Over a year ago, I first planned to share an X1 Card review with readers. The name has been getting a ton of hype. For a while there, it left us all wondering, ‘When will X1 be available?’ Well, it’s official; as of last season, the offer has launched and you can now apply.

So, here’s what I know about the novel credit card offer from X1 — the good, bad, and the ugly — use this info to decide if you should apply.

| *Note that everything listed here is subject to change by the respective card issuers. Always do your due diligence before you apply for any financial offer. |

- What is an X1 Visa Credit Card?

- How is X1 Different From Other Credit Card Offers? And, How is it the Same?

- The Features & Benefits

- 1. Pay No Annual Fee

- 2. Carry a Stainless Steel Card

- 3. Create Multiple Virtual Cards

- 4. Add Family Members to Your Account

- 5. Earn 2X+ Rewards on Every Purchase

- 6. Get Up to 10X (Non-Taxable) Points for Referrals

- 7. Leverage an Array of Insurance & Protections

- 8. Receive Up to 5X Higher Spending Limits

- 9. Get Approved With An Attainable Credit Score

- The Drawbacks

- The Features & Benefits

- X1 Company Overview

- Frequently Asked Questions

- Conclusion: Is X1 Really “the Smartest Credit Card Ever Made?”

What is an X1 Visa Credit Card?

The X1 card is a new, personal Visa credit offer that is intended to extend higher spending limits to those with lower credit scores (and higher incomes). The offer comes with some shiny features beyond that.

Originally, the X1 card was expected to launch in Winter 2020. As we all know, this was not a great year for new businesses, as there were some significant setbacks.

Well, the X1 card weathered the storm and announced its launch in July 2022, which opened doors for its 500K-person waitlist and the general public.

Rather than apply, the website calls new visitors to “Order” a card, which may sound gimmicky. However, this is simply a copywriting decision — no tricks here. You will still need to apply. And, while your credit score won’t be the only determining factor, it will play into the decision somewhat.

How is X1 Different From Other Credit Card Offers? And, How is it the Same?

In a nutshell, the X1 card is built for people with higher incomes and lower credit scores than traditional credit card offers, and it comes with a range of benefits.

From virtual cards to rewards and protection, this offer has quite a bit going for it. In some ways it’s different, and in other ways no better than other credit cards. Let’s explore the X1 offer in full so you know all the ups and downs, what’s different and what’s not, before you apply.

The Features & Benefits

First, let’s take a look at the advantages of becoming an X1 cardholder — there really are quite a few.

1. Pay No Annual Fee

Annual fees are just the worst (when you don’t spend enough to get your money’s worth) — thankfully, the X1 card doesn’t have any.

Some favorable X1 reviews have stated that companies with such a “premium-looking” card do not offer zero annual fees, but this isn’t completely true. For example, the Apple Mastercard offers a nice-looking metal card with no annual fee, and there are definitely others out there.

2. Carry a Stainless Steel Card

It’s amazing how many compliments people get on metal cards when they use them to make in-person purchases. And, the X1 card does offer a lightweight, stainless steel card. If you like the idea of carrying a fancy-looking piece of metal to pay for your purchases, then X1 definitely is an option worth considering.

With that said, the material a card is made from has no impact on your spending limits, your credit score, or your ability to leverage credit. This is a vanity feature (nothing wrong with that).

