Download Your Free, Business Credit Application Template

*This template is intended for informational purposes. All legal documents should be reviewed by an attorney before use, and terms should be defined to protect you in the event of default.

Download your free, printable business credit application template so you can extend credit to your customers, or just find out what a business credit application looks like.

Business Credit Workshop coaching students get access to hundreds of actual business credit applications used by banks across the US.

Most of the time, we focus on ways to improve credit profiles and obtain business credit. But, many of our readers, members, and students run B2B operations that serve other businesses. So, it’s crucial that we understand the ins and outs of extending credit to our business clients and customers… when the opportunity arises.

If you offer your business customers the chance to buy now and pay later, you open a portal to attract more high-ticket sales from those that might not otherwise be able to afford a product or service in a single payment. Plus, by extending lines of credit or private tradelines, you can increase total profits by way of interest and fees.

Or, if you’re just curious about what to expect when you start applying for business credit yourself, this information (and the downloads above) can be helpful.

Here, I provide a breakdown of the essential elements of a business credit application. Finally, I’ll answer some frequently asked questions and provide guidance for new creditors, including options to create online business credit application forms.

- What is a Business Credit Application?

- Here’s How to Create an Online Credit Application Form

- How Should You Ask a Customer to Fill Out a Credit Application?

- Don’t Forget to Do These 3 Things When You Offer Credit to Your Customers

- Summary

Now, let’s get cracking.

What is a Business Credit Application?

A business credit application is a form that enables a registered entity to apply for a line of credit, term loan, revolving tradeline, or a private net 30 account. It collects identifiable information about the business to determine its creditworthiness.

A business credit application serves dual purposes:

- Gather personal, business, and financial data about the applicant

- Serve as a contract between the applicant and creditor

A credit application is considered a legal document, as it should ask for the applicant’s signature. Hence, once signed, and if all terms and conditions are properly outlined in the document, it is legally binding.

Any company that extends credit to their customers needs an application form to weed out those who would not be eligible for any type of financing.

