When you’re a Dell-lover looking to build your credit profile and in need of a new computer, in-house financing is a natural place to turn. You can get upfront funding for your new equipment and potentially boost your scores. But, is the program worth your time? Read this Dell business credit review, and answer that question yourself.

First of all, What is Dell Business Credit?

Dell business credit is one of three business financing packages offered by Dell to fund the purchase of its PCs, electronics, and accessories. The business credit program is controlled by WebBank, who also partners with companies like Avant, Lending Club, Fingerhut, and PayPal to offer financial services to these brands’ existing customers.

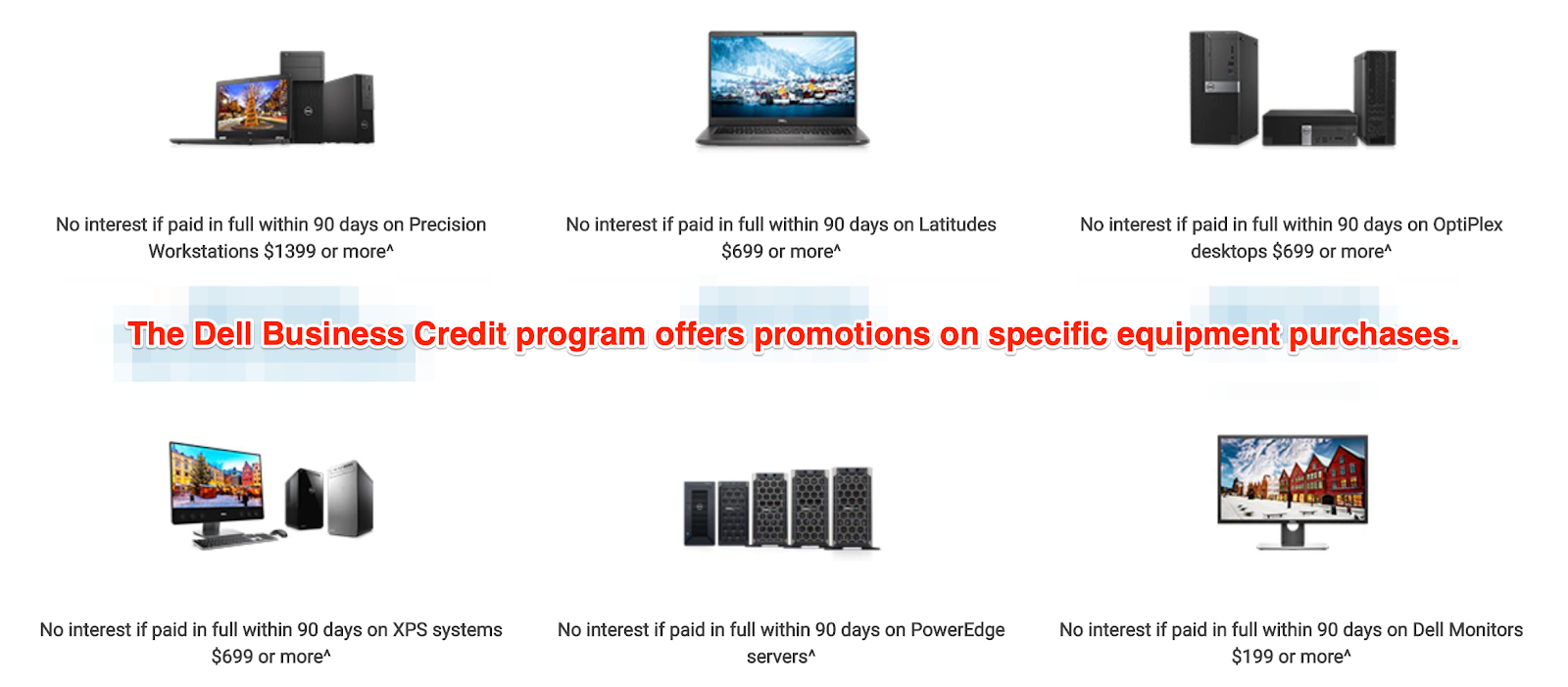

Financing can only be used to purchase directly through Dell and the brand offers promotions on specific equipment. 90-day, 0% interest is a popular example.