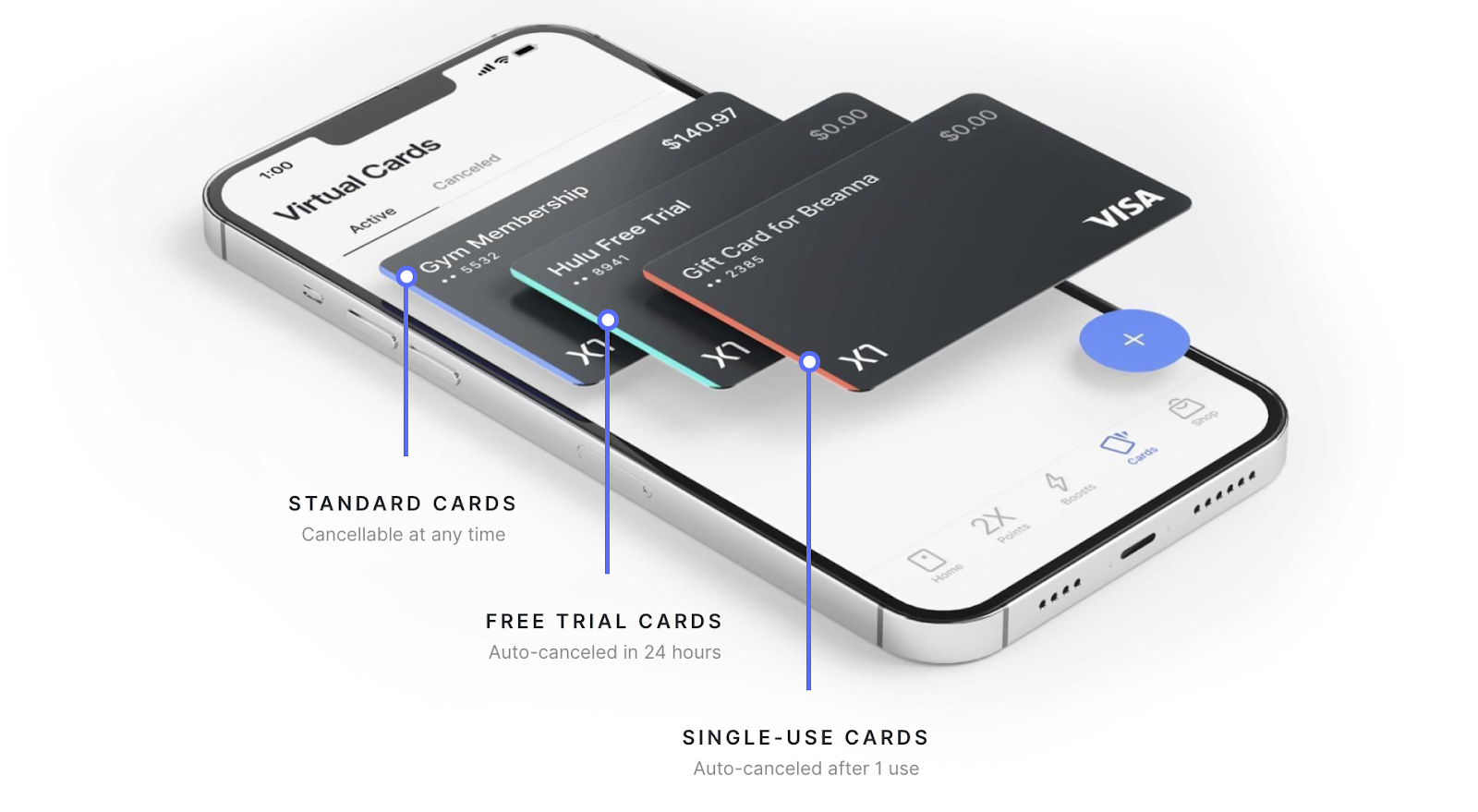

3. Create Multiple Virtual Cards

At some point in our lives, we’ve all had a nasty subscription charge that just wouldn’t go away — virtual cards offer a chance to protect yourself from unwanted spending on your credit card account.

Because the X1 offer includes virtual cards, you can start spending before the metal card arrives. If you haven’t used virtual cards before, they can be exceptionally helpful.

For example, you can create a card for free trial offers so that you aren’t charged a second time if you decide not to continue a subscription or forget to cancel. Or, you can create a single-use card for a one-time purchase like a gift card or other offer from a source you’re not confident about spending with.

Or, if you lose your card, create a new virtual card, and get instant access to it.

I’m going to bring up the Apple Mastercard again because they also offer a virtual card — but currently only allow you to create one at a time. And, when you request a second Apple Mastercard, any autopay accounts connected to the preceding card have to be updated.

Citi’s Double Cash, Diamond Preferred, and Premiere cards offer virtual cards as well, so this isn’t necessarily a breakthrough feature for a personal credit card, but it’s a notable one.

