Key Takeaways

- Ava credit builder helps improve your credit by reporting payments to all three major credit bureaus.

- They offer a “high-limit” virtual card, capped at $2,500.

- Payments and credit usage are tracked to help boost your credit score.

- No credit check is required, and approval happens after linking your bank account.

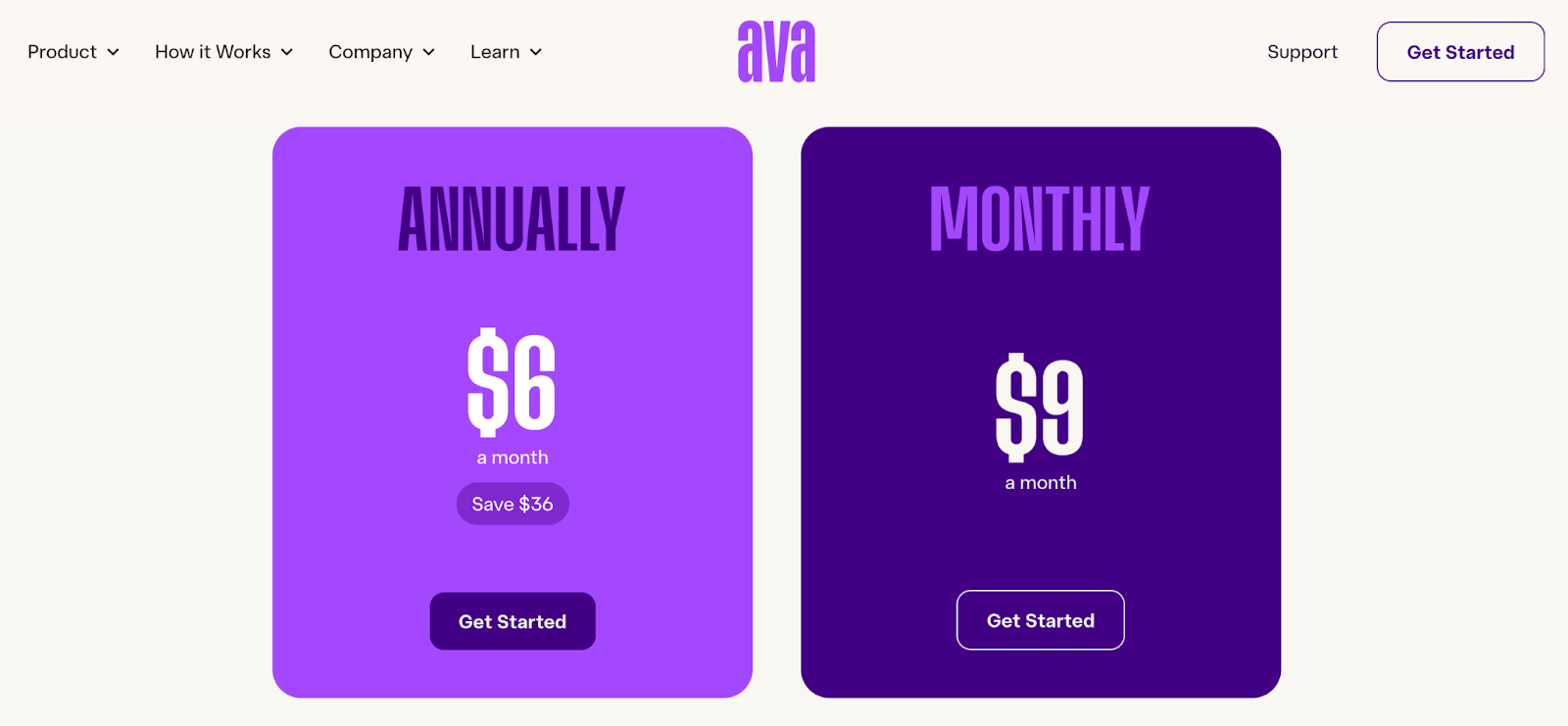

- There’s a monthly subscription fee of $6 (annual plan) or $9 (month-to-month).

- Ava allows you to pay subscriptions with a virtual card and automate payments.

- Account includes a Save & Build account to save money while building credit.

The Ava card is a contemporary offer that promises to help consumers build credit. The promise is that you can use the fee-free card to pay your subscriptions, save money each month, and cash out with a lump sum at the end of the year with a higher credit score. But, is it really all it’s cracked up to be?

Here, we’ll take a look at the full offer from Ava – the card, subscription autopay, credit builder savings account, and the potential implications of taking advantage of it. We’ll even peek behind the curtain at the company behind the product.