The three financing options offered by Dell are:

- PC as a service

- Dell business credit

- Lease options

In addition, Dell offers custom solutions for enterprise solutions for medium and large businesses. So, larger companies can reach out with their needs to come up with packages under the pretense of greater savings on bigger orders.

At first glance, the program looks fine. Yet, Dell’s business financing reviews online seem to deliver more than the usual amount of complaints. So, I decided to dig into the program and share unbiased facts. After reading through, you should be able to decide if the program is worth your time.

Next, How Difficult is it to Get Dell Business Credit and Will You Qualify?

Borrowers who apply for Dell business credit are often surprised by the approval process and credit amount. For example, one business applicant who made $62K in purchases from Dell the previous month was offered a $5K tradeline (MyFico). The amount of funding led this user to the conclusion that WebBank, the actual lender, doesn’t factor customer metrics within the Dell company into its decision.

While this seems a bit wonky and impersonal, Dell did allegedly finance another customer for the same $5K business credit with no social security number and after locking their reports (MyFico). This possibility is appealing because it means that you could potentially qualify for a tradeline without sharing your personal credit report and conceivably start building business credit.

So, if WebBank will qualify an applicant for $5K in credit with no credit history, how easy is it to get a Dell business credit card?

According to WallettHub, WebBank’s cards, including the Dell Preferred Account (which is not the same as the business credit card) are subject to approval with personal credit scores of 640 and up. So, while all situations are different, it’s a fair assumption to make that it is pretty easy to qualify.

And, What Business Credit Report Does Dell Pull?

If you have a fair business credit history with one bureau and bad credit on another, you need to make sure your lender will look at the report with the more favorable score. So, which report will Dell/WebBank peek in at when qualifying you for approval? According to multiple borrowers, you’ll see a hard pull on your Experian report when you apply for a Dell business account.

Then, Why all the Poor Reviews?

Let’s take a look at the common complaints about this card from existing borrowers.

- High interest

- Poor customer service

- High interest

- High interest

- Lack of payment technology

- High interest

Many of Dell’s borrowers complain about the fact that they still owe the full amount of their equipment after making payments, sometimes for years. And, they express that there was no explanation that if their account wasn’t paid in full before the promotional no-interest period, that they would be charged the full interest amount.

Yes, the above is frustrating, but these payment conditions were in the terms and conditions laid out by Dell and WebBank. It’s just that the borrowers didn’t see or understand them.

You should always expect to pay interest on purchases made during a promotional 0% interest financing period if your balance is not paid in full before the end of the period.

So, is Dell Business Credit Worth Your Time?

If you need Dell equipment, should you go straight to the source for funding? — This is the wrong question. Instead, ask yourself the following:

- What are Dell’s current business credit promotions?

- If I leverage these promotions, can I save money on the equipment I need (the promotions often offer 15% price discounts on products)?

- If I leverage these promotions, will I be able to pay off my card within the promotional period to prevent future interest spikes?

If you need Dell equipment and you can afford to pay off your purchase within 90-days, there’s no reason not to take advantage of the financial services. In fact, you could see a bump in your credit scores for on-time payments.

Related Answers

Does Dell have financing?

Yes, Dell offers several consumer and business financing solutions through WebBank for the purchase of its equipment and accessories.

What credit score is needed for Dell financing?

According to WalletHub, WebBank, who controls Dell’s financing options, qualifies borrowers with credit scores of 640+

What business credit report does Dell pull?

When applying for Dell business credit, your Experian report will be pulled.

Does Dell finance bad credit?

According to many borrowers, Dell credit is fairly easy to qualify for, but typically, lenders do not finance anyone with bad credit.

Can I buy a laptop and pay monthly?

Yes! You can leverage financing directly through most laptop manufacturers as tradelines or use alternative funding options to make monthly payments on a new laptop.

Can I lease a laptop?

Yes! Most major laptop manufacturers have lease options for businesses and consumers. Dell’s progressive leasing is one example.

Final Thoughts

Dell business credit offers no major rewards — this type of financing doesn’t allow you to generate points, airline miles, or cash awards. But, for businesses early in the credit building journey, if leveraged properly, Dell’s in-house financing can be helpful. Learn how to make the most of your credit profile. Start by understanding how to use 30-day net vendors to boost your business credit score.