Fundamentals of a Business Credit Application

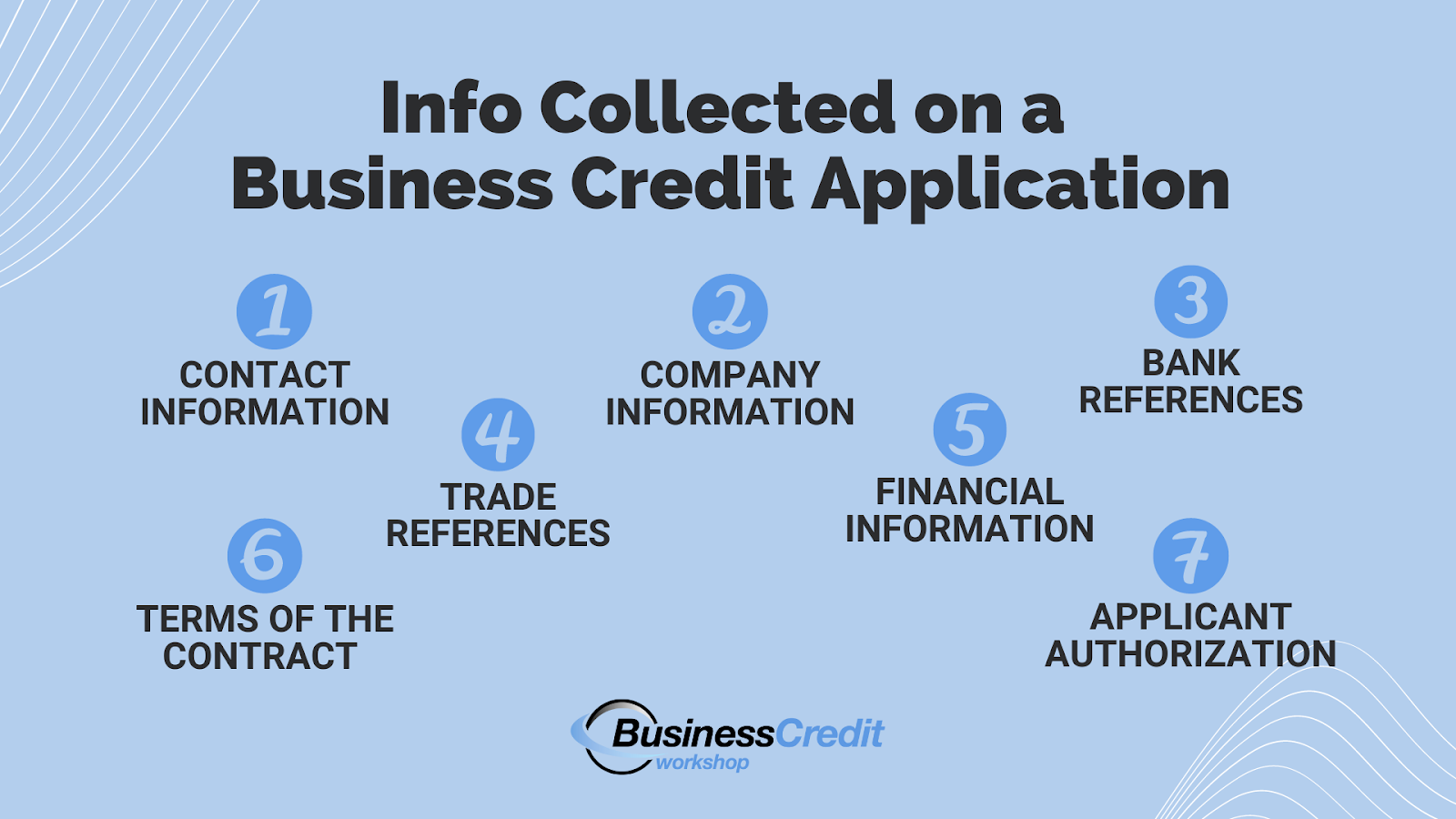

To make an informed determination whether or not a company is worthy of business credit, you need specific identifying information.

- Contact Information

- Full Name

- Professional Title

- % Ownership in Business (Most creditors require at least 50%)

- Company Name

- Tax ID or SSN

- Personal Address (Street, City, State, Zip)

- Business Phone Number

- Business Email Address

- Company Information

- Type of Business

- Years in Operation or Business Start Date

- Business Address (Street, City, State, Zip)

- Legal Entity Type (Proprietorship, Partnership, LLC, Corporation)

- State Registered in

- If DBA or Subsidiary, Parent Company Name & Business Start Date

- Name of Principal Responsible

- Principal’s Address (Street, City, State, Zip) & Phone Number

- Name of any Co-Principal Responsible (optional)

- Co-Principal’s Address (Street, City, State, Zip) & Phone Number

- Bank References

- Checking Account (Bank Name, Account No., Contact Info)

- Savings Account (Bank Name, Account No., Contact Info)

- Credit Line (Bank Name, Revolving/Term, Account No., Contact Info)

- Trade References (Most creditors ask for at least three)

- Company Name

- Contact Name

- Company Address

- Company Phone Number

- Account Age or Account Open Since

- Credit Limit

- Current Balance

- Financial Information

- Amount of Credit Requested

- Total Business Assets

- Total Business Liabilities

- Annual Net Income

- Yes or No: Have Any Officers Filed a Bankruptcy Petition?

- Yes or No: Is Your Company Subject to Any Litigation? (+Explanation)

- Contract Terms

- Terms of use

- Interest and Fees

- Penalties for Noncompliance

- Additional Forms Required (Articles of Organization, etc.)

- Disclosure of Credit Pull

- Applicant Authorization

- Applicant Full Name

- Legal Business Name

- Applicant Signature & Date Signed

(and/or)

- Company Seal & Date Stamped

Once the applicant has submitted their app– assuming it appears they have what it takes, and that you would extend them credit — you’ll need to verify their information and move through the rest of the process.

Here’s How to Create an Online Credit Application Form

In place of or in addition to a paper, pdf, spreadsheet, or doc application, you might want to offer your customers the option to fill out an online credit application form(this is super helpful, especially when applicants are not local).

So, here’s the scoop. There are multiple ways to create online forms, but here’s what I recommend.

i. Use Google Forms

Google Forms has a straightforward user interface and simple design. While it’s not super customizable, it will get the job done, and it’s free for Google Workspace users — both free, personal accounts and business accounts.

ii. Use Jotform

Jotform is another option — super easy to use — that is free for up to 5 forms and 100 monthly submissions. It’s more customizable than Google forms, with integrations with other platforms you might use like PayPal, Google Sheets, Adobe Sign, and HubSpot. It can cost up to $99 per month, depending on your usage

iii. Use Your Website’s Form Builder

If you’re already collecting customer information via contact or subscribe forms on your website, you likely have a form builder that you use. You can probably get into your website dashboard and whip something up based on what you’ve learned here.