This is what’s in store:

- What is the Ava Card & Ava Credit Builder?

- Ava Card Benefits & Features

- Frequently Asked Questions

- Conclusion: Does Ava Help Build Credit?

Now, let’s roll.

What is the Ava Card & Ava Credit Builder?

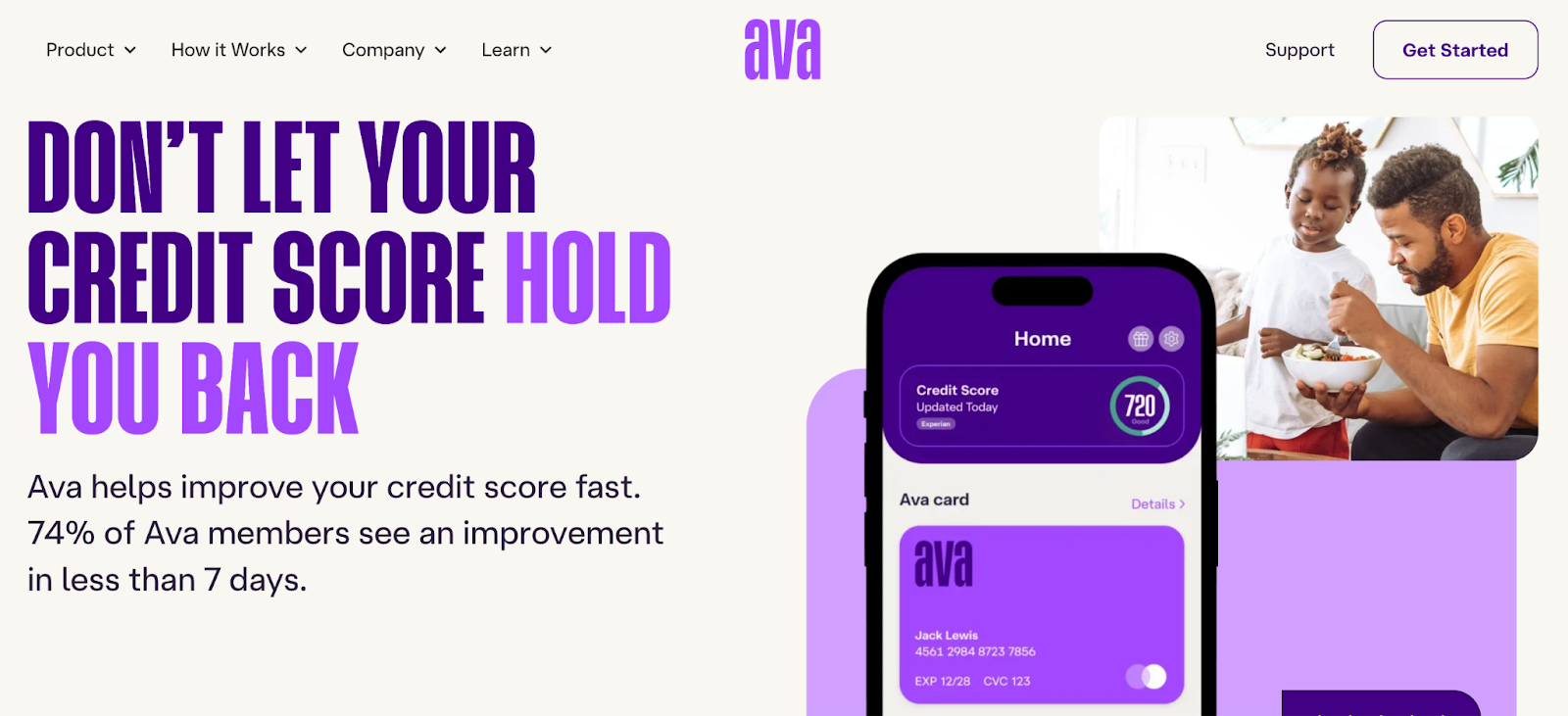

The Ava card is a spending card that can be used with Ava credit builder—a financial tool designed to help people improve their credit scores. It functions as a credit-building program that offers an alternative to traditional credit cards. With Ava, there’s no need for a credit check, and there are supposedly no interest charges or fees associated with the card.

Once you sign up and link the bank account where your paycheck is deposited, you can apparently receive instant approval. You’ll then receive a “high-limit” Ava credit builder card that you can pay your monthly subscriptions with.

How Does Ava Work?

