Historically, business credit building with net 30 terms has been reserved for vendors that sell business and office supplies or fuel cards. But, in the age of the internet, digital services like Fidextech have started to offer net 30 terms and business credit building opportunities.

Unfortunately, not all offers are created equal. It’s important to understand exactly what you’re getting when you sign up for an offer that promises to help you build business credit. Find out whether or not enlisting Fidextech for your digital creative needs will help you meet your goals.

This is what’s in store:

- What is Fidextech?

- Fidextech Features

- Fidextech Net 30 Overview

- Conclusion: Is Fidextech Legit for Business Credit Building?

Now, let’s dive in!

What is Fidextech?

Fidextech is an NYC metro area digital design studio that offers a range of offers that aim to help businesses grow.

Their services include:

- Digital marketing

- Creative works & design

- Web packages

- Hosting

- Product photography

As a bonus, they offer net 30 terms, which means you can pay your balance within 30 days – you don’t necessarily have to pay right away. In some cases, net 30 vendors can help you build business credit, which is a great way to get the capital you need to grow your business. I’ll share more on that later.

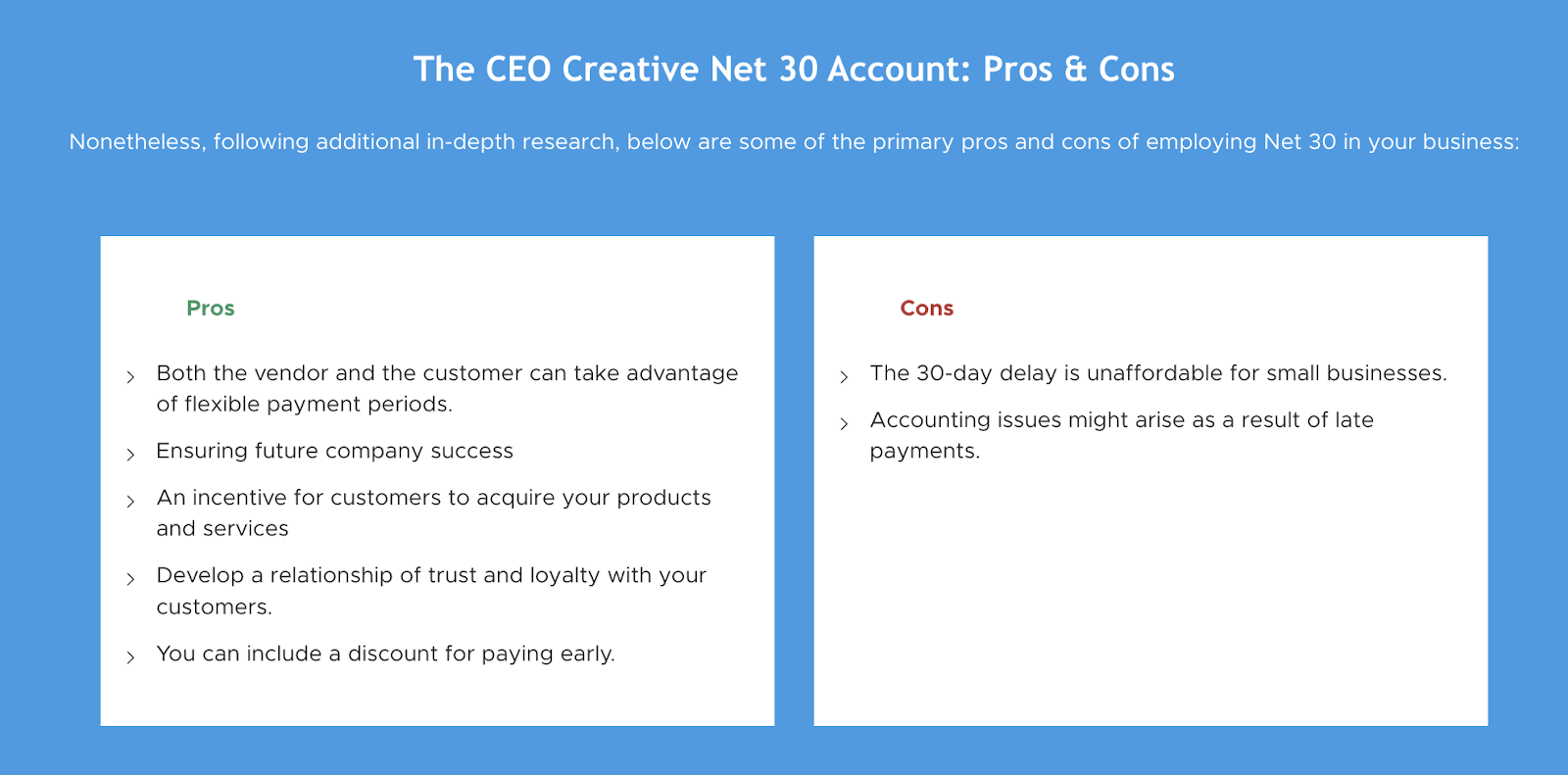

You might also like: The CEO Creative Net 30 Review: Is it Worth Your Time?

Fidextech Company Overview

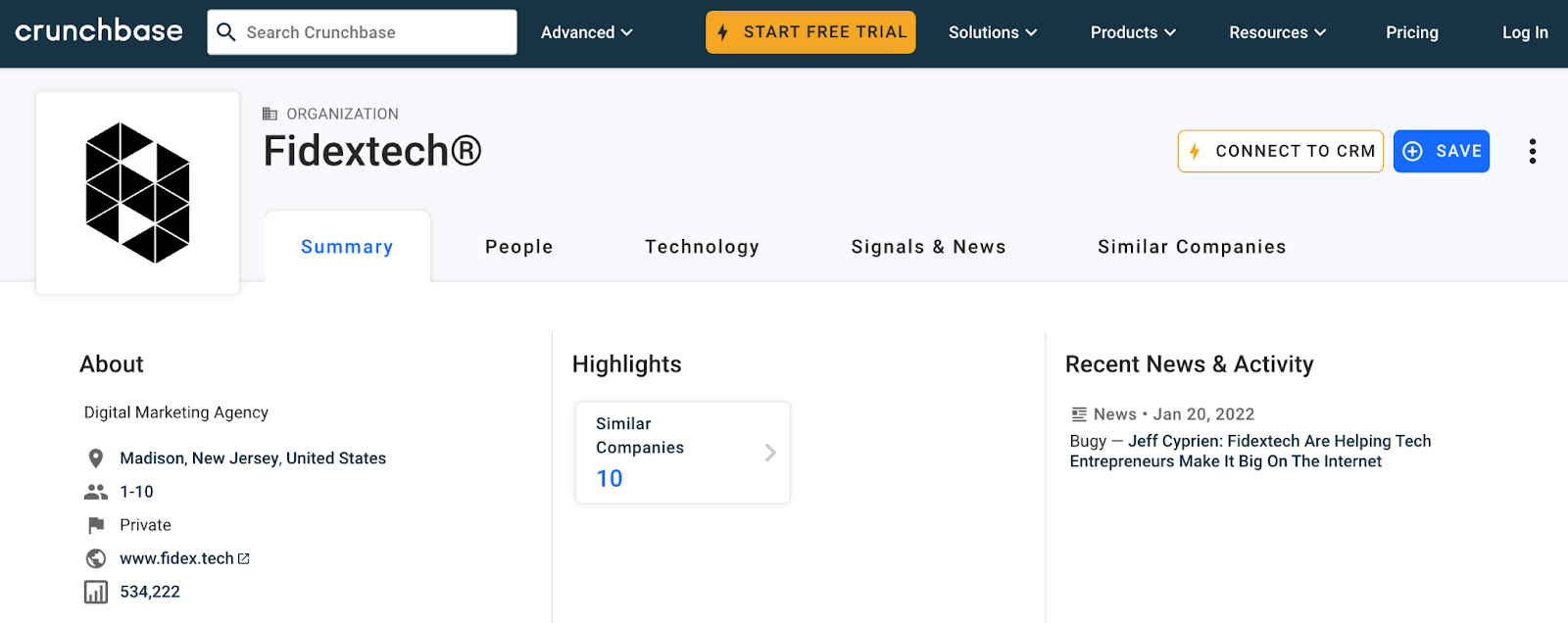

Fidextech LLC is a Madison, New Jersey-based business services agency that was founded in 2017 and registered in September, 2020. Multiple sources cite the company as having ten or fewer employees.

