And, those who are serious about implementing our training can find new ways to boost profits.

Here’s what they tend to ask us:

How do you use credit to generate income?

You can leverage your credit to make investments that are profitable. It’s as simple as that. Some people invest in inventory, real property, or business equipment. Others might opt for something less tangible like digital assets. Though, all investments come with some risk. If you do use your credit to generate income, always be sure that your profit is higher than your account interest and fees.

Can I use a credit card to invest?

Yes. Technically, you can use a credit card to invest in stocks or bonds. When you use credit for investing, it’s probably smarter to look at assets with less risk like business equipment, advertising, or retail inventory.

Does credit funding count as income?

No. Credit funding is debt. It does not count as income and can not be taxed as such.

Can you use a credit card to invest in Bitcoin?

Yes, some of the bigger crypto exchanges allow users to invest using credit cards. Though, we don’t generally advise beyond that on the crypto market or investments in general.

Another work-related problem is that 8.3% believe that their cash business is holding them back from obtaining business credit. It’s actually pretty common for a company to do business using cash. Luckily, this problem has a simple solution (as long as you’re not trying to hide your money from the mafia). Really, you just need to use your bank account.

This is what we most often address with this crowd:

Can I get a business credit card with a cash business?

Yes, you can obtain business credit, even if your income is cash. However, you will need to first make sure that your business is legally established and “credit-ready.” And, you will most likely need to have your money in a business bank account.

Can I get a business credit card with no money in the bank?

In most cases, no. You can not get a business credit card without traceable money. If you are going to apply for business credit, you will need money in a business bank account.

What business funding can I get with a cash-only business?

If you run a cash business, and you refuse to keep all of your money in a business bank account, your funding options will likely be limited to bootstrapping (owner-funding), private investing, and crowdfunding.

Akin to undocumented revenue, another 8.3% say that they believe their occupation or industry keeps them from being able to obtain credit. For example, freelancers and independent contractors have had a particularly hard time, and attribute their type of work to their inability to get funding. The truth is that any business can get funded — they just need to establish their company properly.

For the most part, here’s what this group is asking:

Can I get a business credit card with a 1099?

Yes, you can get a business credit card, even if all of your income is from contract work. To do so, you will need to establish your business properly and account for your financials in a way that makes you appear creditworthy to lenders.

Can I get a business credit card if I am self-employed?

Yes. Self-employed businesses are no less creditworthy than businesses with employees. As with all businesses, you will first need to establish your business properly and get it “credit ready” before you can obtain funding.

Can freelancers get business credit cards?

Yes. Freelancers are self-employed businesses. The thing is, you just need to have your ducks in a row before you apply: Incorporate your business and get it “credit ready.”

Can I get a loan being an independent contractor?

Yes. Independent contractors can get business credit, as long as they set the proper foundation. You will need to incorporate your business, get an EIN and business bank account, and establish your business profiles before anything else.

7. Those Who Want to Increase Their Existing Credit Lines Are a Minority

While not the smallest group, there are not many people who want to grow business credit lines that they’ve already obtained. Only 1.2% of business leaders who seek business credit education want to increase their existing credit lines. Looking at this, I think it’s safe to assume that most people who already have business lines of credit are not super likely to be actively learning about the topic. But, they do have some specific inquiries.

Here, you have the typical questions that this group asks:

How can I get my line of credit increased?

Credit card issuers ultimately want to earn profit from credit card interest. When a cardholder shows that they make payments on time, as agreed, this can lead to an increased credit line. However, making minimum monthly payments is usually insufficient. Paying an account in full while the card is still in regular use is sometimes the fastest way to show worthiness for a credit limit increase.

Why is it so hard to get a credit line increased?

The final determination for a credit limit increase, for any bank, is based on the profitability forecast for the account. Most banks have private underwriting terms, which makes it difficult for many people to determine what will make their account eligible for an increased spending limit.

Will requesting an increase in credit line harm my business credit?

Some banks may conduct a hard pull to your personal or business credit report when you request a credit limit increase. While a hard inquiry does impact your account, the impact is typically low and is always temporary.

When should you ask for a credit line increase?

The best time to request a credit line increase is when you actually need it. But, you should consider your payment history over the past few months, and be sure that your account usage is not nearing your existing credit limit when you do so.

What’s a good credit limit on a business loan?

We often see business term loans in the amount of $20K-100K. The best amount would be whatever you need to grow your business and ultimately improve profitability.

Does canceling a business credit card hurt your credit score?

If you cancel a business credit card, it would decrease your credit limit; this could increase your utilization. You should try to keep your total credit utilization below 30% to optimize your credit score.

8. A Handful of People Are Curious About “Credit Piggybacking”

When they first come to us, 0.7% of small business entrepreneurs are interested in learning how to earn money by allowing others to “piggyback” on their credit. This is the smallest group. And, honestly, I was taken aback when the first person came to us looking to sell business credit since this isn’t a service that we offer. Still, I take everyone’s interests into account. In fact, I reviewed one of the most highly-rated tradeline brokers some time back.

Note: I try not to censor anything I share with Business Credit Workshop readers and coaching students (even when it is controversial). While I don’t endorse tradeline brokering, I have several coaching students who partake in the practice, and I see even more in the online groups I’m part of. Tradeline brokerages can absolutely be legitimate businesses, and — although there are considerable risks — there is potential to earn money for those with an abundance of credit.

So, here’s the skinny on the credit piggybacking questions we most often hear:

Is piggybacking credit legal?

Yes, adding an authorized user to a credit account is legal. Though, it is meant for family and close associates who actually intend to share an account. Many lenders prohibit cardholders from adding strangers to their accounts or using tradeline brokers.

Does adding someone as an authorized user hurt my credit?

No, adding a new user to a credit account does not harm your credit score. However, if the authorized user uses the account irresponsibly, it can negatively impact your credit.

Can piggybacking hurt credit?

Yes, adding an authorized user to an account can hurt credit if the authorized user uses the credit card or line of credit irresponsibly. Simply adding multiple users has no negative impact on a credit score.

What are the disadvantages of credit piggybacking?

Credit piggybacking, as advertised through tradeline brokers may be prohibited by your lender. This means that if the lender found out that you participated, they might close your account. Another risk is that an authorized user who has access to your line of credit may spend irresponsibly, which has the potential to ruin your credit.

What is a tradeline broker?

A tradeline broker is a middleman between a credit account holder and a client who wants to “buy” (more appropriately, “rent”) an account, or be added as an authorized user. Clients are willing to pay for the chance to temporarily show an increased credit line prior to applying for a mortgage or other high-limit financing.

How much can I sell my tradeline for?

Depending on which tradeline broker you were to go with, you could earn from $50 to $2K per month to participate in credit piggybacking.

Final Takeaway

There are several motivations that drive people to seek out education on business credit. The most common reason is the need for help with their credit scores. Many people also have a general lack of knowledge about business credit, and more than one in ten are interested in locating specific business credit offers.

Moreover, some entrepreneurs enjoy learning more about various financial topics, while others want help obtaining specific types of funding or want to use business credit to solve business-related challenges. A small minority of business owners are interested in increasing their existing credit lines, and a handful of people are curious about “credit piggybacking.”

We have assisted thousands of business owners in building business credit and improving their credit scores, enabling them to obtain lines of credit to grow their companies. This post contains the top questions asked by entrepreneurs about business credit. These are our exclusive insights and responses to these queries based on our experiences working with these business owners.

Do you want to learn how to obtain up to $100K in business credit in as few as 30 days? If so, join Business Credit Workshop today.