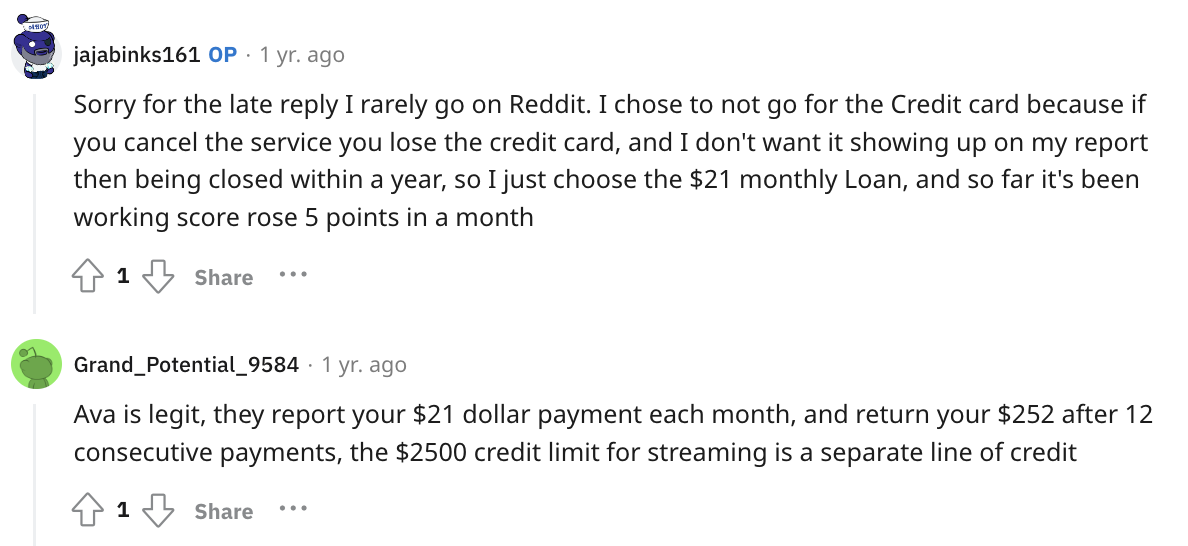

Payments through the Ava card and monthly payments into a Save & Build savings account are reported to credit bureaus to potentially boost your credit score over time. Plus, after 12 months of making payments into the Save & Build account, you’ll get all your money back.

You might also like: Cred AI Review: Are You Really Better Than Your Bank?

How Much Does Ava Credit Cost?

While Ava advertises that there are “no fees” for using the card, it’s not exactly free. Ava charges a $6 per month subscription fee for those who sign up for an annual plan. If you prefer a month-to-month subscription, the fee is $9 per month.

Ava notes that achieving a credit score of 700 or higher can potentially save you over $3,000 annually—Having a high credit score can help you get lower insurance rates and help you qualify for better terms on financing, but the amount you can actually save is relative to your situation and any financial products you’re interested in.

Still, $9 bucks a month is less expensive than a lot of comparable offers on the market.

You might also like: Is Credit Strong Legit? A Complete Personal and Business Credit Builder Review