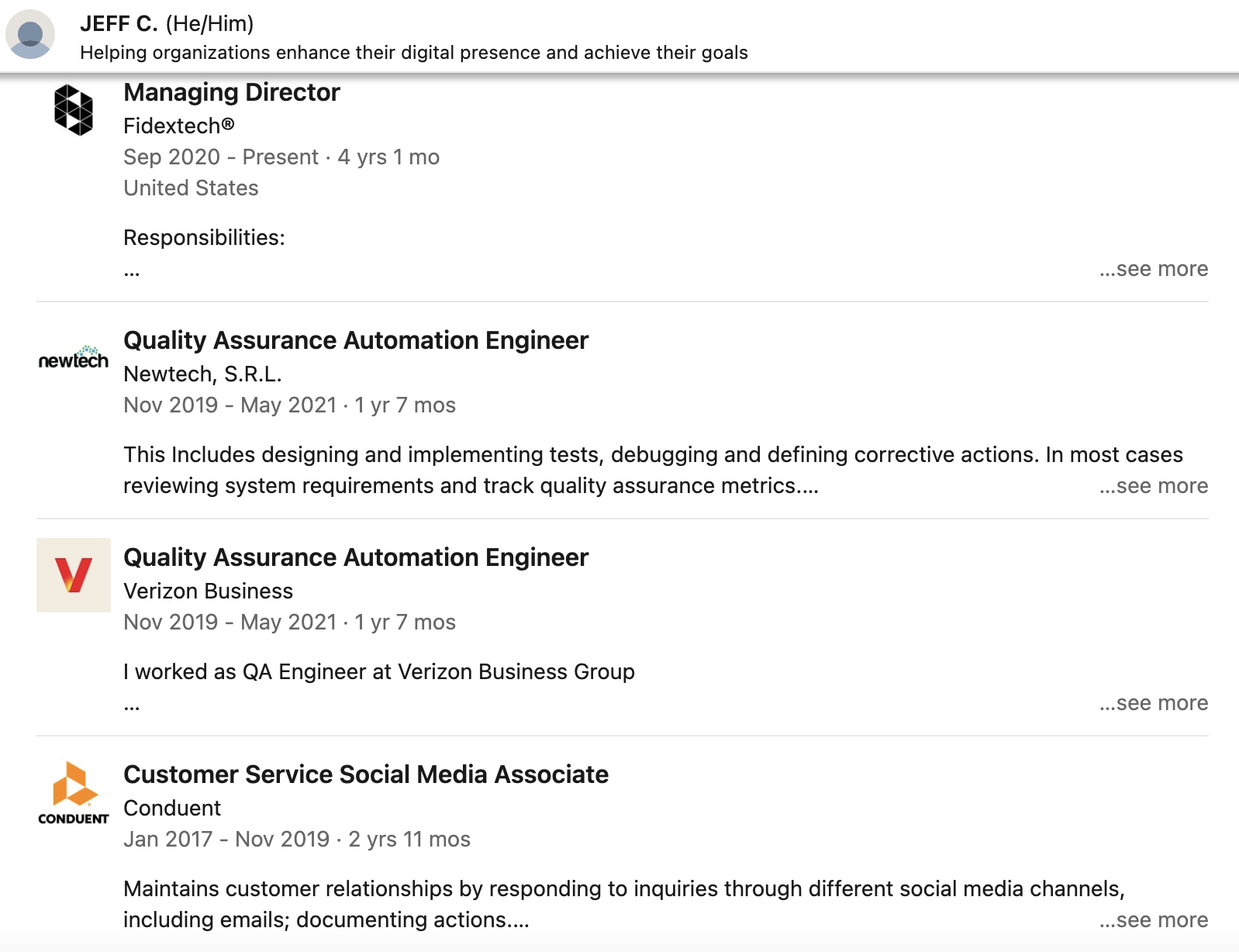

The only human name I found to be affiliated with the company is Jeff Cyprien. On LinkedIn, he’s known as “Jeff C.” and lists himself as the Managing Director of the company.

