So, you’re thinking about whether or not you might need a business charge card. Well, you’ve landed in the right place. Here, we’ll explore what it is, why you might need one, and see a list of charge cards that offer the best business features and perks. You’ll also find answers to some of the most common questions I hear.

This is what’s in store.

- What is a Business Charge Card?

- Best Business Charge Cards for Startups

- Frequently Asked Questions

- Conclusion

Now, let’s get to it!

What is a Business Charge Card?

A business charge card, also known as a corporate card, is a payment card issued to a business rather than an individual. Here’s what you need to know:

- It’s used for business-related expenses like travel, supplies, or client entertainment.

- Unlike credit cards, you’re typically required to pay off the balance in full each month.

- Many business charge cards offer perks like rewards programs, expense management tools, and employee spending controls.

- They can help track expenses, simplify accounting, and provide businesses with financial flexibility.

- Businesses of various sizes, from small startups to large corporations, use these cards.

Overall, a business charge card can be a handy tool to manage business expenses and cash flow.

You might also like: 7 Best Cash Back Corporate Credit Cards to Explore

Business Charge Card vs Credit Card

Here’s a comparison between a business charge card and a business credit card.

| Business Charge Card | Business Credit Card |

| Typically, you’re required to pay off the balance in full each month.Since you’re expected to pay in full, there are usually no interest charges.Often used for business expenses where immediate payment is expected.Some charge cards have no pre-set spending limits.Annual fees can be higher than credit cards, but often come with premium benefits.Many offer rewards programs and perks tailored to business needs.Often equipped with tools for expense tracking and management. | You can carry a balance from month to month, with interest charges applied to the outstanding balance.Typically has a pre-set spending limit based on creditworthiness.If you carry a balance, interest charges will apply to the remaining amount.Annual fees vary depending on the card, and may be lower than charge cards.Offer rewards programs similar to personal credit cards, often with options for cash back, points, or travel rewards.Some credit cards offer expense tracking tools, but they’re not typically as robust as charge cards. |

In essence, a business charge card requires full payment each month with potentially higher annual fees but often comes with premium benefits. Meanwhile, a business credit card offers more flexibility with revolving payment terms and typically lower annual fees, but may incur interest charges if you carry a balance.

You might also like: Corporate vs Business Credit Card: What’s the Difference?

Are Charge Cards Good for Business?

Charge cards can be beneficial for businesses, but whether they’re a good fit depends on various factors. So, why do people use a charge card?

Here’s how they can be useful:

- With the requirement to pay off the balance in full each month, charge cards promote responsible spending habits and help prevent debt accumulation—This can lead to better expense management and financial discipline within your business.

- Since charge cards dictate that you pay the balance in full, there are typically no interest charges—This can save money in the long run compared to credit cards where interest can accrue on carried balances.

- Many charge cards offer rewards programs tailored to business needs, such as:

- Cash back on business-related purchases

- Travel rewards

- Discounts on business services.

These perks can provide additional value to your business.

- Charge cards often come with robust expense tracking and management tools, helping you keep better track of business spending, categorize expenses, and simplify accounting processes.

However, there are also some potential drawbacks to think about:

- Charge cards may come with higher annual fees compared to credit cards, especially those that offer premium benefits and rewards programs. Depending on your spending habits and the value derived from these perks, the annual fee may or may not justify the expense.

- While charge cards are widely accepted, there may be instances where certain vendors or suppliers do not accept them—This can pose challenges if you rely heavily on vendors who prefer credit cards or other forms of payment.

- Since charge cards require paying the balance in full each month, they may pose cash flow constraints if you have irregular income or seasonal fluctuations. But, you can mitigate this with proper budgeting and cash flow management.

So, charge cards can be useful for businesses that prioritize responsible spending, value expense management tools, and can afford the higher annual fees. However, carefully consider your specific needs, spending habits, and cash flow requirements before you decide if a charge card is the right fit.

You might also like: How to Convert Credit Cards into Cash

Best Business Charge Cards for Startups

When it comes to choosing the best business charge card for startups, several options offer benefits tailored to the needs of new businesses. Here are some top recommendations.

These cards offer a range of benefits suited to the needs of startups, including rewards, expense management tools, flexible payment options, and tailored perks. Consider your business’s spending patterns, priorities, and eligibility criteria when choosing the best option.