Company Overview

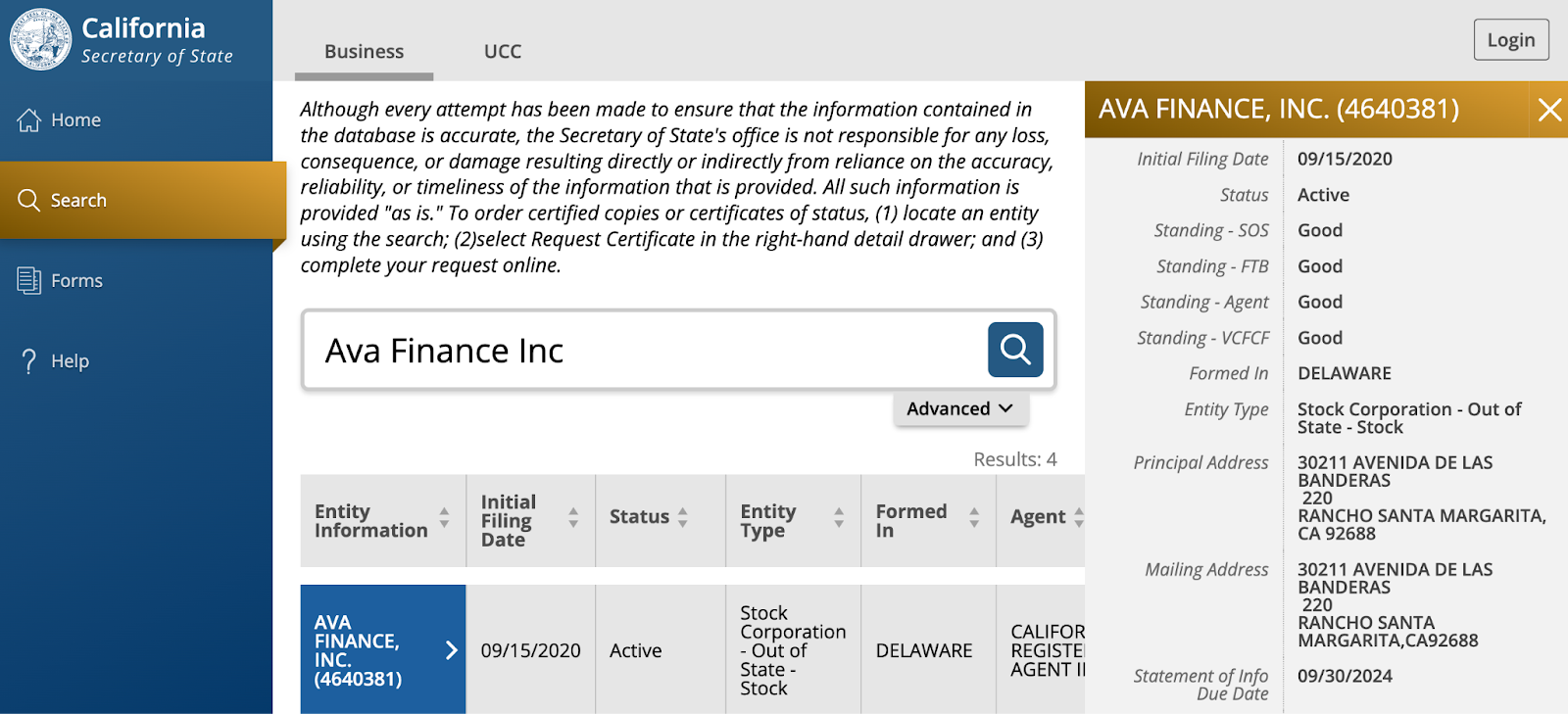

Ava Finance Inc. is a San Francisco-based, privately-held, for-profit company that was founded in 2020 by Abed Lawand, Omar Sinno, and Reza Rahman. The company is legally registered, active, and in good standing in the state of California.