Cyprien’s previous experience includes a few years as a Quality Assurance Automation Engineer at Verizon and Newtech and a few years as a Customer Service Social Media Associate at Conduent. I can’t say for sure that Cyprien is Fdextech’s founder, but it appears that is the most likely case.

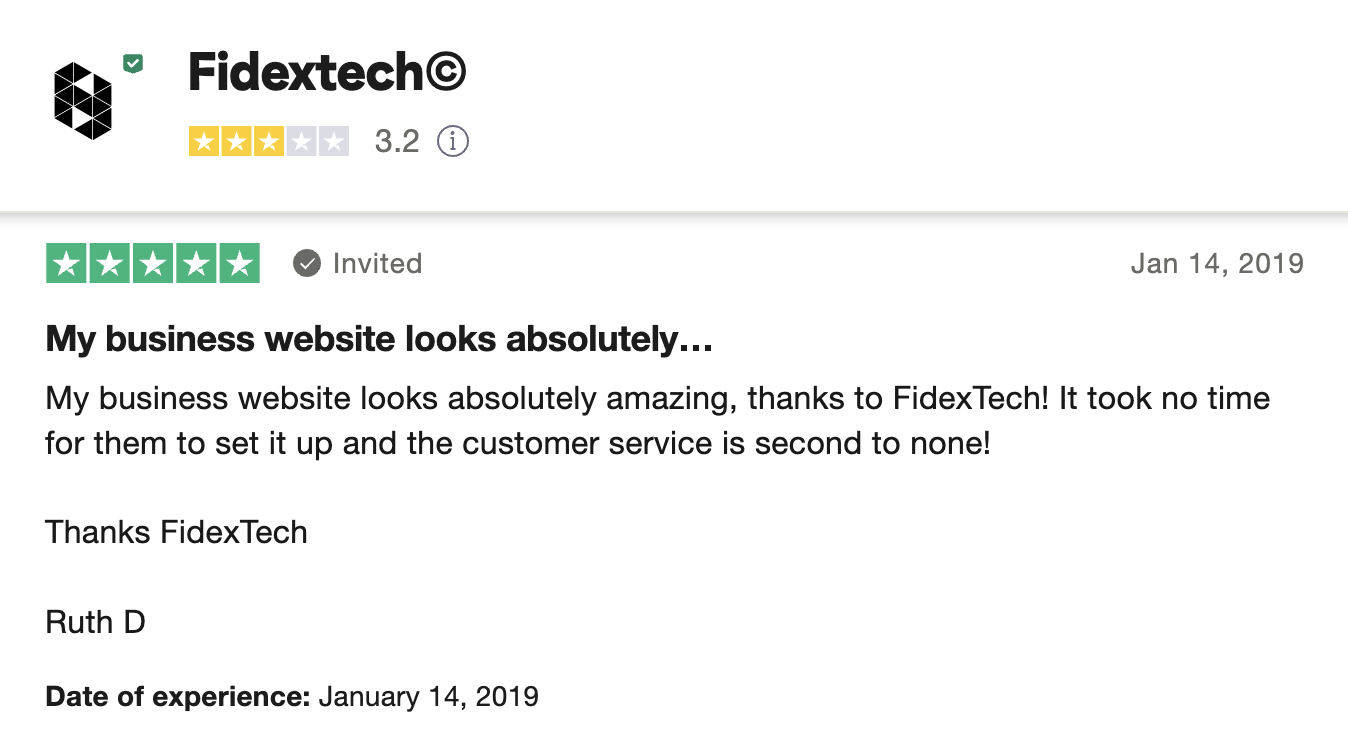

While I couldn’t find a Better Business Bureau profile for the company, and nobody has mentioned them on Reddit, Fidextech is listed on Trustpilot. Of their 10 reviews on the platform, most of them are positive, yet their TrustScore is a middling 3.2. One user reports “very rude” customer service, while the rest of the feedback is pretty positive.

