I first discovered FairFigure when writing up my most recent post, a comprehensive Fidextech review. I found it so interesting that I put it at the top of the list to research next. Now, here’s everything I know.

Let’s take a look at what FairFigure is, see an overview of company leadership, and explore the features of the card in detail.

This is what’s in store:

- What is FairFigure?

- FairFigure Capital Card Features

- FairFigure Partnership Opportunity

- Conclusion: Is FairFigure Legit?

Now, let’s roll!

What is FairFigure?

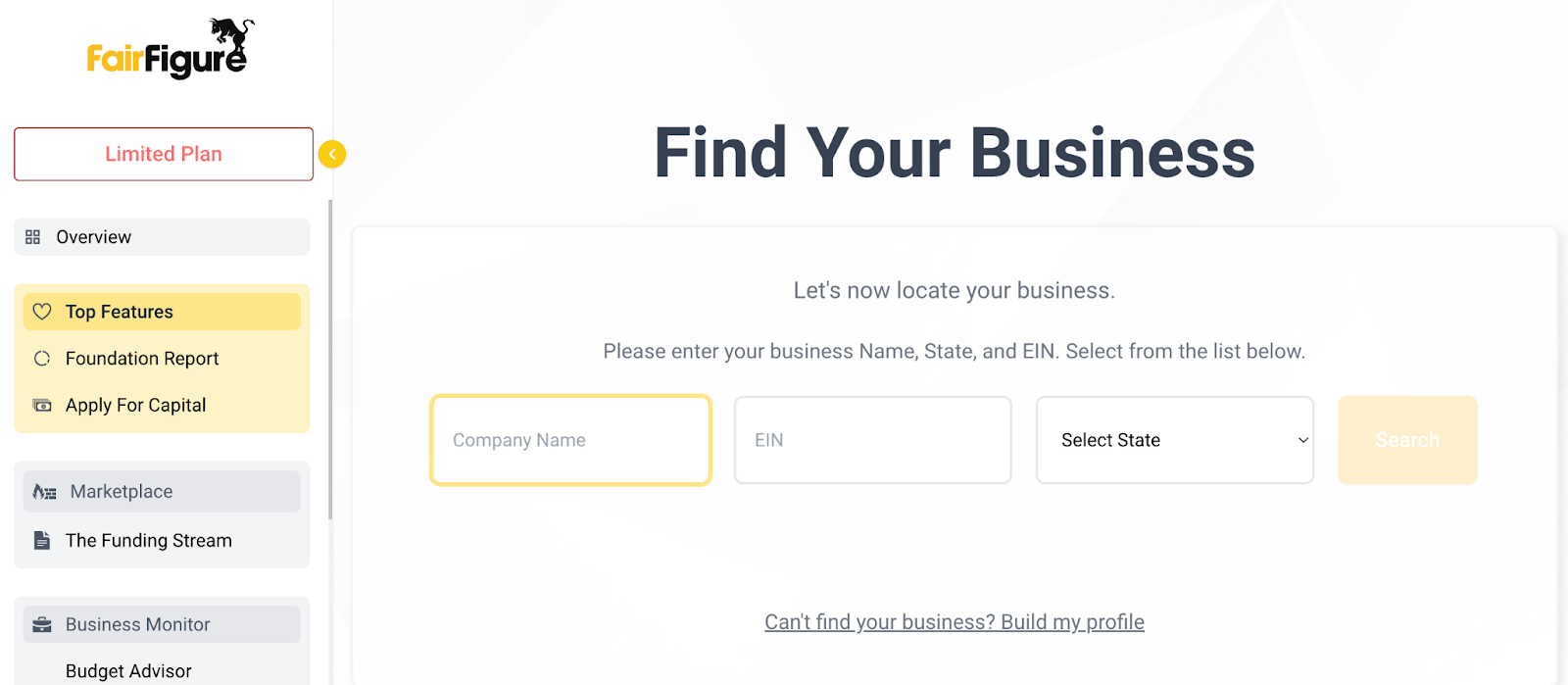

FairFigure is a platform designed to help small business owners build, monitor, and improve your business credit. They offer a service that allows you to track both your business and consumer credit scores in real time. It includes features like a Business Credit Correct tool that helps identify and fix incorrect information.

