When you start any business in New Jersey, it’s crucial to make sure you’re fully insured. Some types of coverage are required for businesses in our state and others are elective but beneficial. Meanwhile, depending on your scope of products and services, some insurances might be completely useless.

Find out which coverages are necessary, which ones are generally helpful, and some that could be a wasted expenditure for certain businesses. Then, get answers to some of the most common questions small business owners in New Jersey have about insurance.

Here’s what’s in store:

- What is Small Business Insurance?

- What are the Requirements for Business Insurance in New Jersey?

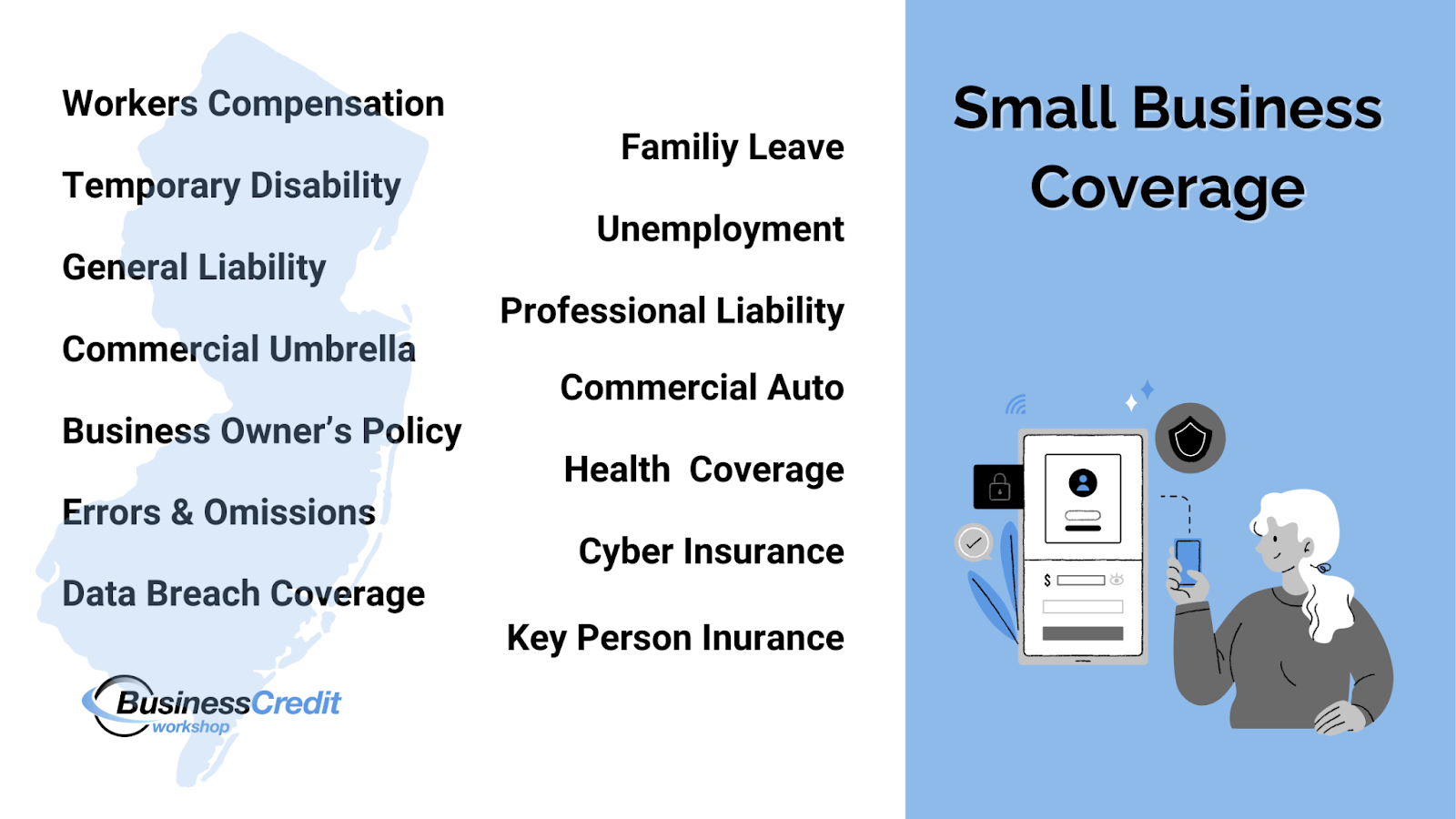

- Small Business Coverage Types You Need to Understand

- 1. Worker’s Compensation Insurance

- 2. Family Leave Insurance

- 3. Temporary Disability Insurance

- 4. Unemployment Insurance

- 5. General Liability Insurance

- 6. Professional Liability Insurance

- 7. Commercial Umbrella Insurance

- 8. Commercial Auto Insurance

- 9. Business Owner’s Policy (BOP)

- 10. Employee Health Insurance Coverage

- 11. Errors & Omissions Insurance

- 12. Cyber Insurance

- 13. Data Breach Insurance

- 14. Commercial Property Insurance

- 15. Key Person Insurance or Corporate-Owned Life Insurance (COLI)

- Business Insurance Providers in New Jersey

- Frequently Asked Questions

- Final Takeaway

Now, let’s get moving!

