Each month, thousands of people search for details about the credit card that touts an offer that will help you build credit with no credit check, fees, or interest, with up to a $10K spending limit. TomoCredit’s free card almost sounds too good to be true. So, is it?

In this credit card review, I’ll answer this and other pressing questions — everything you need to know before you apply for the Tomo offer, whether you’re a consumer or a business owner.

Here’s what you’ll learn:

- How Does a TomoCredit Card Work?

- What Do Cardholders Think About the TomoCredit Card?

- TomoCredit Company Overview

- Frequently Asked Questions

- The Verdict: Is the TomoCredit Card Trustworthy?

Now, let’s get moving.

How Does a TomoCredit Card Work?

In a nutshell, TomoCredit’s software connects to your bank account and analyzes spending behavior to determine your eligibility and initial credit limit (if any). The offer is designed for young adults and U.S. immigrants but not restricted to any demographic — anyone (even non-citizens) with a bank account, SSN or ITIN, and a government-issued ID can apply without impacting their credit score.

Now, there is a small catch: you need to pay your balance in full each week to maintain your account. It’s similar to a charge card or Net terms offer.

TomoCredit is a legitimate company, and everything above is true. Still, there’s more to look at

First, the card comes with a range of features and benefits.

1. It’s Free

There is no annual fee and no interest. The truth is that they can’t competitively charge interest because no balance will be carried on the card. This restriction will probably pay off for anyone who has a hard time paying their balances in full, and it limits cardholders’ ability to rack up too much debt.

However, you do need to have at least $800 in your bank account to qualify.

2. No Credit Score is Required

Usually, credit card issuers rely on credit scores to determine an applicant’s creditworthiness. Lower credit scores typically leave people with credit card and loan options that have higher interest rates, lower spending limits, and fewer benefits.

Tomo was designed for people with no credit (who the founders believe are worthy of financial options) who want to build a better life. Hence, a credit score doesn’t factor into the decision at all.

3. Access World Elite Mastercard Rewards

TomoCredit’s card is provided by World Elite Mastercard, hence cardholders can leverage the benefits.

- Earn 1% cashback on all purchases in addition to other savings and rewards.

- $1,000 cell phone protection – pay your phone bill with your TomoCredit card and get protection for up to $1000 with a $5 deductible.

- Savings on partner offers from Lyft, DoorDash, Fandango, ShopRunner, and McAfee.

- Exclusive offers from Priceless.com – take advantage of experiences and courses only available to Mastercard cardholders with a Priceless.com membership.

If you do receive a TomoCredit card (or any other World Elite Mastercard), be sure to explore the benefits and take advantage of what you can to make your experience more worthwhile.

