Fix and flip or “flipping houses” involves buying properties, renovating them, and selling them quickly for a profit. It’s an exciting way to invest in real estate and offers the potential for significant profits. But, the right financing is crucial.

Thinking about diving into the flipping market? Here, I want to walk you through everything you need to know about fix and flip loans so you can make informed decisions and boost your investment potential.

This is what’s in store:

- What Are Fix and Flip Loans?

- How Fix & Flip Loans Work

- Types of Fix & Flip Loans to Consider

- This is How to Qualify for a Fix & Flip Loan

- Common Alternatives to Fix and Flip Loans

- Frequently Asked Questions

- Conclusion

Now, let’s dive in!

What Are Fix and Flip Loans?

Fix and flip loans are short-term financing options designed for investors looking to buy, renovate, and sell properties quickly. Unlike traditional mortgages, these loans focus more on the property’s potential value after renovations rather than your credit history. They typically have higher interest rates and shorter repayment terms but provide fast access to capital—exactly what you need when timing is critical.

Understanding the various funding types can help you choose the best option for your needs.

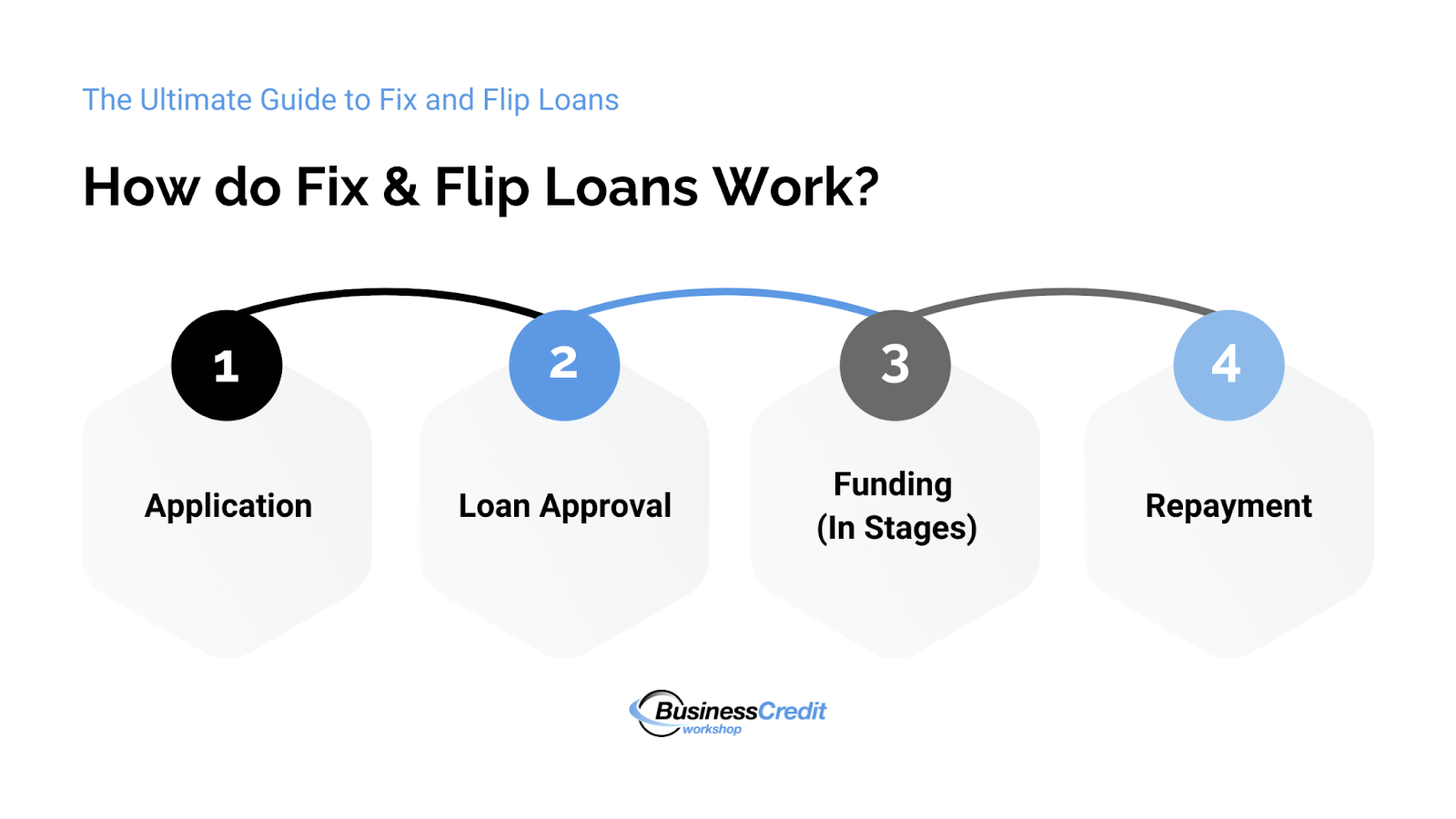

How Fix & Flip Loans Work

For the sake of relevance, we’ll talk about hard money loans that are dedicated to property flipping.