There are many other options out there to help you offer an online application — I’ve just found these to be the simplest to use and most reliable.

How Should You Ask a Customer to Fill Out a Credit Application?

If you’re eager to extend credit to customers — perhaps you want to use your credit offer as a highlight to make more sales — you can include your credit option at checkout (in-person or online) or during the sales process, depending on how your operations run.

Service businesses might want to mention their credit application in proposals or bids — at the point just before the sale is made or earlier.

I also recommend that you bookmark or download our trade reference request template and cover letter template (or create your own), because you can share them with your applicants to help them provide you with more information. Then, you can better determine if they meet your requirements for a credit account.

Recommended Reading: Trade References: Learn Everything You Need to Know

Don’t Forget to Do These 3 Things When You Offer Credit to Your Customers

Here are a few tasty reminders with a helping of details for you to munch on.

1. Do Your Due Diligence and Be Selective

The application form is only the first part of a credit application. If you are going to extend credit to your business customers, it’s so important to make sure that you verify everything that the applicant tells you.

Double-check credit report information with Dun & Bradstreet (D&B), Experian Business, and Equifax Business. Pull personal credit reports if you’re wary. Call the references applicants list on their app. Be 100% sure that someone is honest and qualified before you trust anyone in a buy now, pay later situation.

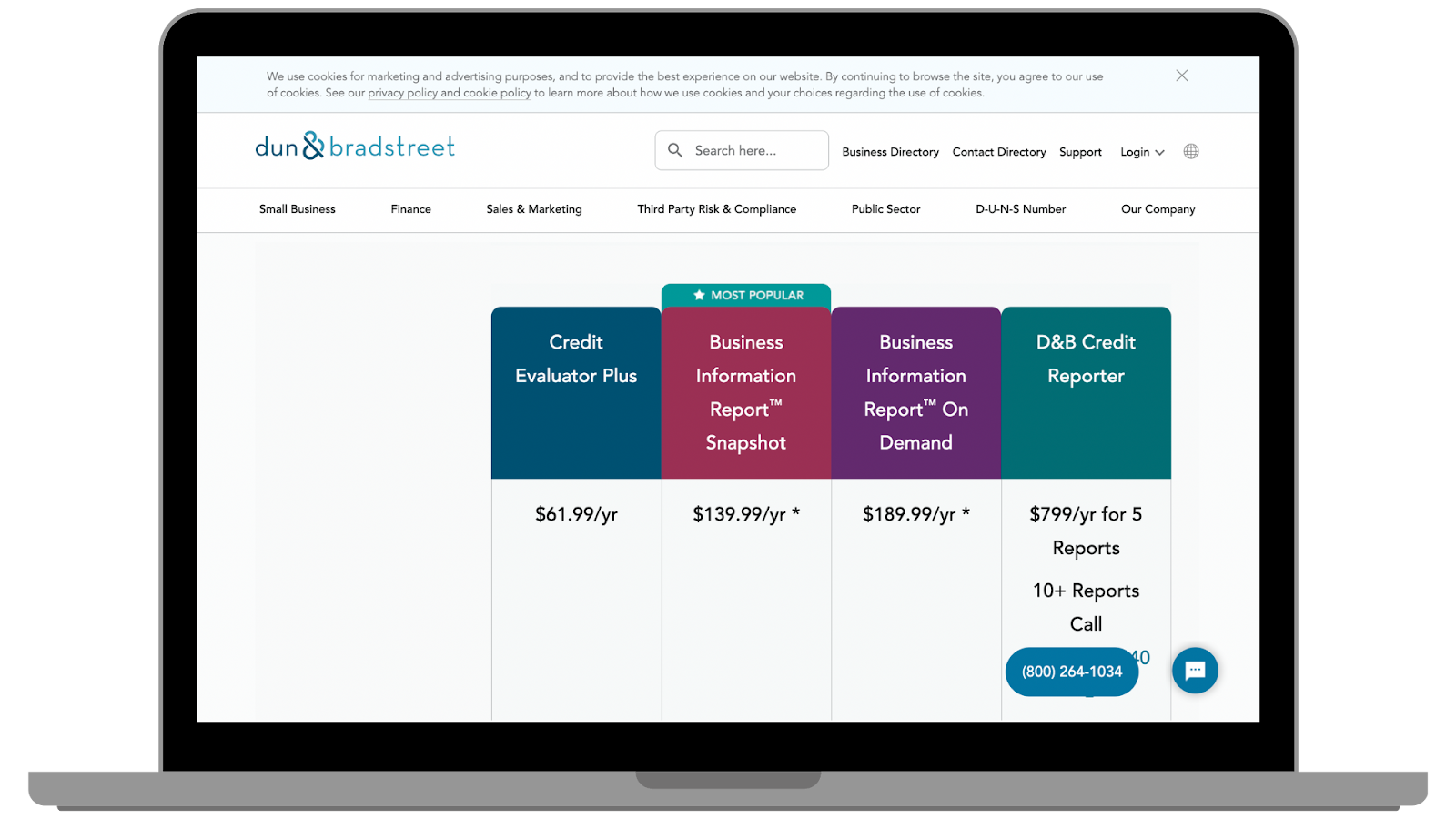

How to Pull a Business Credit Report From D&B

To get a full D&B credit report and PAYDEX Score, visit D&B’s website and select your plan. It will cost from $61.99 to $799 per year, depending on how many reports you will need.

