Expensify is a leading business expense management app with a (fairly new) corporate card offer for small businesses. And, as you know, finding the right corporate card is super important. In this review, I’ll touch on the Expensify app, then dive deep into the Expensify Card offer.

You can explore its features, benefits, and I’ll point you to a couple other corporate card offers you might want to compare.

Here’s what’s in store:

- What is Expensify?

- Expensify Corporate Card Features & Benefits

- Frequently Asked Questions

- Conclusion

Now, let’s scrolll!

What is Expensify?

Expensify, at its core, is an expense management tool designed to simplify the intricate process of handling business expenditures. Its standout feature is the automated receipt tracking, allowing users to effortlessly scan receipts via the mobile app (which reduces manual data entry).

The platform also encompasses:

- Expense reports

- Simplified approval workflows

- Travel benefits

- Receipt scanning

- Cost control measures

- Staff reimbursements

Another distinctive feature of Expensify is its seamless integration between the Expensify Card and the app, facilitating real-time transaction syncing. This real-time connection enhances the overall efficiency of expense tracking and reporting.

Now, I always turn to Reddit for external opinions. This time, Redditors gave the app mixed reviews, but overall decent.

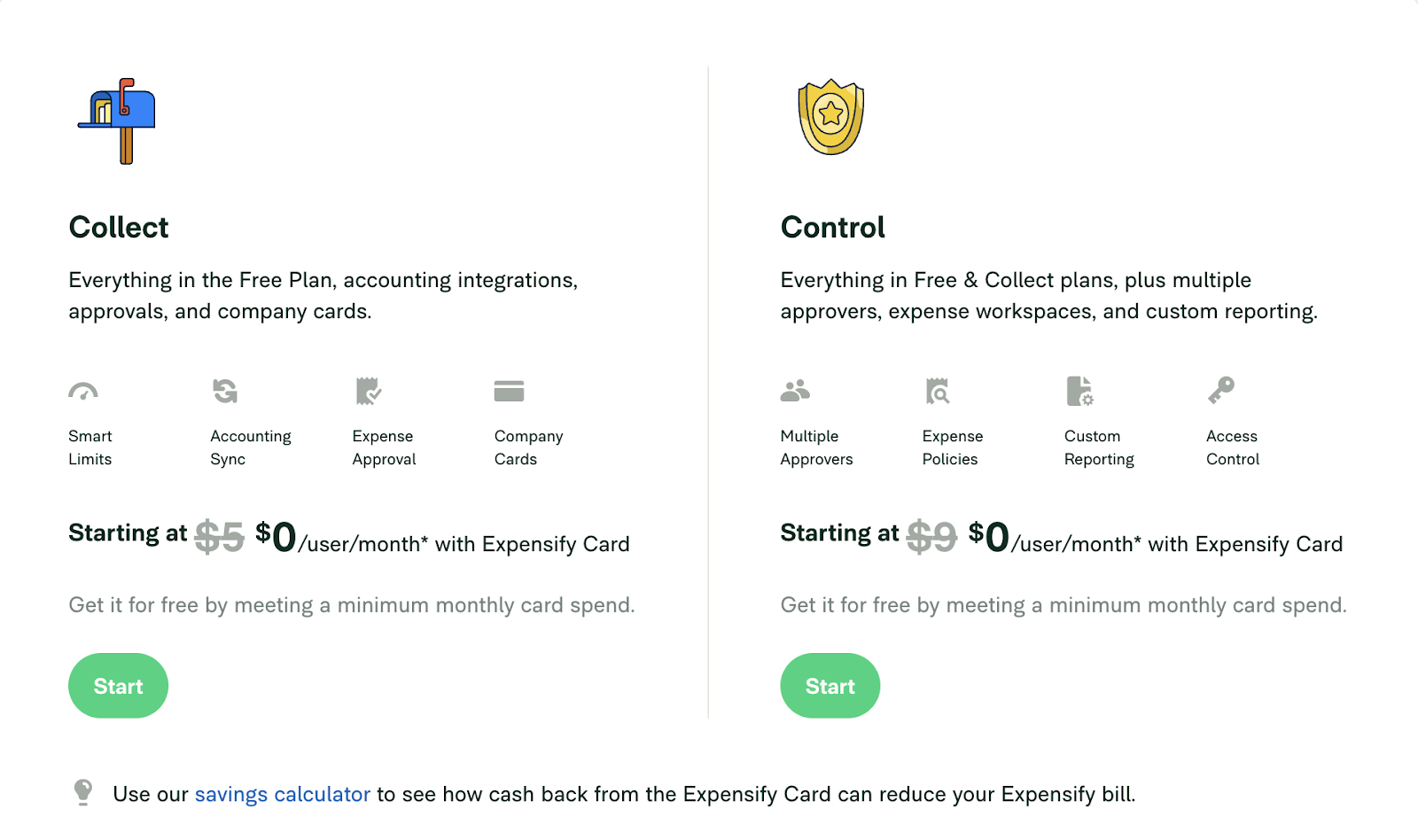

If you’re asking, “How much does Expensify cost?” you’ll be surprised – Most plans are free for up to 25 swipes per month, which gives you the chance to try it out and see if it’s right for you before you commit. After that, you’ll supposedly pay anywhere from $0 to $9 per month, depending on the plan you choose.

However, once you’re in the app, you’ll see that pricing can be a bit higher (though still affordable, and more in alignment with what I would expect to pay).

Overall, I’d say that, collectively, these features form a robust expense management solution for businesses of varying sizes and needs.

Recommended: 7 Best Cash Back Corporate Cards to Explore

Expensify Company Overview

Originally founded in 2008 by Davit Barrett, Expensify Inc. has become a prominent player in the expense management landscape. It’s a publicly-traded, for-profit company with a commitment to simplifying financial processes.

Barrett has served as the CEO of Expensify Inc. since 2009 – previously, he worked as an Engineering Manager at both Red Swoosh and Akamai.