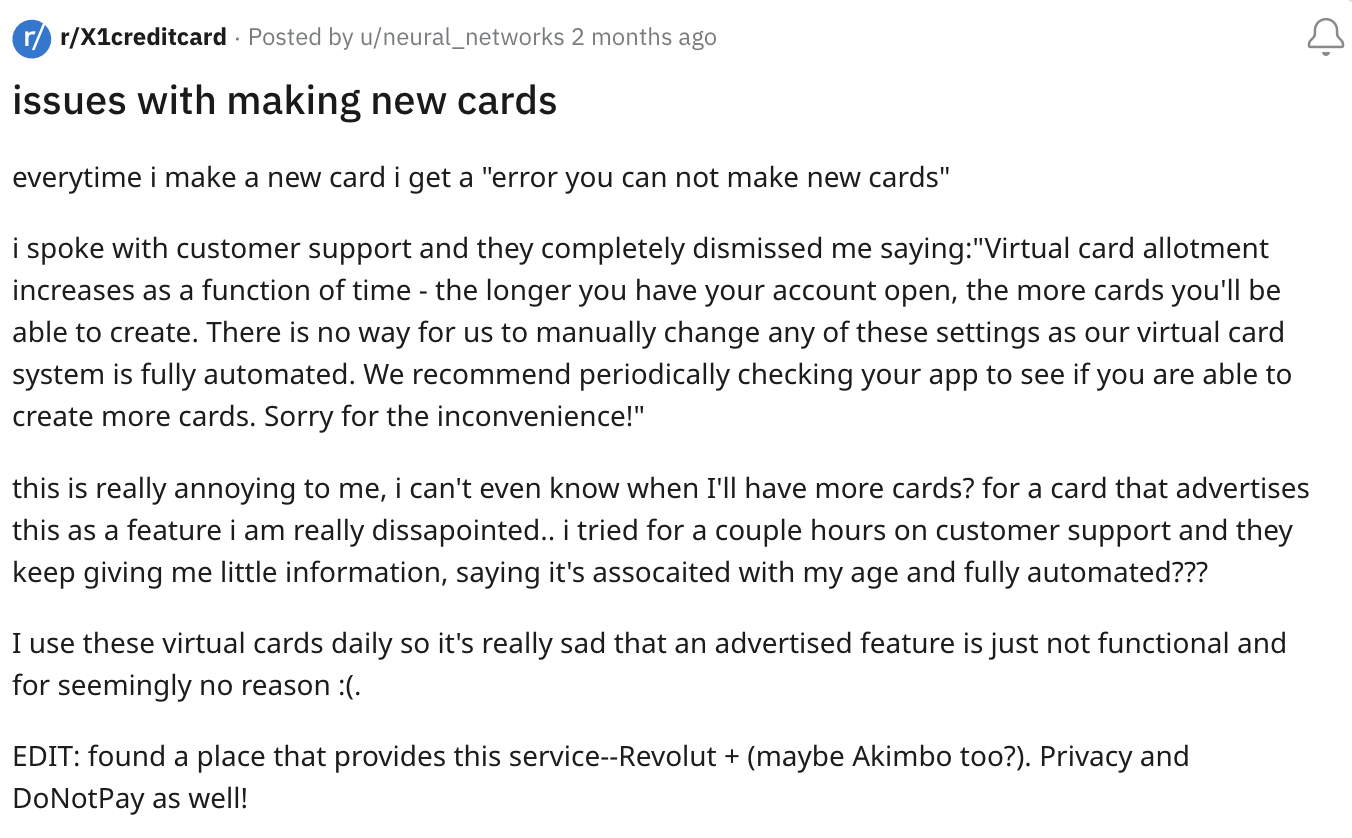

However, this feature comes with limitations.

It seems as though the longer you have an X1 account, the more virtual cards you will be cleared to create. This isn’t really a big deal, though — in the meantime, you can also use a service like Revolut or DoNotPay to help you out with a similar offer.