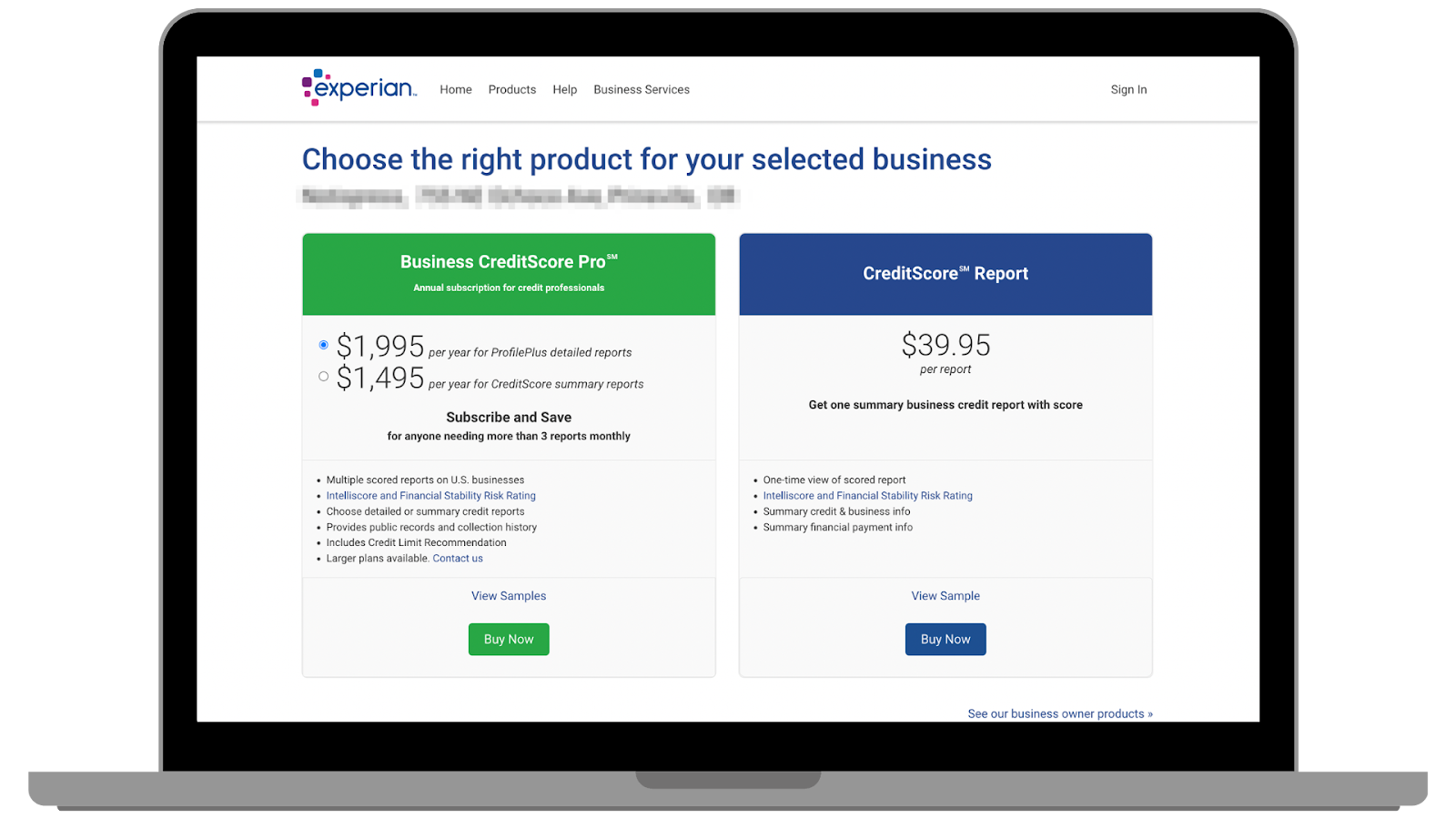

How to Pull a Credit Report From Experian Business

To obtain an Experian Business credit report, go to Experian’s website, search for the business (be sure to select Other Business), and choose whether you would like a one-time report for $39.95 or $1,495 to $1,995 per year (for anyone who needs more than three reports monthly).

How to Pull a Credit Report From Equifax Business

To receive an Equifax Business credit report, visit Equifax’s website and fill out the contact form on the Small Business Credit Report page to connect with the sales team — they can hook you up with the right plan.

2. Consider Reporting Payments to Business Credit Bureaus

As a courtesy to your customers and other creditors, consider reporting on-time payments to the business credit bureaus. Doing so will help your customers establish and grow their business credit profile, and can be a selling point that places you ahead of your competitors.

Furthermore, reporting slow, late, or missed payments help protect other businesses (like yours) from disreputable companies that tend to stiff their creditors on payments.

So, you might want to consider reporting on-time payments to D&B, Experian Business, Equifax Business, and Creditsafe — this typically requires that you join their trade exchange programs.

How to Report On-Time Payments to D&B

To report account activity to D&B, you must either be a part of their DNBi or PPP programs or join the trade Exchange Program. To sign up for D&B’s Trade Exchange Program, you need at least 300 active credit customers.

To apply, either visit D&B’s website or call 1-844-201-9144 to speak to your relationship manager.

How to Report On-Time Payments to Experian Business

Experian doesn’t charge creditors for reporting, but they have requirements such as, members must report a full portfolio monthly. To become an Experian reporting partner, shoot an email to bisdatareporting@experian.com.

How to Report On-Time Payments to Equifax Business

You can register to report payments to Equifax via the registration page on their website or by calling 1-800-831-5614 (Select option three to speak to the correct department).

How to Report On-Time Payments to Creditsafe

Creditsafe is not the most popular business credit reporting solution, and will never hold more weight than one of the primary bureaus. Still, third-party data continues to become more and more desirable to creditors. So, after you pull an Experian Business or Equifax Business credit report, you might also pull from Creditsafe.