What is Small Business Insurance?

Small business insurance is like a safety net for your business—you know, just in case things don’t go as planned. It’s there to help cover your back when unexpected events come knocking. Basically, it’s a bundle of different insurance policies tailored to fit the needs of small businesses like yours.

With small business insurance, you’re not just protecting your business’s physical assets; you’re also safeguarding yourself from:

- Liability claims

- Employee injuries

- Legal hassles

Think of it as a shield against the unknown, to give you peace of mind knowing that you’re covered no matter what life throws your way. Whether it’s property damage, a slip-and-fall accident, or a lawsuit from a disgruntled customer, having the right insurance can make all the difference.

So, while it might seem like any other expense, small business insurance is typically a smart move to protect what you’ve worked so hard to build…But, that depends on whether you need the specific coverage.

You might also like: Low-Risk NAICS Codes +Best SIC Codes for Business Credit in 2024

What are the Requirements for Business Insurance in New Jersey?

So, when it comes to running your business in New Jersey, there are a handful of insurance requirements you need to keep in mind to cover both you and your employees.

Let’s break it down:

- Most businesses, except for sole proprietors with no employees, need Workers Comp. Check with your insurance provider or the Compensation Rating and Inspection Bureau for details.

- If you’ve got employees, you need to follow the New Jersey Family Leave Act. This means they can take leave for things like caring for a new child or a family member with a serious health issue. You will need coverage to fund this.

- You’ve also gotta pay disability insurance taxes and provide info when employees need to file for disability benefits. You can choose coverage through the state plan or a private one.

- And, you need to have unemployment insurance – It helps workers who lose their jobs or work less than full-time due to lack of work.

- While it’s not a must by state law, offering health or life insurance to your employees is typically a good move. You can find resources through the Department of Banking & Insurance or the state’s health insurance marketplace.

- If you’ve got 20 or more employees with health benefits, you also need to offer continuation of coverage under federal law (COBRA) – Smaller businesses have state continuation options.

Additional types of coverage may be needed based on industry requirements and business needs. Review New Jersey’s employer requirements to understand what the state expects from you.

Note: Effective January 8, 2024, businesses with outstanding liabilities for wage, benefit (including insurance infractions), or tax law violations risk being placed on the Workplace Accountability and Labor List, “The WALL.” If your company is listed on the wall, you’ll be ineligible for public contracting opportunities with State, county, or local governments until all liabilities are settled.

For help making sure you’re in compliance with workplace laws, you can reach out to the New Jersey Department of Labor at wagehour@dol.nj.gov.

You might also like: Sole Proprietorship VS LLC: How to Choose Your Entity Wisely

Do small businesses in NJ have to offer health insurance?

Small businesses in New Jersey are not legally required to offer health insurance to their employees. Unlike some states that have specific mandates for employer-sponsored health insurance, New Jersey does not have such requirements for small businesses.

So, the decision for a small business (with fewer than 50 employees) to offer health insurance is typically voluntary and depends on factors like your budget and desire to attract and retain talent.

In New Jersey, the Small Business Health Options Program (SHOP) is a handy tool for small businesses with 1–50 employees. SHOP helps you offer private insurance to your team. And, you can usually enroll any time of year.

You may want to offer health insurance as part of your employee benefits package because:

- Health insurance can make your company more competitive in the job market and help attract and retain qualified employees.

- Providing health insurance demonstrates your commitment to employee well-being and can lead to higher job satisfaction and staff morale.

- You may qualify for tax incentives, such as the Small Business Health Care Tax Credit, if you offer health insurance to employees – this might save you up to 50% of what you contribute as an employer.

- Access to health insurance can help your employees stay healthy and address medical issues promptly, which could lead to fewer missed days and increased productivity.

If you choose to offer health insurance, work with insurance brokers or agents to explore available options and find coverage that meets your needs and budget.

What is the Minimum Liability Insurance in New Jersey?

If you’re cruising around the Garden State, you gotta have liability insurance with minimum coverage limits of 15/30/5. That means $15,000 for each person injured in an accident, up to $30,000 per accident for bodily injury, and $5,000 for property damage.