FairFigure also offers the FairFigure Business Capital Card, which you can use to get funding without personal credit checks or personal guarantees.

Key features include:

- Business and consumer credit monitoring.

- FairFigure Capital Card that helps build credit while providing same-day funding.

- Payment reporting to commercial credit bureaus.

- Identity Theft Protection and Darknet Scanner to help secure your company.

With FairFigure, there are no personal credit checks for funding or credit applications, since they rely on business EINs instead. The company positions itself as a tool to help businesses grow by helping them improve credit scores and secure better funding options.

You might also like: Low-Risk NAICS Codes +Best SIC Codes for Business Credit in 2024

Company Overview

FairFigure Capital LLC is a Fort Lauderdale-based company that was founded in 2021 by Dana Angelino. Angelino happens to own and co-own several other companies, including numerous net 30 offers that help people build business credit.

His other businesses include:

- Crown Office Supplies

- Shirtsy

- Signsy

- Greentees

- Coconut Bikinis

- A few others

So, FairFigure’s founder is as informed as anyone could be about the business credit building market and net 30 offers. Other than a bank executive, I can’t think of a better background for a business credit builder company leader.

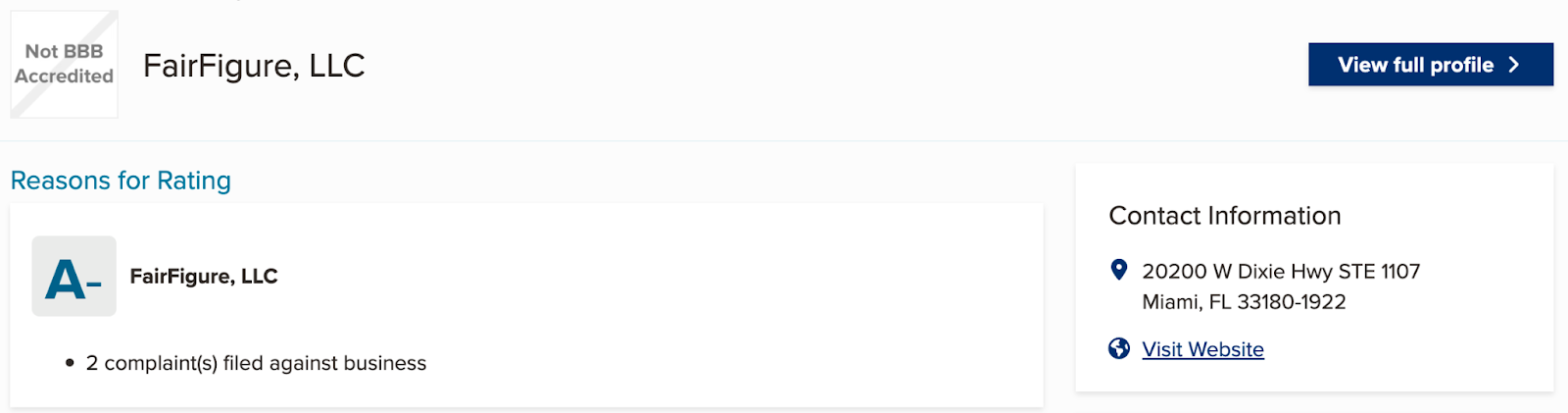

While FairFigure is not Better Business Bureau-accredited, they have an A- rating on the platform, with minimal complaints and a handful of positive reviews from satisfied users.

I didn’t find any FairFigure reviews on Trustpilot, mentions on Reddit, or staff reviews on Glassdoor. Most of the reviews I did find appeared to be affiliate reviews, so I assume they were somewhat biased.

Without ever having applied for the card myself, I can only say that, if I were a betting man, I would wager that the company is trustworthy based on what I know about its leadership.

With that said, I did notice something about the offer that is quite misleading. FairFigure claims to offer cashback on card purchases.