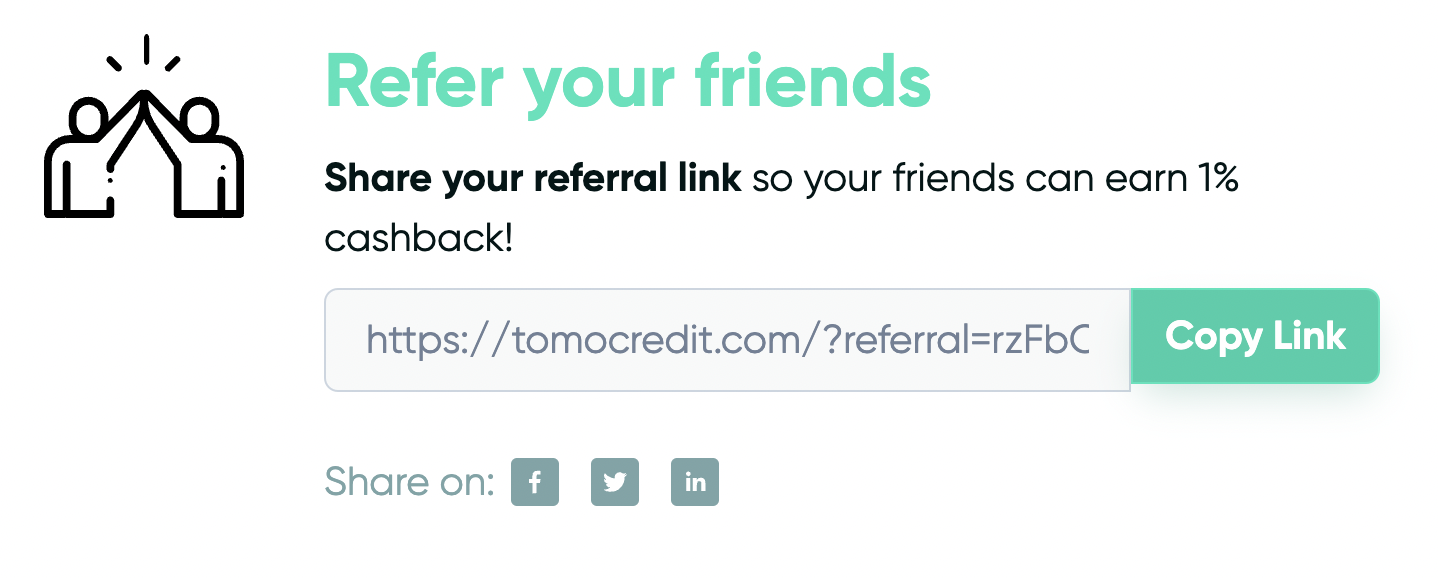

4. Earn Cashback for Referrals

Last week, I shared an X1 Card review, and found out that they’re offering up to 10X points on referrals, and inviting some cardholders to leverage unlimited rewards. And, I know that Tomo encourages users to invite others to apply, but the public offer leaves me wondering about the details of their referral rewards offered for.

I know that cardholders can earn 1% cashback for referring your friends. But, I still don’t know how many people you can refer in a calendar year, nor how long the 1% can be earned (is it 30 days? 90?). So, I reached out to the team for more details about the offer, and I will update this page as soon as I have it.

What Do Cardholders Think About the TomoCredit Card?

While the offer is fairly new, it’s been around long enough to gauge what current cardholders think about the offer. So, I’ve done some digging, and here’s what I found.