Why I mention them here, is because you can join their Trade Exchange Program a bit easier than the other bureaus… and they can automate reporting through your accounting software. Here’s how to leverage the program:

- Claim your company on Creditsafe’s directory

- Login to your Creditsafe account

- Authorize your accounting or ERP software

Many popular accounting tools will easily integrate (Xero, Quickbooks, and Freshbooks, to name a few). If the platform doesn’t integrate with your software, or if you don’t use accounting software, you can still manually report.

3. Enlist a Third-Party App or Platform to Manage Your Credit Program (At Least Think About it)

If the sole reason you want to offer business credit is to get more high-ticket sales, and you have no desire to earn income from fees and interest, explore your options for third-party credit offers, since they will make your job so much easier.

Your choices vary greatly and depend on your business offer. For example, check out Affirm, Klarna, and Afterpay to see if your business might qualify to offer customers their buy now pay later terms — if so, they will do everything for you.

If you do want to manage your credit program, it’s a good idea to explore debt collection offers so that you might outsource that portion of your work (I can almost guarantee you will have to collect on missed payments at some point).

Summary

To extend business credit to your customers, you can use the business credit application template at the top of this page to get started — note that all legal documents should be reviewed by an attorney. And, printable applications are great, but so are online applications.

If you’re just starting down the path to offering business credit to your customers, remember to do your due diligence and verify everything on the application. Think about reporting on-time payments to business credit bureaus. And, consider enlisting help from third parties (if you can find an offer that meets your needs).

Do you have a customer or client who didn’t quite meet the mark and got rejected for a line of credit through your program? Invite them to join Business Credit Workshop to learn how to boost their business credit score and obtain up to $100K in business credit in as few as 30 days.