Overall, there’s a lack of transparency, which leaves me without enough information to give you any sort of opinion on the company’s legitimacy. If anything, I might say that their website and offer is deceivingly professional looking without enough trust signals.

You might also like: The Growegy Net 30 Account: Is it a Legitimate Offer?

Fidextech Features

Now, for the offer. If you sign up with Fidextech, this is what you can likely expect, based on the website and advertising.

1. Digital Marketing

To double-check my initial assumption, I decided to peek in at a couple of their digital marketing clients’ websites at random:

- prophecyhomecare.com

- savorird.com

The first has low ranking metrics and the latter isn’t reachable, as of mid-September 20204. So, I don’t see any sign that they can deliver on the digital marketing offer.

Fidextech also offers digital marketing consultation. I wouldn’t be any more eager to hire them for this than I would marketing implementation.

2. Creative Works & Design

I won’t be so hard on Fidextech in the creative works and design arena—the few client websites I was able to pull up at were aesthetically appealing. And, if the brand’s own website is a testament to the agency’s skills, I would say they at least know what they’re doing in the way of web design.

However, their work examples were out of date when I viewed them. Several of the websites in the Fidextech case studies section were no longer live when I tried to view them.

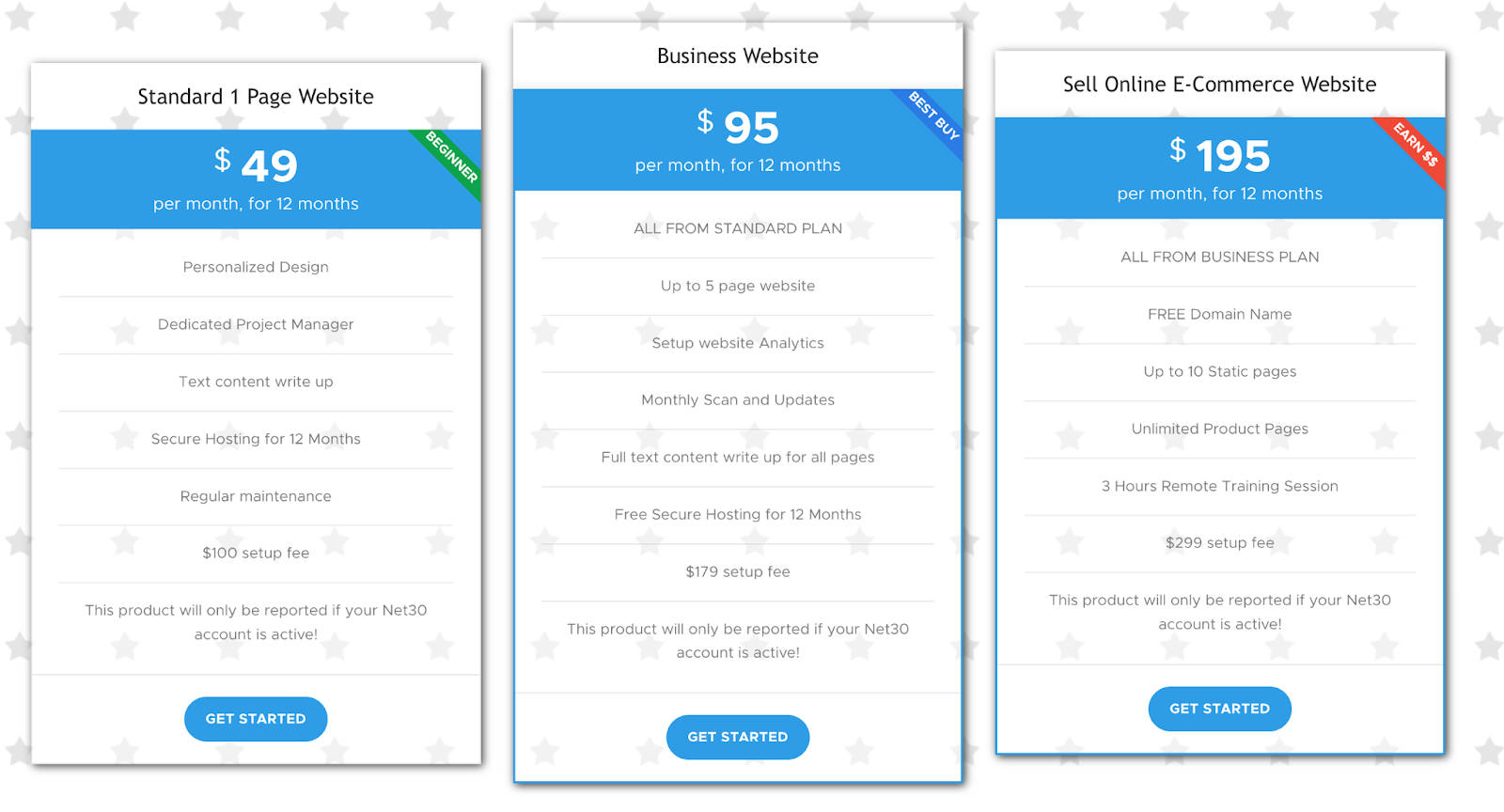

3. Web Packages

If you sign up for a web package, Fidextech promises to help you with eCommerce (online shopping), CMS web design (WordPress), web development, and web support.

This means you can get help designing, redesigning, or migrating your website. You’ll need to request a quote to find out how much a customized package will cost.

4. Hosting & Domain Registration

Fidextech also offers shared and cloud hosting, dedicated server space, domain name registration, and hosting support. This can be really helpful if you’re not technologically inclined.

They offer the following domains for registration:

- .com

- .tech

- .club

- .blog

The main problem with relying on someone else for these types of services is that they might end up being the one in control of your account. But, this can be a good thing if that’s what you prefer.

5. Product Photography

Finally, Fidextech advertises product photography services. If you need help with food photography, eCommerce or advertising product photography, or still life photography, this could be a great add-on service.

Usually, specialized photography is a standalone offer that requires you hire someone separate from your web developer or take your own website photos. So, this service might give Fidextech an edge. Sadly, I couldn’t find examples of their photo quality, so I can’t recommend this service either.