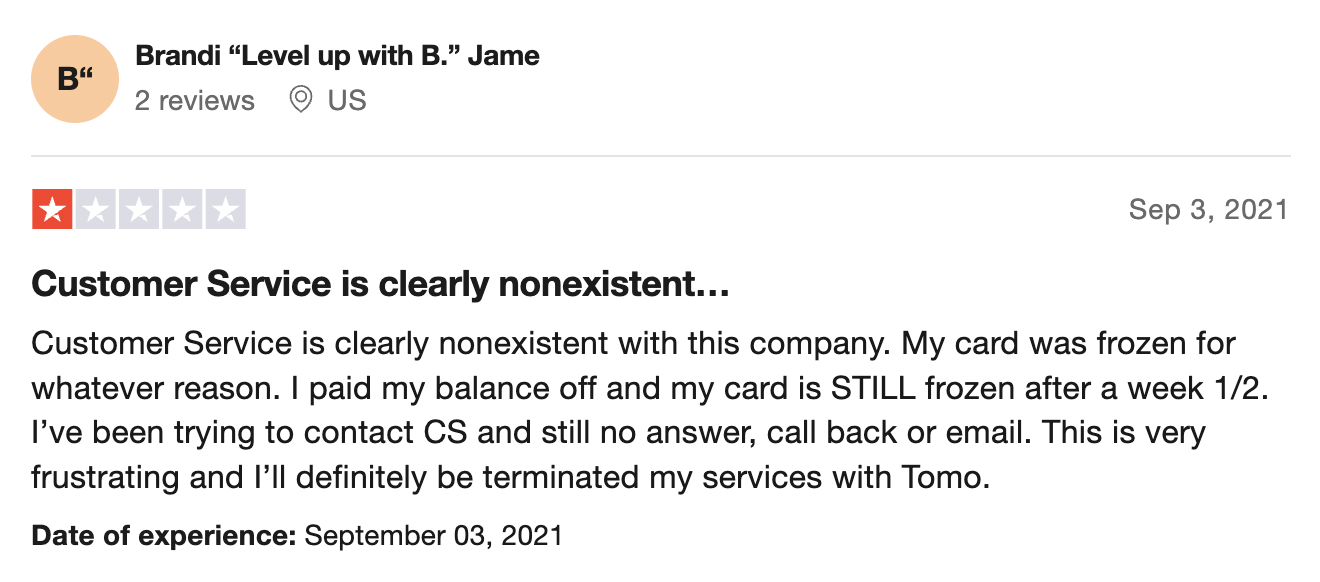

Some cardholders have been unhappy with the lack of reporting on behalf of Tomo. I’m going to say that you should err on the side of caution here, but that it can take a bit of time and a ton of active accounts for a financial offer to establish a reporting relationship with credit bureaus. With an optimistic mindset, I believe Tomo will start reporting to all three credit bureaus as agreed soon if they haven’t already.

Next, several account holders complain about Tomo’s poor customer service and communication. Cardholders should be able to contact the phone number on the back of their card for help with their accounts. I can’t verify whether this is the case or not — if it isn’t, then it would be the first card I know of that doesn’t have a contact number.

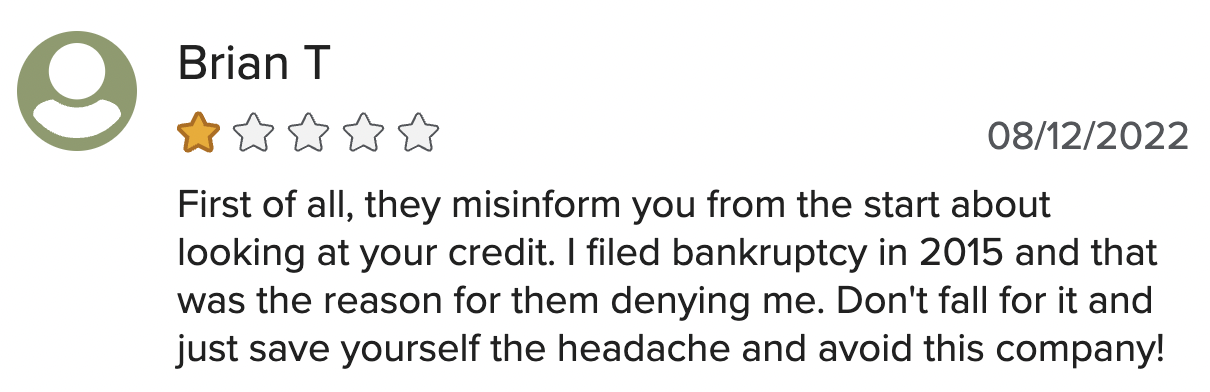

Finally, according to at least one user, they may factor a previous bankruptcy into denial for credit. For a company that is built to help people build credit, this doesn’t make a lot of sense to me.

Recommended Reading: Credit Secrets Book Review: Can you Erase Bad Credit?

TomoCredit Company Overview

TomoCredit was founded in 2018 by Kristy Kim and Dmitry Kashlev. It’s both minority-owned and woman-owned.

Prior to founding TomoCredit, Kristy Kim (Tomo’s current CEO) worked as a Finance Counsel Member at Forbes and formerly was the Vice President of Investments for Kinetic. And, before 2018, Dmitry Kashlev (CTO) was a Senior Software Engineer with Qventus and Software Architect at Eargo. Between the two of them, they have strong financial and technology backgrounds. So, it seems like a good match for a partnership like this.

Kristy Kim is pretty active on Reddit and has even done a couple of AMAs, where she’s answered questions, and responded to positive feedback as well as that of the trolls and naysayers — this isn’t something you see every day with founders.