To get started, you apply for a loan by submitting a detailed plan that includes:

- How much the property will be worth after renovations (ARV)

- What the renovations will cost

- When you plan to finish them

Once the lender approves your plan, they give you the money in stages, called “draws,” as you finish different parts of the renovations. This helps manage your budget and lowers the risk for the lender.

These loans usually need to be paid back quickly, often within 6 to 18 months. So, it’s important to have a clear plan for how you’ll either sell the property or get long-term financing before the loan term ends. This way, you can pay back what you borrowed and any interest on time.

You might also like: How to Raise Money for Real Estate Investment: A Beginner’s Guide

The Risks & Challenges of Fix and Flip Loans

While fix and flip loans can definitely be lucrative, they come with inherent risks, like:

- Short repayment periods

- High interest rates or fees

- Market volatility

- Renovation overruns

Fix and flip loans have short repayment periods, typically six months to a year, aimed at minimizing interest costs but requiring precise project planning and timely property sales to avoid financial penalties.

These loans often incur higher costs than traditional mortgages, impacting profitability, particularly if renovations are extensive or sales are delayed.

Plus, economic shifts and unforeseen events like recessions can affect project profitability, which is why you need market awareness, thorough research, a contingency fund, and experienced contractors to manage risks effectively.

You might also like: The BRRRR Method: A Real Estate Portfolio-Building Blueprint

The Benefits of Fix & Flip Loans

Despite the risks involved, fix and flip loans offer several benefits:

- Quick access to capital

- Flexible options

- Potential for high returns

Fix and flip loans provide you with quick approval and funding, essential for seizing real estate opportunities swiftly, especially in competitive markets. You’ll find a variety of loan options tailored to different financial needs and project sizes, accommodating both single property ventures and larger portfolios.

With strategic property choices, renovations, and marketing efforts, fix and flip investments can yield substantial profits in a relatively short period, which makes them a potentially lucrative path to build wealth through real estate.

Recommended: How to use Business Credit to Buy Real Estate!

Types of Fix & Flip Loans to Consider

In general, people are talking about “hard money loans” when they talk about applying for a fix and flip loan. But, this isn’t the only type of financing you can use to fund a property flip. So, let’s explore your best options.

Hard Money Loans

Hard money loans are the most common type of fix and flip loan. They’re popular for their quick approval process.

These loans are secured by the property itself, making them ideal for investors who may not have perfect credit. They’re based more on the property’s after-repair value (ARV) than on your financial history.

While hard money loans offer flexibility and speed, keep in mind that they often come with higher costs.

Hard money lenders usually charge “origination points,” which are upfront fees calculated as a percentage of the loan amount. It’s best to try to negotiate with the lender to reduce this percentage and lower your initial costs—Negotiation can be critical to minimize expenses and improve the financial viability of your fix and flip project.

Before you choose this route, consider whether the speed of access to capital outweighs the cost.

You might also like: A Review of Alpha Funding Partners – Are Their Solutions Right for You?

Business Lines of Credit

Business lines of credit aren’t a loan, per se. Still, they can be used in much the same way, particularly in real estate investing—This option provides flexible access to funds whenever you need them.

Business lines of credit function similarly to revolving loans. They offer flexible access to funds as needed, making them ideal for covering project expenses without borrowing a lump sum upfront. If you have a strong credit history, securing a business line of credit can be advantageous due to its cost-effective nature—you only pay interest on the amount you draw.

Here’s a tip: Some lenders may offer promotional periods with lower interest rates or waived fees initially. It’s worth exploring these options to maximize savings on your real estate investment projects.

Recommended: This is How to Leverage Business Credit to Transform Your Life

Home Equity Loans

Using the equity in your home is a cost-effective strategy for financing fix and flip projects. Home equity loans and HELOCs generally come with lower interest rates than hard money loans, making them attractive options for funding.

However, it’s important to understand that defaulting on these loans puts your home at risk. So, you need careful financial management and a solid exit strategy—This approach is particularly beneficial for experienced investors who are adept at managing risks and timelines in real estate projects.