However, while I was searching for the cashback amount, I came across a blog post on the official website that states: “Instead of cash back, [the FairFigure Capital Card] benefits primarily revolve around your credit.”

I’m not a fan of deceptive messaging or brands with a lack of transparency, so this doesn’t sit so well with me. But, even without cashback, the offer is worth taking a look at.

You might also like: 41 Companies That Help Build Business Credit [Beyond Net 30 Vendors]

FairFigure Capital Card Features

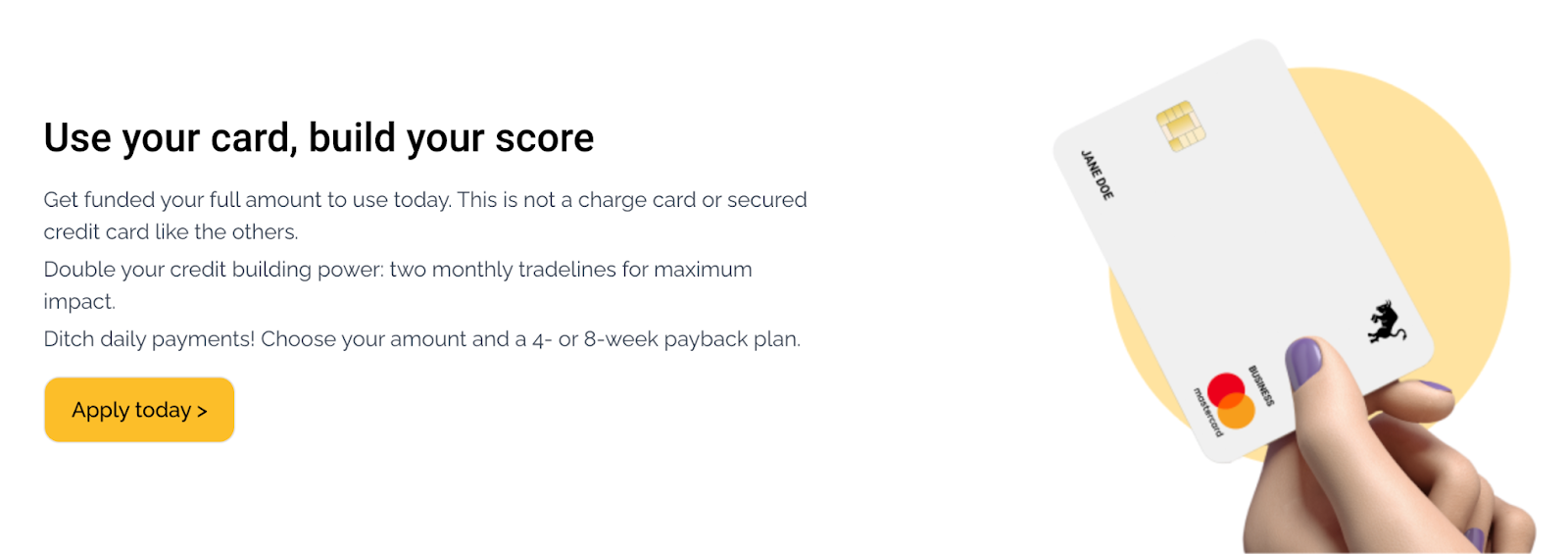

The FairFigure Capital Card is a “no PG” (no personal guarantee) business credit builder card. It lets you apply using your company’s EIN, which allows you to build business credit without personal credit checks or guarantees.

The card offers:

- Flexible four or eight week repayment terms.

- Credit monitoring tools.

- Identity theft protection.

- Reporting to commercial credit bureaus.

Moreover, it provides funding based on business revenue and reports payments to key business credit bureaus, which helps boost your credit score. Ultimately, it’s designed to separate personal and business finances, which makes it practical for small businesses that want to build credit and access funding.

Note, funds must be repaid in full within the payback terms you choose—It’s more like a corporate card, not a credit card.

Recommended: Business Credit Cards You Can Get Without a Personal Guarantee

1. No Personal Guarantee

You don’t have to worry about personal credit checks or guarantees when you apply for the FairFigure Card—This keeps your personal and business finances separate, which reduces the risk to your personal credit score and assets.