4. Add Family Members to Your Account

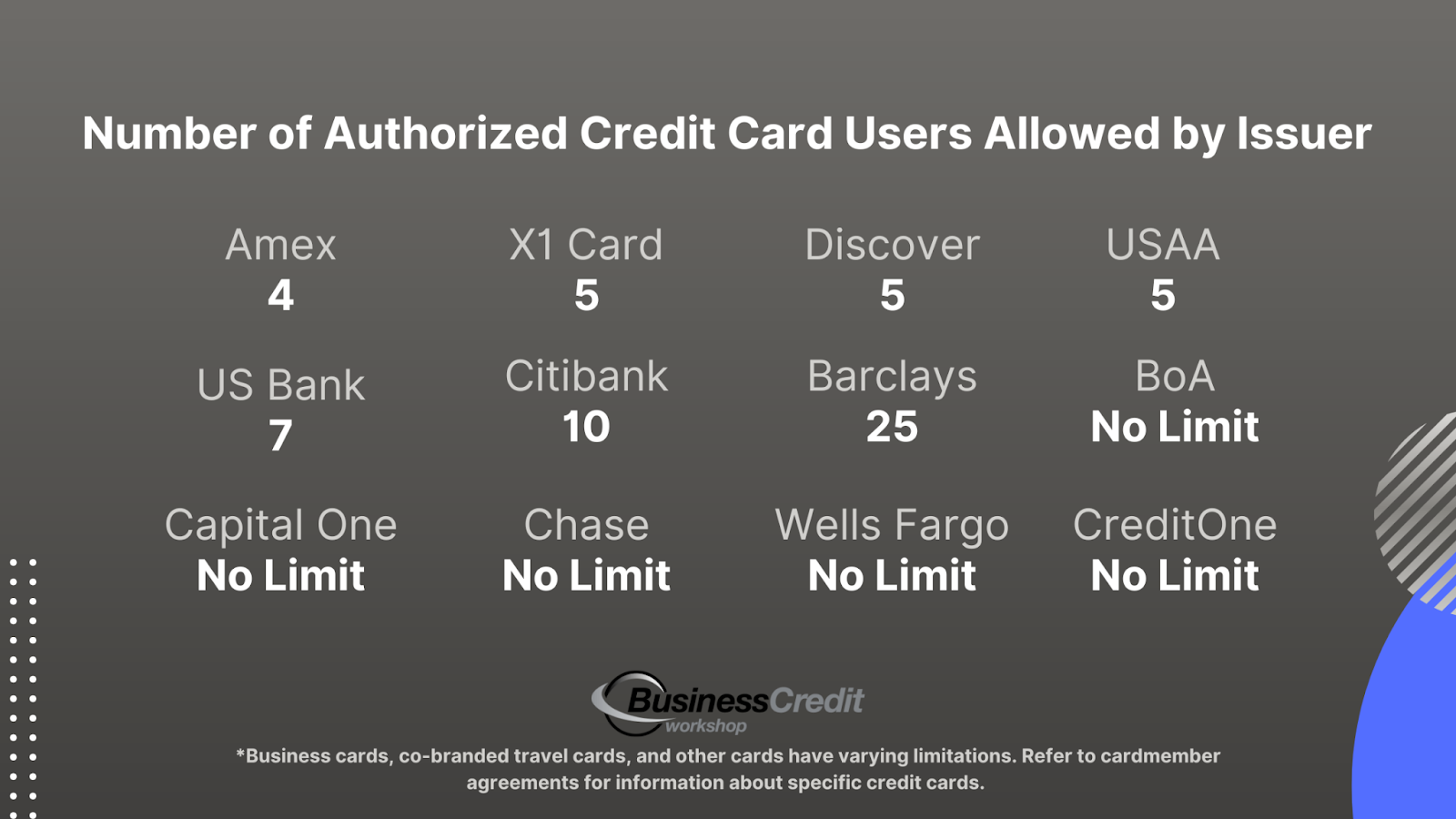

With an X1 card account, you can add up to 5 cardholders to earn points with you. And, there are no age restrictions on the

While this is a benefit to obtaining an X1 card, it’s not a standout feature (but it does outperform Amex). Here’s a breakdown of authorized cardholder limits by issuer.