According to Glassdoor (as of December 2023, anyway), employees would recommend Expensify to a friend and tend to approve of the CEO – This speaks volumes.

In all, I would say Expensify appears to be run by trustworthy leadership and that it’s a legit company. .

What is the Expensify Card?

The Expensify Card – released in 2019 – is a corporate credit card (so, technically not a credit card), designed to automate and simplify expense tracking. It serves as a central component of Expensify’s expense management solution.

Recommended: Corporate vs Business Credit Card: What’s the Difference?

★ With this card, you have the option to settle-up on your balance daily or monthly – the choice is yours. Since it’s a corporate card, it must be paid in full.

When employees use the Expensify Card, the associated transactions are automatically imported and accounted for within the Expensify app. This seamless integration enhances the overall user experience and efficiency in managing expenses.

The Expensify card is equipped with features such as Smart Limits, offering businesses control over employee spending, and real-time compliance checks through the Rogue Agent Detection system to ensure adherence to company policies and mitigate the risk of fraud.

The card also comes with perks, including:

- Cash back rewards of up to 2%

- Exclusive travel benefits

- Access to higher credit limits without the need for a credit check.

With its automated features, real-time syncing, and additional benefits, the Expensify Card aims to streamline expense management and provide businesses with a practical and efficient tool for handling financial transactions.

You might also like: In-Depth Divvy (BILL) Credit Card Review: Read This Before You Apply

Expensify Corporate Card Features & Benefits

Corporate finance becomes more streamlined and advantageous when you take advantage of all of the features of your financial tools. Expensify and the Expensify Card offer an integrated solution, purpose-built to cater to evolving business needs — Let’s take a look at the card features and benefits.

You might also like: Business Credit Workshop’s Official Business Credit Building Checklist

1. Benefit From Up to 2% Cashback Rewards

Expensify provides you with cashback rewards on every purchase made with your corporate card. The straightforward rewards structure offers 1% cash back on every swipe and an additional 1% for substantial monthly spending exceeding $250,000 across all Expensify Cards company-wide.