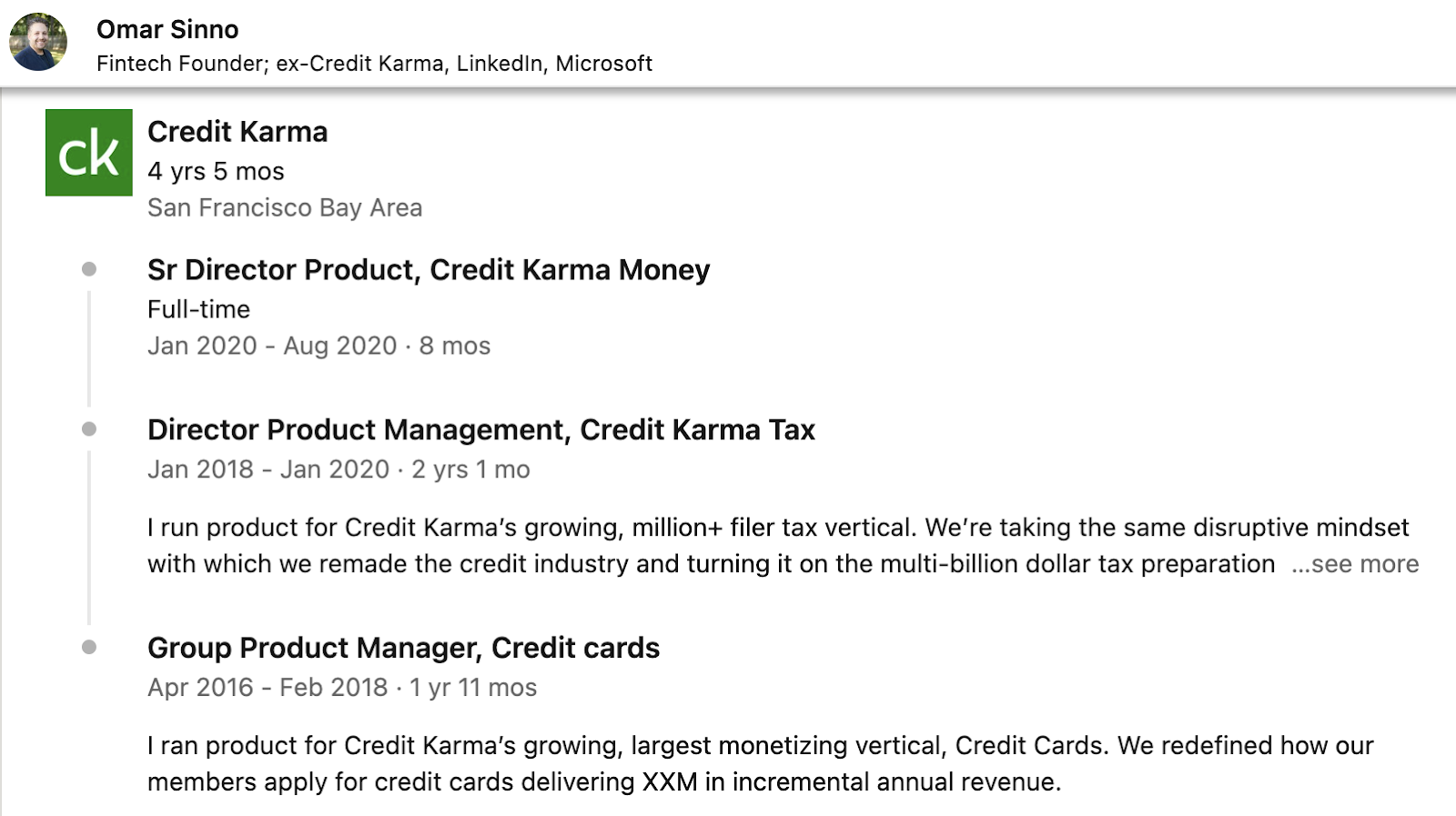

Prior to launching Ava credit builder – the current CEO – Sinno was the senior product director at Credit Karma® for nearly 5 years, the senior product manager at LinkedIn® for three years, and co-founder of other various businesses.

Next to his career history, Sinno’s education in software engineering and business make him a natural choice to lead the company.

Plus, Trustpilot reviewers rate the company as excellent with 4.8 stars across the board. Most users cite the fact that their credit scores jumped quite a bit within a short amount of time when they signed up.

However, the Better Business Bureau (BBB) tells a slightly different story. Users rate the company as 3-star with more than a handful of complaints closed within the last year. They have been accredited with BBB since 2022, and have an A- rating. But, they’re only showing 3 out of 5 stars.

This really isn’t that bad, considering lots of financial companies have hundreds of BBB complaints. And, people tend to flock to this particular platform when they have a bad experience.

After a quick search, I found no lawsuits against Ava Finance Inc., open or otherwise.

In all, it seems to be a reputable company and a trustworthy brand to do business with…if the offer is a good fit for your situation, anyway.

You might also like: 14 Best Credit Monitoring Services for Scores, Reports, & ID Theft Protection

Ava Card Benefits & Features

Compared to the other credit builder platforms that I’m familiar with, the Ava card is a relatively simple offer, which I like. There’s nothing that might confuse some people into signing for added products and services that they don’t need.

And, it’s unique in that it helps people build credit by paying their bills/subscriptions – Netflix, Hulu, Verizon, Allstate…

Overall, Ava credit builder targets key credit factors such as on-time payments, credit utilization, and credit age to help improve your credit score. Learn how it works.

You might also like: 6 Best Fintech Credit Cards to Apply for (Consumer & Business)