Furthermore, it’s pretty common to add minor children to a credit card account. When adding a child or other family member to a credit card account, always be sure that they understand how credit works, and you know that you are responsible for payment, no matter who does the spending.

5. Earn 2X+ Rewards on Every Purchase

There are a plethora of personal rewards credit cards on the market, most of them offering lower rewards than the X1 card.

All purchases earn at least 2X points per dollar spent. Cardholders that spend $15K or more in one year on their card will level up to 3X points.

Note that X1 is not the only personal credit card with the equivalent of 2X points on all spending. For example, Wells Fargo Active Cash offers 2%+ cash back on all purchases and Capital One Venture Rewards provides users with 2+ miles per dollar spent.

With that said, there seem to be some hiccups with points redemption.

Rather than simply shop as you normally would with a retailer, you have to use the app to leverage “boosts,” which is what X1 calls their bonus points. I find this to be the case with most credit cards. And, in many cases, you might find better rewards redemption with other cards — it just depends on where you shop.

6. Get Up to 10X (Non-Taxable) Points for Referrals

Like many other credit cards, X1 has a referral program. X1 cardholders who refer a new approved account will receive a “mystery reward multiplier” of 4X, 5X, or 10X for all spending made on the new account in the first 30 days. X1 card referral rewards are non-taxable, originally you could invite up to three friends to apply.

However (this just in), some users have been invited to share unlimited referrals with up to 10x points rewards, which is awesome.

Most other cards offer a flat rate for referrals, which is typically the equivalent of around $100 per approved account. These bonuses often max out around the equivalent of $500 to $2K per year. And, most of these other referral rewards are considered taxable income. With X1, you could earn more (if the new cardholder you refer is a big spender).

7. Leverage an Array of Insurance & Protections

As an X1 cardholder, you’ll have access to quite a few insurance and protection offers.

Here’s a breakdown:

- Cell phone protection – pay your phone bill or purchase your phone with the credit card and quit paying insurance through your carrier

- Trip interruption reimbursement – when you pay for travel with your card, there’s no need to purchase trip protection

- Purchase security – rest easy knowing your transactions are safeguarded

- Auto rental collision damage waiver – bypass rental car insurance when you pay with your card

- Extended warranty protection – prolong the standard manufacturer’s warranty for any item you purchase with your card

- Return protection – you’re covered for return fees for any item you purchase with your card

- Zero liability protection – don’t pay out-of-pocket for fraudulent card use

- Visa Signature concierge service – 24/7 enhanced support through Visa

- Travel & emergency assistance – get help when you need it — just call the number in your cardholder agreement

- Roadside dispatch – get a tow, a tire, or a battery delivered when you have problems on the road

Personally, I love taking advantage of included insurances and protections through my credit card as opposed to purchasing additional insurance through vendors because it’s convenient and it saves money.

The trick is to make sure you know which cards come with which protections so that you use the right card for relevant purchases — X1 has a well-rounded offer, so you don’t have to worry about that.

8. Receive Up to 5X Higher Spending Limits

While the X1 card does not claim to guarantee any specific credit limit, they assert that most approved applicants receive a higher credit limit than their current average line. This data was acquired from X1 cardholders on August 22, 2022.

What’s interesting about this to me is that this advertised benefit used to be, “based on advertised terms as of August 16, 2020, for each of the following cards: Chase Sapphire Preferred®, American Express Blue Cash Preferred®, American Express Amex Everyday® Preferred, Bank of America Premium Rewards®, Citi PremierSM.”

So, it seems like the company found a way to reach its original goal and verified this through its current cardholders.

9. Get Approved With An Attainable Credit Score

The key feature of the X1 card that does stand out is that you can claim all of the above benefits and features without a fantastic credit score. This isn’t typical with other credit card offers. With X1, approval is based primarily on current income and future earnings, not a fantastic credit score.

Some cardholders claim that they’ve gotten the best interest rate and highest limits out of all other credit cards. Unfortunately, in most of these cases, we don’t know which other cards they have, so it’s impossible to determine if this is as exciting as they claim.

The Drawbacks

All credit cards come with pros and cons — it’s not fair to tout on about an offer without clearly explaining both. So, here are the potential downsides of the X1 card.