Some of Kim’s answers are perceived as elusive, but I think people should cut her some slack — some of the company’s investors probably have a hand in what she’s allowed to disclose about the offer.

And, since they’re currently looking for a Brand Marketing Specialist to bring onto the team, I think we’ll start to see more transparency and a more organized presentation of the offer.

How Does TomoCredit Make Money?

Tomo’s card offer comes at no charge to consumers, so people have wondered how the company makes money. There’s one conspiracy that they’re bringing the social credit system to the US (this might not be 100% false). But, TomoCredit actually earns from interchange fees — merchants pay a small percentage to Tomo each time transactions are processed.

The interchange fee revenue model can be profitable with enough active cardholders, as we’ve seen with corporate cards from Ramp, Brex, Stripe, and Divvy. However, TomoCredit is not profitable… yet.

The company does plan to add auto loans and mortgages to its financial offer down the road, possibly within the next ten years. Both auto loans and mortgages are highly lucrative business models. There’s no way to know if the card offer will be a gateway to more traditional loan offers or if the loan and mortgage offers will be more innovative like the card.

Frequently Asked Questions

Does Tomo pull your credit?

No. When you apply for a TomoCredit card, you will not receive any pull to your credit (not even a soft inquiry). Instead of a credit report, the system uses information from activity in your bank account to make a creditworthiness determination.

Is TomoCredit Card secured or unsecured?

TomoCredit offers an unsecured credit card. But, some features such as weekly payments in full are like a secured account.

Where is the Tomo card accepted?

The TomoCredit card is a Mastercard and is accepted by millions of merchants (anywhere Mastercard is accepted).

Can you carry a balance on a Tomo card?

No, since the card is designed to help users build credit, they do not allow cardholders to carry a balance. Weekly payments made in full are required to maintain a TomoCredit card account.

How often does Tomo report to credit bureaus?

At the end of each calendar month, TomoCredit reports cardholder payments to credit bureaus. With the claim that they are the “first card to offer expedited weekly payments,” this can be confusing. To confirm, Tomo reports each month, not each week.

Which credit bureaus does Tomo report to?

TomoCredit reports cardholder payments to Transunion, Equifax, and Experian. Though, some cardholders have complained that the company is not reporting monthly to all three bureaus yet. Tomo does not report to business credit bureaus.

Will TomoCredit Help You Build Business Credit?

When you apply for a Tomo Credit card, Plaid will connect the automated underwriting system to most major checking accounts, including business accounts. But, Tomo does not report on-time payments to business credit bureaus. So, accepting a Tomo credit card offer will not help you build business credit.

Can you use a Tomo card at an ATM?

No. TomoCredit offers a credit card, not a debit card. And, they do not currently allow any cash advances or ATM withdrawals.

Does the Tomo card have an app?

Yes, TomoCredit has Tomo Card apps for iPhone and Android to help users conveniently activate their cards, track their account activity, and pay their credit card bills.

How do you contact Tomo?

As of today, TomoCredit doesn’t have a live chat on their forward-facing website, so you can reach out via their website contact form, email help@tomocredit.com, or call the phone number on the back of your TomoCredit card. Current cardholders can use the in-app chat when logged in to their account.

The Verdict: Is the TomoCredit Card Trustworthy?

To me, there are a few warning signs with Tomo’s offer:

- The advertised high ($10K) spending limit could get some people into trouble

- The offer is like a secured card in that you have to pay your balance each week

- The company’s communication and transparency could use some work

However, the benefits seem like they might outweigh the risks for those who need to build out their credit profile. And, this is a legal offer from a legitimate company. So, if you’re in need of a credit builder option, Tomo might be a good choice.

For more information on that topic, I recommend Credit Secrets, as it’s the best credit-building program I’ve ever heard of, and it’s absolutely inexpensive for the amount of value it provides.

And, if you’re interested in learning how you can obtain up to $100K in business credit (that won’t show up on your personal credit report) in as few as 30 days, start here.