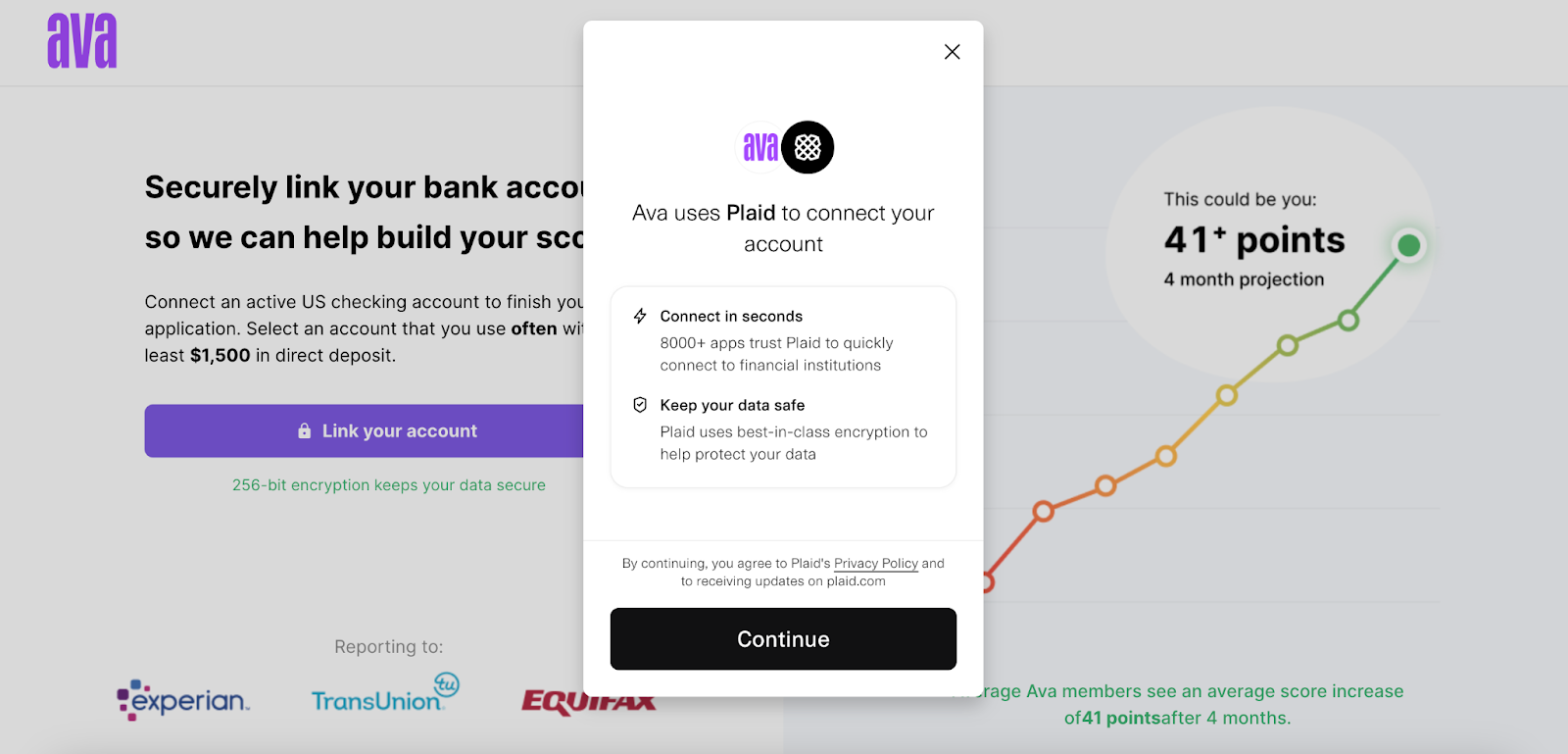

1. Secure Bank Account Connection

When you first log in to your Ava account, you’ll be asked to provide your home address, then connect your bank account. Ava Financial uses Plaid to encrypt the connection and keep your finances secure.

Plaid seems to be a trusted and safe way to share financial data with a company. However, it’s important to be cautious and review the privacy policy and terms of use to understand how your data is handled and protected by both Plaid and the service you’re connecting to.

Ava Finance, Inc. collects and shares personal information based on the product or service you have with them.

This can include sensitive details like:

- Social Security numbers

- Account information

- Credit history

- Transaction records

- Payment history

They share this information for everyday business purposes like processing transactions, reporting to bureaus, and responding to legal inquiries. However, Ava Finance does not share personal information with affiliates for marketing or non-affiliates for marketing purposes.

For questions or concerns about how Ava Finance handles personal information, you can contact them at legal@meetava.com.