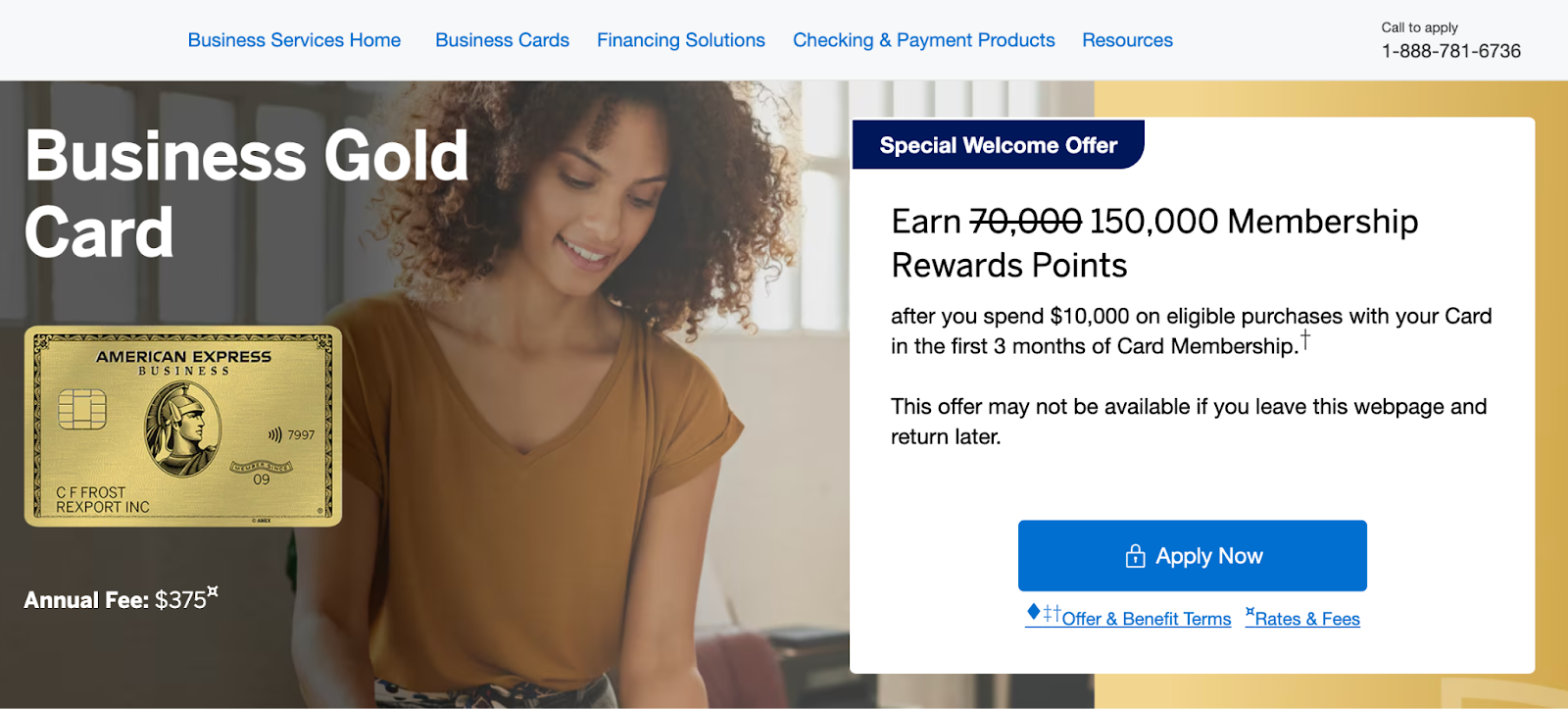

1. Amex Business Gold Card

The American Express Business Gold Card offers valuable rewards, earning Membership Rewards points on eligible purchases, with 4X points in two select categories where your business spends the most each billing cycle (up to $150,000 in combined purchases per year).

It features a generous welcome offer in the form of bonus points after meeting spending requirements. The card provides access to tools like Vendor Pay and ReceiptMatch to simplify expense tracking and management.

And, it includes a flexible payment option to carry a balance for eligible charges with interest charges—essentially turning it into a credit card for qualified business operations if that’s what you need.

2. Brex Corporate Card

The Brex corporate card offers a range of advantages tailored to meet new business’ needs. One notable feature is that it doesn’t require a personal guarantee, making it ideal for startups without an established credit history or the need for a security deposit.

Moreover, you can earn points on all purchases, with bonus points available in categories like travel and restaurants. The card comes with intuitive expense management tools, including an easy-to-use dashboard for tracking expenses and gaining real-time visibility into spending.

And, you can enjoy additional benefits such as discounts and credits on various business services, including AWS, Google Ads, and more.

Recommended: Brex Card Review: Is This Corporate Card Offer Too Good to be True?