This cashback feature can provide tangible benefits as you spend, manage, and optimize your business expenses – For every $1,000 you spend, you can earn up to $20 (it may not seem like much, but it can add up fast).

2. Cash in on Exclusive Partner Discounts

Distinguishing itself through strategic partnerships, the Expensify Card unlocks exclusive perks and discounts from industry-leading partners. As a cardholder, you gain access to a variety of benefits, which can potentially result in substantial savings of up to $75,000.

This cashback structure positions the Expensify Corporate Card as not just a financial tool but a strategic asset for you, seeking cost-effective solutions through collaborative partnerships.

You might also like: Brex Card Review: Is This Corporate Card Offer Too Good to be True?

3. Get Streamlined Expense Reporting

Your Expensify Card goes beyond transactional benefits by offering streamlined expense reporting. The platform allows for seamless expense tracking and reporting, reducing the administrative burden on your finance teams. With an intuitive interface, you can efficiently manage and reconcile expenses, improving your overall financial efficiency.

4. Leverage Travel Benefits

Enhance your business trips with travel benefits, including Expensify Concierge, which includes:

- Travel bookings

- Free medical advisory

- Emergency transport if needed

They offer a more comprehensive travel support system than I expected, which I think the company’s commitment to providing a holistic solution for businesses.

You might also like: Marriott Bonvoy Business Credit Card Review & Comparison

5. Set Smart Limits on Spending

Your Expensify Corporate Card empowers you with Smart Limits, a nuanced approach to financial control. Tailor spending thresholds for your employees, ensuring financial responsibility and providing flexibility to set limits based on individual roles or departments.

Smart Limits promote conservative financial practices, which contribute to a more controlled and efficient expense management process.

6. Take Advantage of Virtual Cards

Expensify’s Virtual cards provide an additional layer of convenience, allowing for secure online transactions without the need for a physical card. Not only that, but you can generate new cards if/when you need them.

Virtual cards give you financial leeway while maintaining prudent spending practices.

You might also like: 6 Best Fintech Credit Cards to Apply for (Consumer & Business)