If you’re running a business, you’ll need workers’ comp insurance to take care of your employees if they get injured on the job – this includes behind the wheel. The coverage amounts depend on things like your payroll and what your business is all about.

While it’s not a must-do by law, having general liability insurance is a smart move for businesses. It helps cover you if there are claims of injury, property damage, or other mishaps.

Remember, the exact coverage you need can vary, so it’s best to chat with an insurance expert to make sure you’ve got the right protection for your situation.

You might also like: How to Use Business Gas Cards to Build Your Business Credit

Small Business Coverage Types You Need to Understand

There are many types of small business insurance coverage that you should be familiar with, whether you currently need it or not. If you employ others to work for you in New Jersey, you undoubtedly need at least a handful of these coverage types.

And, depending on your operations, you could need any of these policies (now or in the future) to protect certain aspects of your company.

You might also like: Everything You Need to Know About a DUNS Number & Why You Should Care

1. Worker’s Compensation Insurance

Worker’s Compensation Insurance is a must if you have employees. It kicks in to cover medical expenses and lost wages if an employee gets injured or sick on the job. It’s there to protect both you and your workers, ensuring they get the care they need while shielding you from potential lawsuits.

- You need it if: You hire employees in the state of New Jersey.

- You don’t need it if: You run a sole proprietorship or single-member LLC with no employees.

2. Family Leave Insurance

Family Leave Insurance is crucial for offering your employees the support they need during significant life events. It allows them to take time off for the care of a new child or a family member with a serious health condition, without worrying about job security.

- You need it if: You hire employees in the state of New Jersey.

- You don’t need it if: You run a sole proprietorship or single-member LLCs with no employees.

3. Temporary Disability Insurance

Temporary Disability Insurance ensures that if one of your employees falls ill or gets injured and can’t work, they’re still covered financially. It helps them with wage replacement during their recovery period, easing their financial burden.

- You need it if: You hire employees in the state of New Jersey.

- You don’t need it if: You run a sole proprietorship or single-member LLCs with no employees.

4. Unemployment Insurance

Unemployment Insurance provides a safety net for your employees if they lose their jobs through no fault of their own. It’s a legal requirement to have this coverage, helping your former employees bridge the gap until they find a new job.

- You need it if: You hire employees in the state of New Jersey.

- You don’t need it if: You run a sole proprietorship or single-member LLCs with no employees.

5. General Liability Insurance

General Liability Insurance is like a safety net for your business. It covers legal costs and damages if someone is injured on your property or if you or your employees cause damage or injury to someone else.

- You need it if: You run a business, regardless of size or industry.

- You don’t need it if: You don’t run a business.

6. Professional Liability Insurance

Professional Liability Insurance, also known as Errors & Omissions Insurance, is essential for professionals who provide services or advice. It protects you from claims of negligence or mistakes in your work that result in financial loss for your clients.

- You need it if: You are a professional who offers services such as consultant, accountant, lawyer, or healthcare provider.

- You don’t need it if: You do not provide professional services.

7. Commercial Umbrella Insurance

Commercial Umbrella Insurance provides an extra layer of liability coverage beyond the limits of your other insurance policies. It’s like a safety net for your safety net, offering additional protection when your other coverage maxes out.

- You need it if: You might benefit from extra liability coverage, especially if your business operates in high-risk industries.

- You don’t need it if: Your general liability and/or professional liability coverage is adequate.

8. Commercial Auto Insurance

Commercial Auto Insurance is a must-have if your business owns vehicles used for business purposes. It covers damages or injuries resulting from accidents involving your company vehicles.

- You need it if: You own or lease vehicles that are used for business purposes.

- You don’t need it if: You don’t own or use vehicles for work.

9. Business Owner’s Policy (BOP)

A Business Owner’s Policy (BOP) bundles several types of insurance, including property, liability, and business interruption insurance, into one convenient package. It’s a cost-effective way for small businesses to get essential coverage.

- You need it if: You’re looking for comprehensive coverage at an affordable price and can qualify.

- You don’t need it if: You run a larger business with more complex insurance needs.

10. Employee Health Insurance Coverage

Employee Health Insurance Coverage is crucial for attracting and retaining top talent. It provides medical coverage for your employees and their dependents, ensuring they stay healthy and productive.

- You need it if: You want to offer competitive benefits to employees or you employ more than 50 full-time equivalent employees.

- You don’t need it if: You have no employees – Companies with fewer than 50 full-time equivalent employees aren’t required by law to offer health insurance, but it’s still a valuable perk.

11. Errors & Omissions Insurance

Errors & Omissions Insurance, also known as Professional Liability Insurance, is essential for professionals who provide services or advice. It protects you from claims of negligence or mistakes in your work that result in financial loss for your clients.