For those considering real estate investor lines of credit (REILOC), these specialized credit lines offer tailored financing options designed specifically for ongoing real estate investments, providing further flexibility and potential cost savings compared to traditional funding methods.

You might also like: Should You Use a Real Estate Investor Line of Credit to Renovate Property?

Personal Loans

Personal loans can be a viable option for funding fix and flip projects, particularly if you need a smaller amount of capital and have a good credit history. Here are some common types:

- Unsecured personal loans – These loans don’t require collateral, which makes them less risky for your assets. They’re typically based on your creditworthiness and income. While they may come with higher interest rates, they offer flexibility and quick access to funds.

- Peer-to-peer (P2P) loans – P2P lending platforms connect borrowers directly with individual lenders willing to fund their projects. These loans often have competitive rates and terms, depending on your credit profile and the platform’s requirements.

- Revolving credit lines – Using revolving credit to finance renovations can be convenient, but it’s important to manage interest rates and repayment terms carefully. Some credit cards offer promotional periods with low or zero interest rates, which can be advantageous if you can pay off the balance before the promotional period ends.

When considering personal loans for fix and flip projects, compare rates, terms, and repayment schedules from different lenders to find the option that best fits your financial situation and investment goals.

You might also like: 11 Alternate Ways for Entrepreneurs to Raise Capital with Online Lenders

401(k) Loans

Borrowing from your retirement fund can provide a convenient source of financing for fix and flip projects, allowing you to avoid external lenders. Since you’re essentially borrowing from yourself, the interest payments contribute back into your account.

However, it’s important you make some important considerations based on IRS guidelines:

- If you fail to repay the loan according to its terms, any unpaid amounts may be treated as a distribution from your retirement plan.

- You may need to include the previously untaxed amount in your gross income for the year of the distribution

- Unless you meet exceptions, You might face an additional 10% tax.

- Not repaying the loan can reduce your retirement savings.

To mitigate these risks:

- Ensure your repayment plan aligns with your project timelines and financial capabilities.

- Consider consulting a financial advisor to navigate the complexities of using retirement funds for real estate investments.

These steps are crucial to assess whether borrowing from your retirement fund is the best choice to fund your fix and flip projects.

You might also like: 1-800Accountant Reviews: Expectations vs Reality

Seller Financing

You may be able to leverage seller financing, also known as owner financing or seller carryback, when the property seller provides financing instead of or alongside a traditional mortgage lender—This arrangement can offer flexibility in terms, potentially lower costs, and a streamlined approval process. It’s particularly attractive if you may not qualify for a conventional loan.

Now, while it seems like a great idea, it’s super important to approach seller financing with caution. Conduct thorough due diligence on the property and negotiate clear terms with the seller to avoid misunderstandings or disputes later.

Weigh the benefits against potential risks and consider seeking legal advice to ensure all agreements are legally sound and in your best interest.

This is How to Qualify for a Fix & Flip Loan

Qualifying for a fix and flip loan hinges on several key factors that can significantly influence your ability to meet fix and flip loan requirements.

To enhance your chances of qualifying for a fix and flip loan and secure favorable terms:

- Work on your credit score

- Build your real estate experience

- Invest in the property evaluation process

- Get your documents organized

By taking proactive steps to strengthen your financial profile and project plan, you can position yourself as a strong candidate for a fix and flip loan. Here’s a deeper dive into each factor to help you navigate the process effectively.

1. Get Your Credit in Check

Improving your credit score is crucial before applying for a fix and flip loan.

For personal credit, focus on paying down debts, correcting any errors in your credit report, and ensuring timely payments on all obligations—A higher personal credit score generally leads to better loan terms and lower interest rates, reflecting your financial reliability to lenders.

For business credit, maintain a good payment history with vendors and suppliers, and ensure your business accounts are separate from personal finances. A strong business credit profile demonstrates stability and can improve your chances of favorable terms for fix and flip loans.

Lenders often consider both personal and business credit when evaluating your loan application, so strengthening both can enhance your borrowing options and overall financial position.

Recommended: This is How to Build Business Credit Fast [Step-by-Step Guide]

2. Network With Other Real Estate Investors

If you’re just starting with fix and flip projects, team up with seasoned investors or tackle smaller projects first to establish a track record. This builds credibility and gives you hands-on experience in real estate investing.

Having prior experience in real estate investment can significantly strengthen your standing with lenders. They often prefer borrowers who have successfully completed fix and flip projects before. This track record demonstrates your ability to handle property renovations and sales effectively, reassuring lenders about your capability to manage projects and repay loans on schedule.