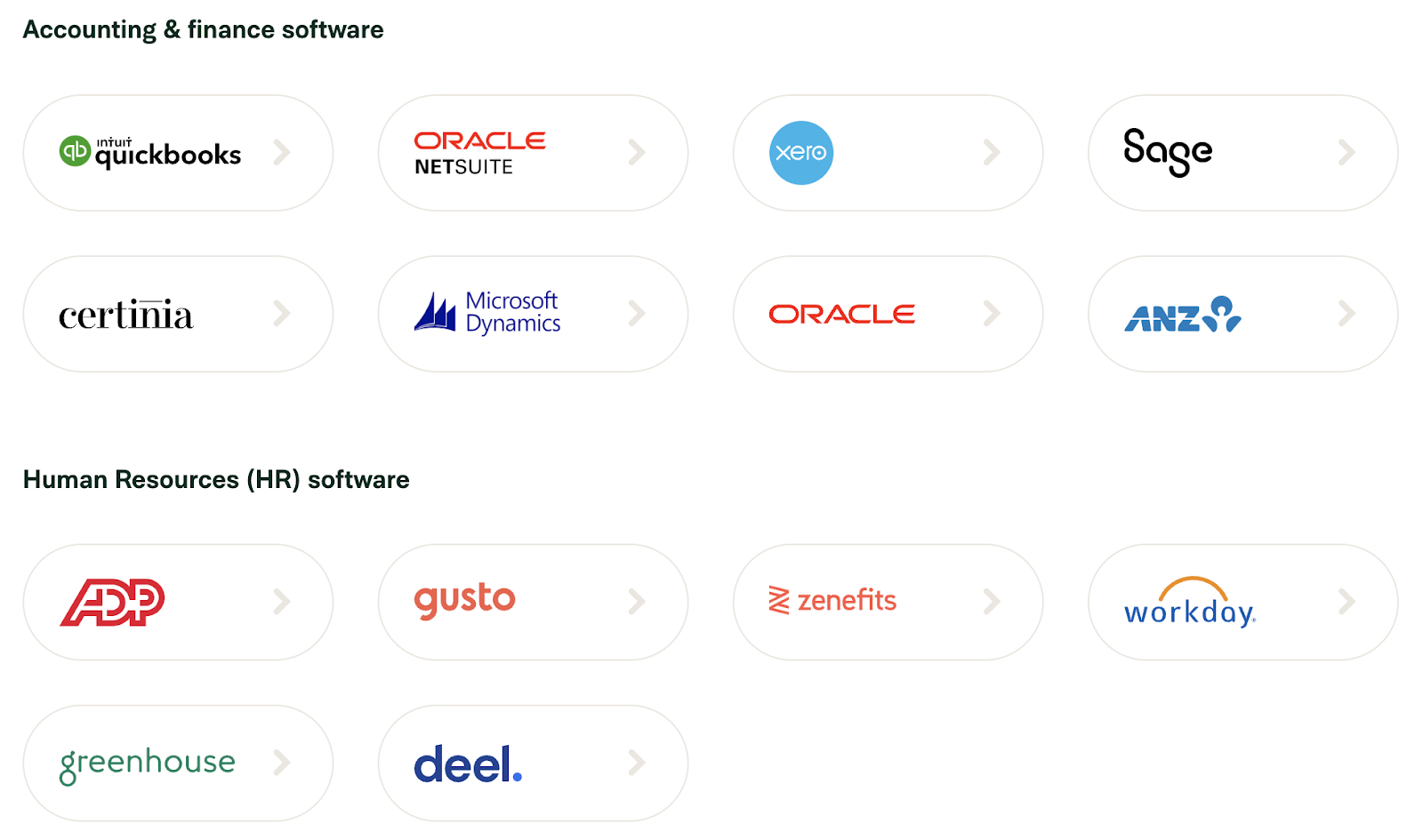

7. Integrate With the Expensify App & More

Then, you can integrate Expensify with your other software tools, including accounting, finance, ERP, travel, and tax, providing seamless data transfer and collaboration between platforms.

The user-friendly experience ensures that you can efficiently track and report expenses without the delays associated with manual data entry.

You might also like: Gusto Review: Let’s Really Evaluate This Famed Payroll Platform

Frequently Asked Questions

What does the Expensify card do?

The Expensify Card is a corporate card designed to automate expense tracking. It offers features like Smart Limits, real-time compliance checks, and automatic daily or monthly settlement. Users can gain up to 2% cash back on purchases, and the card seamlessly integrates with the Expensify app for efficient expense management.

How do you request an Expensify card?

You can initiate the request within the Expensify platform, typically through the account settings or the designated card management section. The platform guides you through the application process for a quick and hassle-free experience.

How do you pay your Expensify card?

Payment for the Expensify card is conveniently handled through automatic daily or monthly settlement (your choice). The card balance is automatically paid in full each day or each month from the connected business bank account.

Is Expensify any good?

Expensify is widely regarded as a reliable expense management solution — Its features, including real-time compliance, receipt tracking, and the Expensify card’s benefits, contribute to its positive reputation. Many users like its user-friendly interface and seamless integration capabilities.

Is the Expensify card free?

Yes, the Expensify card comes free with an Expensify account. It has no additional fees, no interest charges, and no commitment. Expensify users can leverage the card’s features and benefits at no extra cost.

Conclusion

In sum, the Expensify Card presents a compelling solution for businesses seeking efficient expense management. Its automation features, cash back rewards, and integration capabilities make it a strong contender in the corporate card landscape.

However, I need to note that Expensify does not report on-time payments to credit bureaus at this time. There are comparable corporate cards you can get that actually help you build business credit, which has the potential to transform your life.

Are you ready to obtain up to $100K in business credit in as few as 30 days? Join Business Credit Workshop today!