No PG business credit offers are perfect for businesses that want to build credit solely through their EIN.

You might also like: Here’s How to [Actually] Get Business Credit With Just an EIN +More Options

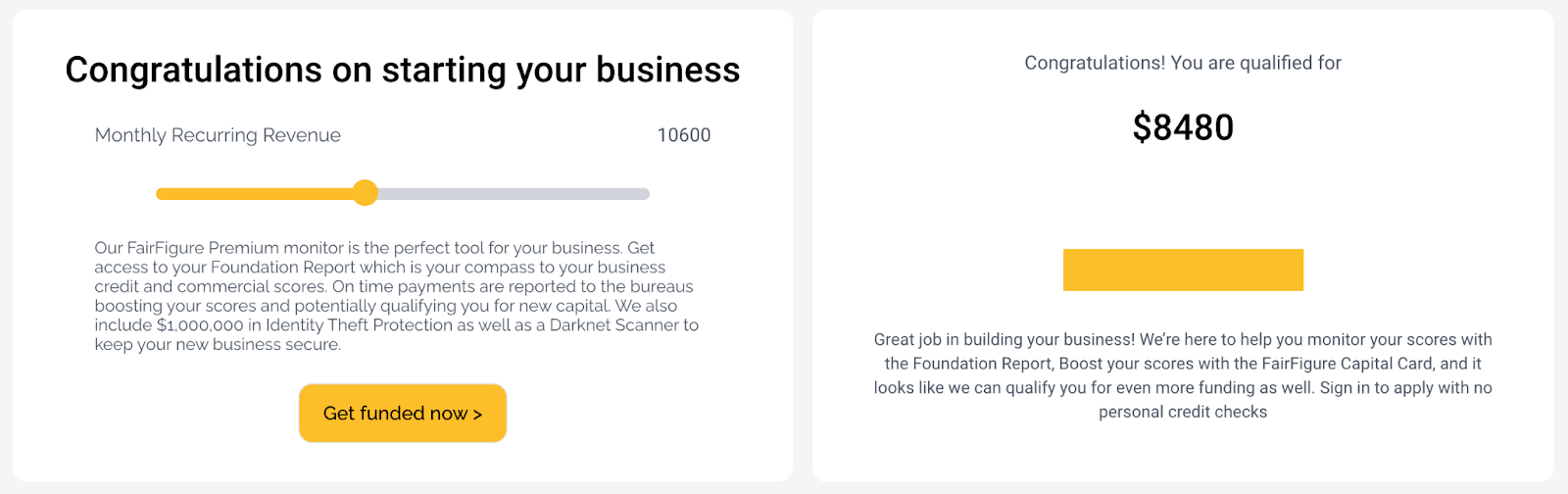

2. Adjustable Spending Limits

Your spending limit with FairFigure is based on your business revenue. For example, if your business meets the qualifications, you could start with a $1,000 limit. As your revenue grows, so does your spending power.

So, if your business brings in $10K in monthly revenue, you might qualify for an $8K limit. The scalability allows you to extent your purchasing power as your business expands and gives you access to more capital when needed.

3. Net 30 or Net 60 Repayment Terms

Net 30 or net 60 terms refer to how much time you have to pay back what you’ve borrowed. With FairFigure’s card, you can choose either 30 or 60 days to pay your balance in full.

If you choose net 30, you’ll need to pay off your card in full within 30 days of making a purchase. And, if you choose net 60, you have 60 days.

4. Personal and Business Credit Monitoring

For $30 per month, FairFigure offers business credit monitoring that helps you track your financial health.

FairFigure monitors business credit scores from:

- Fundex

- CreditSafe

- Equifax

And, provides consumer credit monitoring from:

- Equifax

- Transunion

- Experian

This service not only keeps you updated on your credit scores but also reports your $30 monthly subscription as a separate vendor tradeline.

So, paying for the monitoring service helps build your credit faster by adding an extra positive payment to your business credit report.