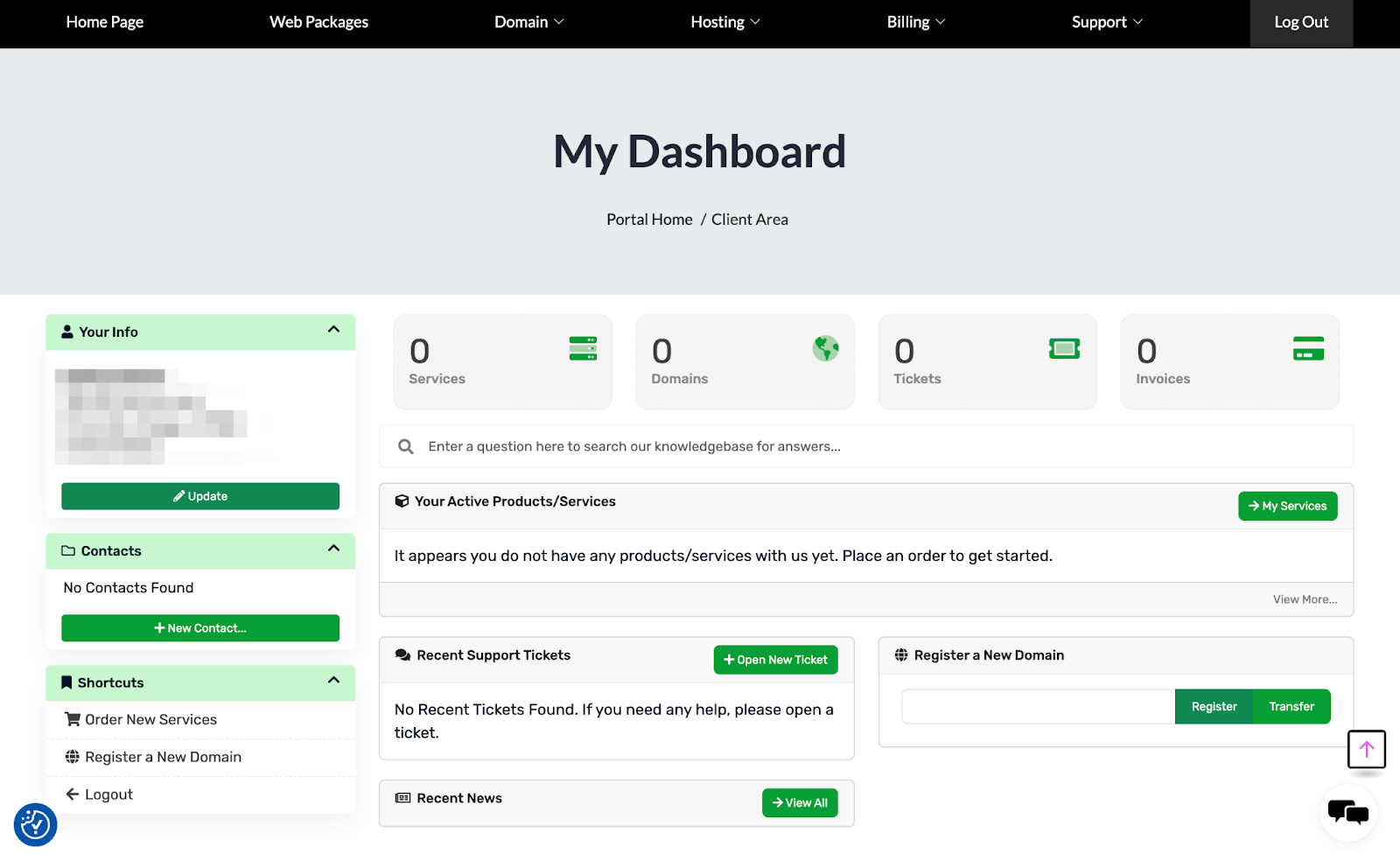

6. Dedicated Account Dashboard

It’s interesting that Fidextech offers an account dashboard for a marketing services offer. At first, it seemed more like a project tracking dashboard, but I noticed you can add services once you’re logged in.

You can register, renew, and transfer website domains without speaking to anyone at the company from inside your Fidextech dashboard…Proceed with caution because it’s impossible to say how reliable this platform’s hosting is.