1. Not Intended for Business Use

The X1 program terms clearly state that this card is NOT designed for business use. Several self-employed applicants have complained of not being approved for the card. It seems as though income verification is done via personal bank accounts. For many, this is a drawback.

With that said, for those who aren’t approved, there’s no impact to their credit score, since the x1 underwriting process skips the initial hard pull. So, there’s no considerable risk in applying — but, accepting an offer may be another story.

2. Upon Approval, There Will Be a Hard Pull

On the X1 credit card website, one of the main selling points is to “See if you’re approved with no impact to your credit score.” However, you always need to read the fine print.

If you scroll down the page or read the program terms & conditions, you’ll realize that accepting an offer from X1 after pre-approval will result in a hard pull. Now, this is normal, but potentially misleading (another copywriting decision).

3. You Might Find Unexpected Limitations

While the X1 card seems to have partnered with some major tech, fitness, retail, and travel partners (Bose, Patagonia, and Amazon, to name a few). Admittedly, this may be plenty for some people, and it likely comes with added points on select purchases. Sadly, purchases outside the partner network might be hit or miss.

Limitations on purchases and unpredictable transaction approvals have been infuriating for some cardholders. So, I say you should enter without lofty expectations — otherwise, you might be disappointed.

X1 Company Overview

When gauging the trustworthiness of a financial offer, it’s important to understand who and what is backing it. So, who is behind the X1 Card?

X1 Inc. was co-founded by Deepak Rao and Siddarth Battra, who both left Twitter in 2017 to start this venture to build “the smartest credit card ever made.” Rao was a product manager and Battra was a software engineer. Also notable, Apple’s previous Head of Credit, Abhi Pabba, has recently gone to join X1 as their new Chief Risk Officer.

X1 Visa cards are issued by Coastal Community Bank, an FDIC member. To date, X1 has received $47 million in funding from 14 investors, including Global Founders Capital, Spark Capital, and Harrison Metal.

Frequently Asked Questions

How does the X1 card work?

Visit the X1 website and “order” your card. There will be no hard pull to your credit until after you are approved. Upon approval, you can receive 2+ points on all spending, and refer up to three friends. Manage virtual cards and take advantage of a spectrum of insurance and protections on purchases.

Approval is based more on income than credit score, which is a novel feature for a personal credit card.

How does the X1 card verify income?

X1 does a soft credit inquiry to make approval decisions. If additional verification is needed, you will be contacted by the card’s underwriting team to submit proof of income documentation.

What credit bureau does X1 card use?

Users report a hard pull from Experian upon approval and reporting to Experian and Transunion. The card should start to report to all three bureaus once they have enough cardholders to do so.

What are X1 points worth?

As with most credit rewards, X1 points are equal to one cent, but some purchases may offer 1:1.4 rather than 1:1 (in these cases, they’re worth 1.4 cents each).

How do you redeem X1 points?

You can redeem X1 points directly on in-app purchases when your points balance can cover the full amount. You may also redeem points as cash back on your statement.

How long is the x1 card invite good for?

The invitation period for an X1 card referral/invitation code is six months.

Conclusion: Is X1 Really “the Smartest Credit Card Ever Made?”

Is the X1 card legit? Yeah, I think so! Does it deserve all the fuss? Maybe… especially considering that they’ve managed to pack a ton of features into one credit card offer. For some people in certain situations, it could be a go-to credit card. For others, not so much.

I feel it’s important to note that, in this article, the focus was on comparing the X1 card to more traditional credit card offers. And, the findings might have been different if we would have looked at it side-by-side next to less conventional offers like the Gemini card or Cred.ai (Who knows, maybe that’s something we’ll add in the future). So, again, do your due diligence before you apply for any card.

The biggest downside, from my perspective, is that X1 doesn’t cater to business owners. Perhaps, in the future, they will offer a business solution. Until then, they do offer features for personal card features that are more akin to existing business credit card offers, so I think it’s worth taking a look at under certain circumstances.

If you’re interested in learning how to obtain up to $100K in business credit in as few as 30 days, join business credit workshop today.