- You need it if: Professionals such as consultants, accountants, lawyers, and healthcare providers.

- You don’t need it if: Businesses that don’t provide professional services may not need this insurance.

12. Cyber Insurance

Cyber Insurance is becoming increasingly important in our digital world. It protects your business from financial losses and liabilities resulting from cyberattacks, data breaches, and other cyber incidents.

- You need it if: You store sensitive data or rely on digital systems to conduct business.

- You don’t need it if: You do not store sensitive data or digital systems in your operations.

13. Data Breach Insurance

Data Breach Insurance is a specialized form of insurance that covers the costs associated with data breaches, including notification expenses, credit monitoring services, and legal fees – it is related to cyber insurance, but doesn’t provide the same coverage.

- You need it if: You store any sensitive customer or employee data online.

- You don’t need it if: You have no customer or employee data stored online.

14. Commercial Property Insurance

Commercial Property Insurance protects your business property, including buildings, equipment, and inventory, from damages or losses due to covered perils such as fire, theft, or vandalism.

- You need it if: You own or lease property for business purposes.

- You don’t need it if: Your business has no valuable, insurable real estate or assets.

15. Key Person Insurance or Corporate-Owned Life Insurance (COLI)

Key Person Insurance, also known as Corporate-Owned Life Insurance (COLI), provides financial protection to your business in the event of the death of a key employee. People used to sometimes call this type of coverage, “dead peasant life insurance” 🤮– But, in practical use, It helps cover the financial losses and expenses associated with losing a key member of your team.

- You need it if: You rely heavily on key employees or individuals whose loss would have a significant financial impact on your business.

- You don’t need it if: You have no employees or “key persons” within your operations.

Business Insurance Providers in New Jersey

When you’re looking for small business insurance in New Jersey, you have a few options. Some types of insurance can be found through official state programs, while others are available from insurance providers or brokers. Let’s break it down for you:

- State insurance programs – These are programs set up by the state of New Jersey to offer specific types of insurance for businesses. They’re meant to be easy to access and affordable, giving you insurance that fits your needs.

- Private insurance providers – These companies (think Insureon, Progressive, or The Hartford) sell insurance directly to businesses. They offer different types of coverage like liability or workers’ compensation insurance. They handle everything from creating policies to dealing with claims.

- Insurance brokers – Brokers are like middlemen between you and insurance providers. They help you figure out what kind of insurance you need and then find the best policies for you. They’re experts at navigating the insurance world and can help you find the right coverage.

When you’re deciding between state programs, private insurance providers, and brokers, think about how much help you want.

If you’re comfortable doing things on your own, you might go straight to an insurance provider. But if you want someone to guide you through the process, a broker could be really helpful – Either way, the goal is to get the insurance that keeps your business safe.

Frequently Asked Questions

How much does business insurance cost in NJ?

The cost of business insurance in New Jersey varies based on the size of your business, the type of coverage you need, and your industry. Generally, small businesses might pay anywhere from a few hundred to several thousand dollars per year.

Why is business insurance so expensive?

Business insurance costs can seem high because it’s designed to protect your business from a wide range of risks, including property damage, liability claims, and employee injuries. Factors like the size of your business, the industry you’re in, and your claims history can also impact the cost.

Do I need insurance for my LLC in NJ?

While New Jersey doesn’t require all LLCs to have all types of insurance, you likely need to get certain types of insurance. For example, if you have employees, you need to provide workers comp, family leave, disability, and unemployment coverage.

Which insurance company is best for small business?

The best insurance company for your small business depends on factors like the type of coverage you need, your budget, and your preferences. It’s a good idea to compare quotes from multiple insurers to find the right fit. You may want to use a combination of state programs and private insurance providers.

Is business insurance a startup cost?

Yes, business insurance can be considered a startup cost because it’s necessary for protecting your business from risks right from the beginning. It’s an investment in your business’s security and can provide peace of mind as you grow.

Final Takeaway

Starting and running a business in New Jersey comes with its fair share of risks, but having the right insurance can help mitigate those risks and protect what you’ve worked so hard to build.

From workers’ comp to cyber Insurance, understanding the different types of coverage available and which ones are essential for your business is key to safeguarding your assets and ensuring your peace of mind.

Remember, while some insurance types are required by law, others are optional but highly recommended – Know what you need and what you don’t to save you time and money and protect your assets.

Take the time to assess your needs, explore your options, and invest in the protection your business deserves. With the right insurance in place, you can focus on growing your business with confidence, knowing that you’re prepared for whatever challenges may come your way.

Want to learn how to obtain up to $100K in business credit in as few as 30 days? Join Business Credit Workshop today!