Fidextech Net 30 Overview

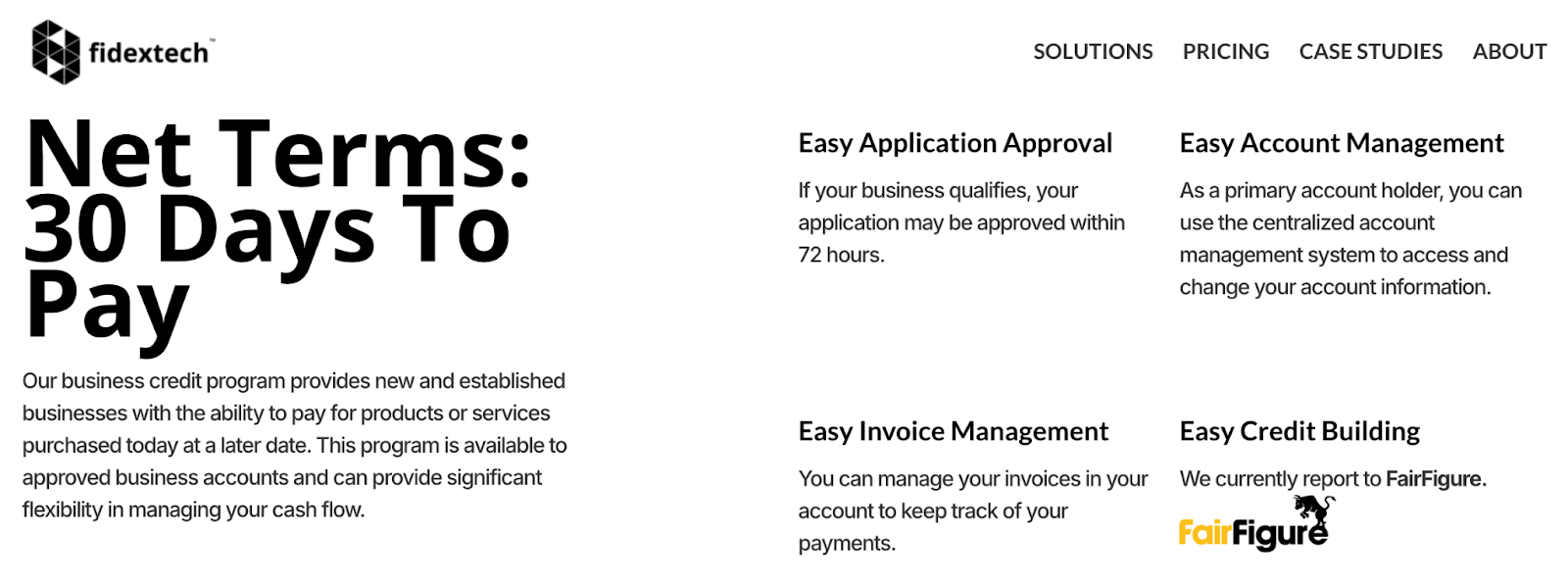

Fidextech offers net 30 terms to “approved” customers. In this case, it appears as though you would need to be approved for the FairFigure card, which is a business credit builder offered by a third party.

So, you’ll need:

- A legally established entity.

- An EIN.

- A business bank account that connects to Plaid.

- Probably at least $2.5K in monthly revenue.

I’ve read that most businesses that apply will qualify for an initial limit of $1000 on the FairFigure card. After you’re approved, you’ll be able to pay for your Fidextech digital services with the dedicated card and pay later with net 30 terms.

The FairFigure Review is coming soon, so sign up for our emails or come back soon to learn more.

What Credit Bureau(s) Does Fidextech Report to?

Most business net 30 accounts that offer reporting will report directly to a business credit bureau or multiple bureaus like Experian Business, Equifax Commercial, or Dun & Bradstreet. As of September 2024, Fidextech currently reports account payments to FairFigure, which is a newer credit building platform, NOT a business credit bureau.

According to FairFigure’s official website, they report data to Equifax Commercial, CreditSafe USA, SBFE, and their own Foundation Report. So, through Fidextech (if they hold up their end of the bargain), you may be able to get on-time payments reported to these bureaus through the third party service.

There is no indication that your payments to Fidextech will be reported to Experian Business nor Dun & Bradstreet—This may change, so check the official website for the most up-to-date information.

Recommended: Everything You Need to Know About a DUNS Number – and Why You Should Care

How Do You Cancel a Fidextech Account?

To cancel your Fidextech account, provide a 30-day notice via phone at (877) 353-5223 or make an appointment via the Fidex.tech contact form. Access to products will be suspended upon termination.

According to their terms, you may be able to terminate immediately if Fidextech becomes insolvent or breaches the contract.

You can request a refund for clear balances in your advance account, unless you violated the agreement. Refunds will be processed within 14 business days, minus bank fees.

Payments during a trial period or already debited amounts are non-refundable. Follow Fidextech’s guidelines for proper cancellation and refunds.

You might also like: Office Garner Review – NET 30 Vendor

Conclusion: Is Fidextech Legit for Business Credit Building?

While Fidextech offers an intriguing opportunity for businesses seeking to build credit through net 30 terms, potential users should approach with caution. The range of services—from digital marketing to product photography—presents a comprehensive package, but the company’s transparency and customer service reviews raise concerns.

The lack of a solid track record, coupled with limited information on its business credit reporting practices, makes it crucial for you to weigh the pros and cons carefully.

Before you commit to anything, make sure you fully understand the terms and your eligibility for the FairFigure card, as well as the implications of relying on a third-party credit builder.

Do you want to learn how to obtain up to $100K in business credit in as few as 30 days? Join Business Credit Workshop today!