Note that, in some cases, lenders may even stipulate a minimum number of completed projects as a qualification requirement.

You might also like: The Best Credit Cards for Landlords: A Comprehensive Guide

3. Learn How to Evaluate Properties Effectively

Make sure the property undergoes a thorough evaluation by a specialized real estate appraiser. A precise estimate of its after-repair value (ARV) supports your loan application and may increase your borrowing potential.

Lenders rely heavily on the ARV, which forecasts the property’s post-renovation worth. A professional appraisal is typically required to accurately determine the ARV, guiding the maximum loan amount based on future value. This calculation influences the loan-to-value (LTV) ratio, crucial for securing financing. Lenders also assess the property’s current state and location to gauge renovation feasibility and market potential.

Real estate investors commonly use two strategies to assess potential fix and flip profitability:

- The 70% rule advises not paying more than 70% of the ARV minus repair costs. For instance, if a property’s ARV is $200,000 and repairs cost $40,000, the maximum purchase price should not exceed $100,000.

- The 2% rule suggests that monthly rent should ideally be at least 2% of the property’s purchase price, primarily used for rental property evaluations.

These strategies help investors make informed decisions to optimize returns and minimize risks in real estate investment.

You might also like: Y Combinator: Fast Track to Success or Waste of Time?

4. Get Really Good at Organizing Your Documents

Ensure you gather all required financial documents early in your loan application process. A well-organized project plan is crucial to show your readiness and dedication.

Thorough financial documentation is vital when applying for a fix and flip loan. Include recent tax returns, bank statements, and a detailed project plan outlining your renovation strategy and projected costs.

Transparency about your financial status demonstrates your ability to manage the loan responsibly and gives lenders confidence in your financial management skills—This can enhance your chances of approval and may result in more favorable loan terms.

You might also like: Free, Printable Business Credit Application Template

Common Alternatives to Fix and Flip Loans

When traditional options won’t work, consider alternative funding options like cash reserves, crowdfunding, or joint ventures for your fix and flip project.

| Pros | Cons | |

| Cash Reserves | No loan interest costs.Best for financial stability.No new debt obligations. | Ties up liquidity.May limit opportunities.May reduce emergency funds. |

| Crowdfunding | Spreads risk by pooling funds.Access to larger projects.Increases diversification. | Limits control over choices.Potential project delays if goals are unmet. |

| Joint Ventures | Costs shared with partnersRisks shared with partners.Access to capital and experience. | Requires clear agreements.Highest potential for conflict or disagreements with partners. |

In some cases, these alternatives can provide flexibility and leverage in financing your fix and flip ventures beyond traditional loan options.

With cash reserves or “personal capital,” you can use your personal savings to avoid loan interest costs. But, this may tie up liquidity, which can limit other investment opportunities or emergency funds.

Crowdfunding platforms like Fundrise let you pool funds with others, spreading risk and accessing larger projects. It offers diversification, but may limit control over property choices.

Partnering with investors allows you to share costs and risks, which is beneficial if you lack experience or capital. Just make sure to establish clear agreements to manage expectations and ensure a successful partnership.

You might also like: Torro Business Funding Review: Is This Zero Hassle Offer Legit?

Frequently Asked Questions

Can you get a fix and flip loan with bad credit?

Yes, but expect higher rates. Hard money loans may be an option as they focus more on the property’s value than the borrower’s credit score.

How do fix and flip loans differ from traditional mortgages?

They are shorter-term, have higher interest rates, and focus more on the property’s potential value rather than just your credit score and income.

What happens if you default on a fix and flip loan?

You may lose the property, and it can impact your credit score. It’s essential to have a solid exit strategy to avoid default.

How do you avoid taxes on a fix and flip?

Consider reinvesting profits into another property through a 1031 exchange to defer taxes. Consult a tax professional to understand your options.

Conclusion

Deciding on fix and flip loans comes with challenges and rewards. Understanding these loans—from hard money to personal funds—helps you fund projects wisely for better profits. Each loan type has things to think about, like fast cash or higher rates. Pick what matches your goals and risk level.

As you start your fix and flip journey, keep learning about markets, property checks, and money plans. This helps you make smart choices, lower risks, and grab good deals in real estate. Whether you’re new or a pro, using the right loans can make your fix and flip projects successful.

Ready for more? Look into loans, plan your investments, and jump into fix and flip real estate. Your path to money growth and real estate wins starts now!

Interested in using business credit to fund your fix and flip venture? To learn how to obtain up to $100K in business credit, join Business Credit Workshop today!