5. Identity Theft Protection

With the $30 credit monitoring subscription, FairFigure includes $1 million in identity theft protection to safeguard your business. You’ll also benefit from a Darknet scanner that alerts you if your business’s sensitive information is exposed.

With this added security, you can focus on growing your business without the worry of identity theft.

Recommended: 14 Best Credit Monitoring Services for Scores, Reports, & ID Theft Protection

6. Reporting to Business Credit Bureaus

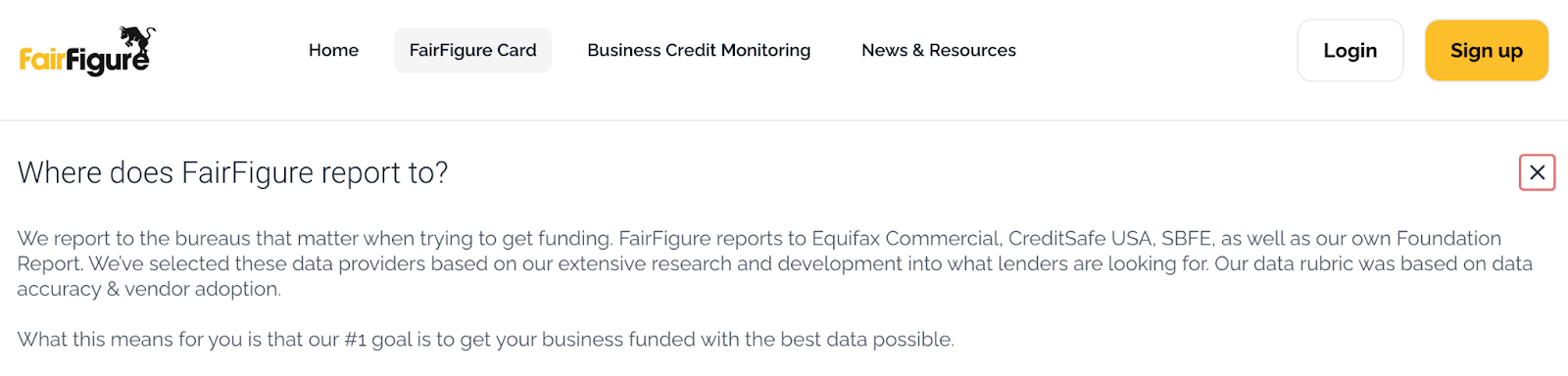

According to FairFigure’s official website, they report data to:

- Equifax Commercial

- CreditSafe USA

- SBFE

- Their own Foundation Report

So, you can get your credit monitoring and FairFigure card payments reported to these bureaus.

However, there is no current indication that FairFigure reports to Experian Business or Dun & Bradstreet. This may change, so it’s a good idea to check their official website for the most up-to-date information.

You might also like: Everything You Need to Know About a DUNS Number – and Why You Should Care

FairFigure Partnership Opportunity

Again, I first learned about FairFigure through Fidextech, a web design and marketing agency that offers FairFigure net 30 terms to their clients, which caught my attention.

Through the affiliate program, you can earn up to $120 for each client or customer who signs up and is approved for the FairFigure Capital card. The card allows you to offer net 30 terms to your clients who can then pay you while building positive payment histories.

The program supports new businesses by establishing their profiles with credit bureaus and helps most business owners get approved for at least $1,000 in initial funding.

You might also like: A Complete Fundwise Capital Review: Should You Use Their Business Funding Services?

Conclusion: Is FairFigure Legit?

So, can you really build business credit that easily with FairFigure? It’s a bit more complex than a simple yes or no. While FairFigure offers two tradelines—the Capital Card and the monitoring service—these alone may not be enough to significantly boost your business credit.

Still, you can use the FairFigure card to pay your other tradelines, which might be super helpful. Keep in mind that paying $30 for credit monitoring is optional and may not be necessary on the business credit building journey; there are other ways to track your credit without this added expense.

Ultimately, FairFigure provides some solid tools, but building substantial business credit often requires more than just these offerings. Consider your options carefully before you dive in.

Want to learn how to obtain up to $100K in business credit in as few as 30 days? Join Business Credit Workshop today!