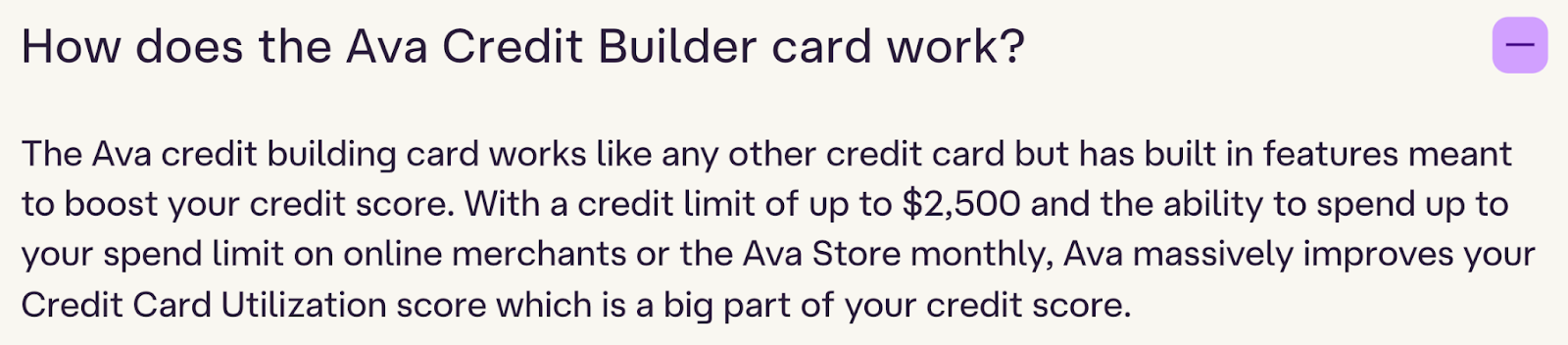

2. The “High-Limit” Ava Card

Ava provides a no interest, so-called, ‘high-limit’ credit card. This card is supposedly designed to lower your credit usage instantly, which should positively impact your credit score.

But, the highest available limit is $2,500. Compared to many starter credit cards that offer $250, $300, or $500, yes, the limit is greater. But, this is not what everyone considers “high,” so it’s worth clarifying.

Ava promptly reports your payments to all three major credit bureaus:

- Experian®

- TransUnion®

- Equifax®

So, your spending will help boost your credit score across all three bureaus. Ava also claims to watch your utilization to be sure you’re not spending more than what credit bureaus consider responsible.

Ava is not a physical card—no Mastercard, no Visa, only a virtual card.

Finally, Ava Financial will report your account within a week of being approved, and will report your payments within 24 hours – most credit cards report on certain dates each month or quarter.

Now, the Ava card can only be used on subscription services in Ava Financial’s partner database. Let’s see who they are.

3. Autopay Subscriptions

Ava Financial partners with 66+ popular subscription services (so far) that allow you to use your Ava credit to pay. And, we’re not just talking about video streaming services—Their ecosystem has a pretty wide range of services.

Partner categories include:

- Gaming

- Health & Fitness

- Kids

- Music & Audiobooks

- Security & Safety

- Shopping

- Streaming TV

- Utilities & Insurance

Enjoy automated payments and reminders to ensure you never miss a subscription payment. The Ava card can help make sure that you pay on-time, and build credit while doing it.

You might also like: Is the National Debt Relief Program Legit? The Honest Answer

4. Save & Build Credit Builder

Ava’s Save & Build account is a pretty typical credit builder savings account:

- You make payments up to $30 into an account every month.

- Your payments are reported to credit bureaus as a loan payment.

- You collect the funds (up to $360) at the end of the 12-month term.

By reporting payments, this should contribute to boosting your credit score…But, if you miss a payment, it will be reported as a negative item. So, be sure you are consistent enough to make the payment every month as agreed before you start the program.

Note: Monthly payments are automated through your bank account.

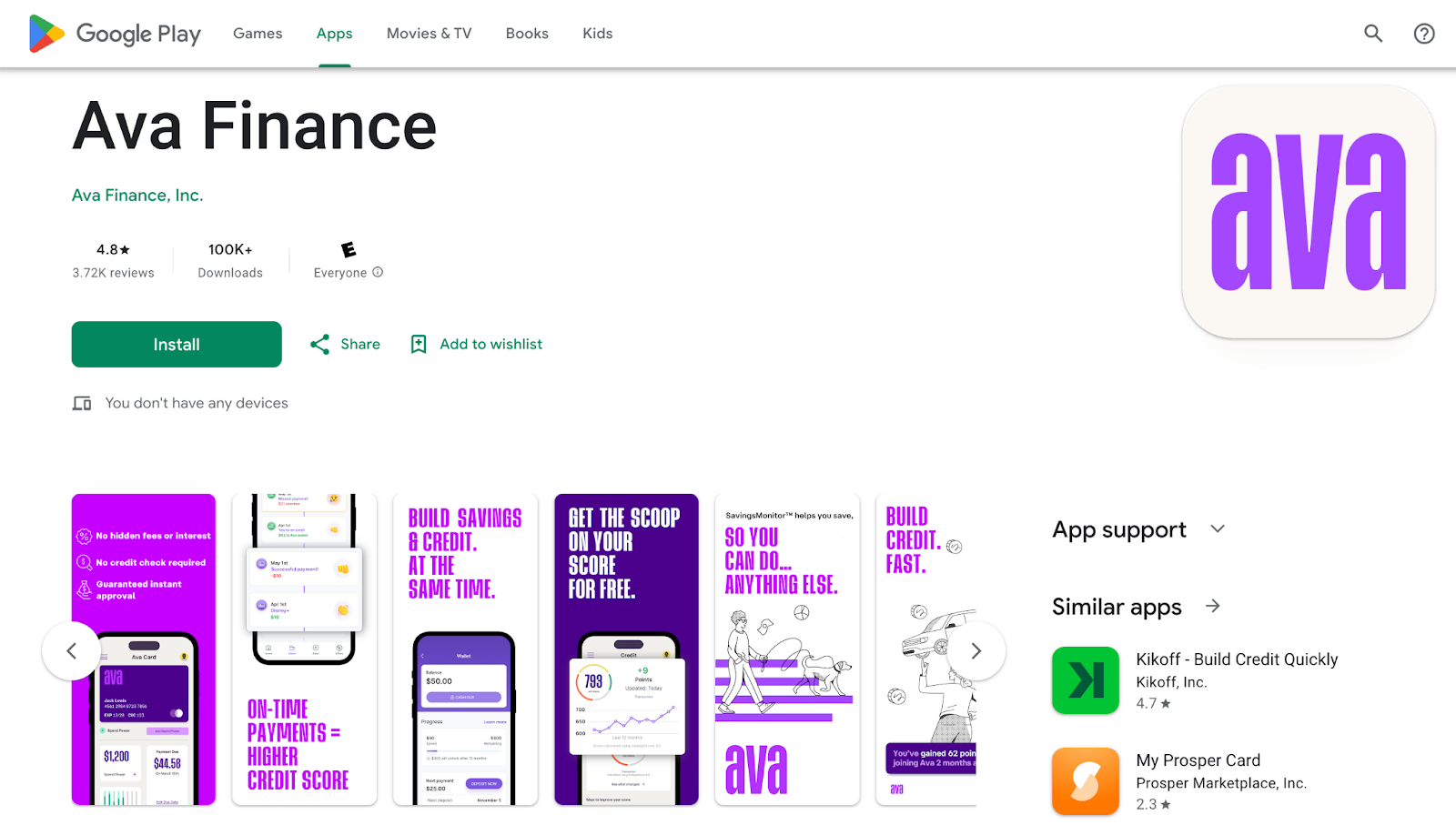

5. The Ava App

Manage all Ava Credit and Ava Save & Build features conveniently through the Ava mobile app. It’s a centralized platform to access and monitor your credit-building progress from your Android or iPhone.

The app maintains a 4.8-star rating on the Google Play store and 4.9 on the Apple Store. The key complaints with the app seem to relate to the user’s lack of understanding about the offer.

Frequently Asked Questions

Is Ava a real credit card?

Ava is a legitimate account that reports payments to credit bureaus, but it is not a traditional credit card. There is no physical card, and payments from a can only be made within Ava Financial’s partner network.

Does Ava report to Experian?

Yes, Ava reports your payment history and credit activity to all three major credit bureaus, including Experian® — They first report within a week of opening an account, then within 24 hours of you making your payments.

How do I cancel my Ava credit card?

To cancel your account contact Ava Finance directly through their customer support channels—Email support@meetava.com or call (920) 287-0282.

Conclusion: Does Ava Help Build Credit?

Whether or not an Ava card can help you boost your credit depends on why your credit score is low in the first place, and whether or not you can make the payments on-time as agreed.

If your score is low because you don’t have any items reporting to the credit bureaus, then, yes, you can use a product like this to boost your score over time. If you need to increase your credit utilization or add a new type of tradeline to your credit mix, the Ava card’s optimized reported utilization might actually help. And, the 12-months savings aspect of a builder loan could be very appealing in the right situation.

However, if your credit score is low because you have negative items reporting, a new credit account isn’t going to help much, if at all. In fact, A credit builder card won’t help you clean up your credit or make debt go away. These situations require customized credit repair solutions.

If you need to fix your personal credit, start learning the right steps from reputable sources — The FTC’s credit counseling guide is a trustworthy place to start.

Do you want to learn how to obtain up to $100K in business credit in as few as 30 days? Join Business Credit Workshop today!