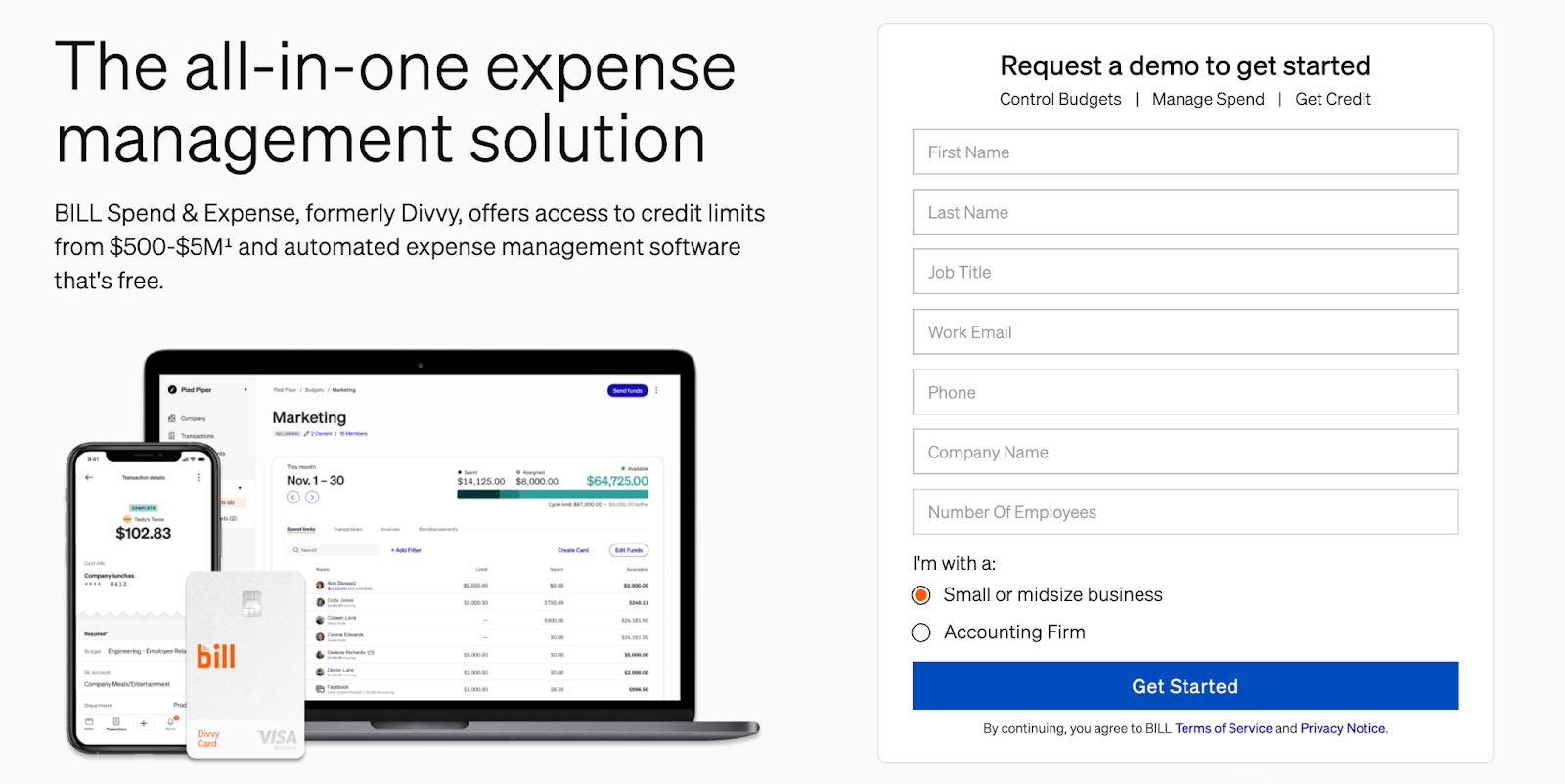

3. Bill Spend & Expense (Divvy) Card

The Divvy Spend & Expense card – formerly “Divvy” – offers several benefits tailored to businesses. Firstly, it boasts no annual fee, making it a cost-effective option if you want to manage expenses without incurring additional charges. As a charge card, it also eliminates interest charges, which provides further financial flexibility.

The card comes equipped with robust expense management features, including real-time expense tracking and budgeting tools. You can easily categorize spending, which enables better expense control and analysis. Plus, the card rewards users with points or cash back on all purchases, with bonus rewards available in select categories.

Lastly, the Divvy card simplifies the reimbursement process for employees’ out-of-pocket expenses, which makes it convenient for both employers and staff.

Recommended: BILL Spend & Expense Card Review (Formerly Divvy Credit Card)

4. Ramp Corporate Card

The Ramp Card offers innovative solutions for businesses seeking better cash flow options.

Positioned as a top choice among alternative corporate cards for startups, Ramp stands out for its:

- Rewards program

- Expense management tools

- Accessibility

With features like unlimited staff cards and smart spending limits, Ramp empowers you with complete control over business expenses—It eliminates various fees and offers a generous 1.5% cash back on spending.

Qualification is straightforward, with no credit checks or founder guarantees required. Compared to other marketplace offers, Ramp offers competitive benefits, which makes it a compelling offer with minimal downsides.

Recommended: Ramp Credit Card Review: Is This the Corporate Card for Your Business?

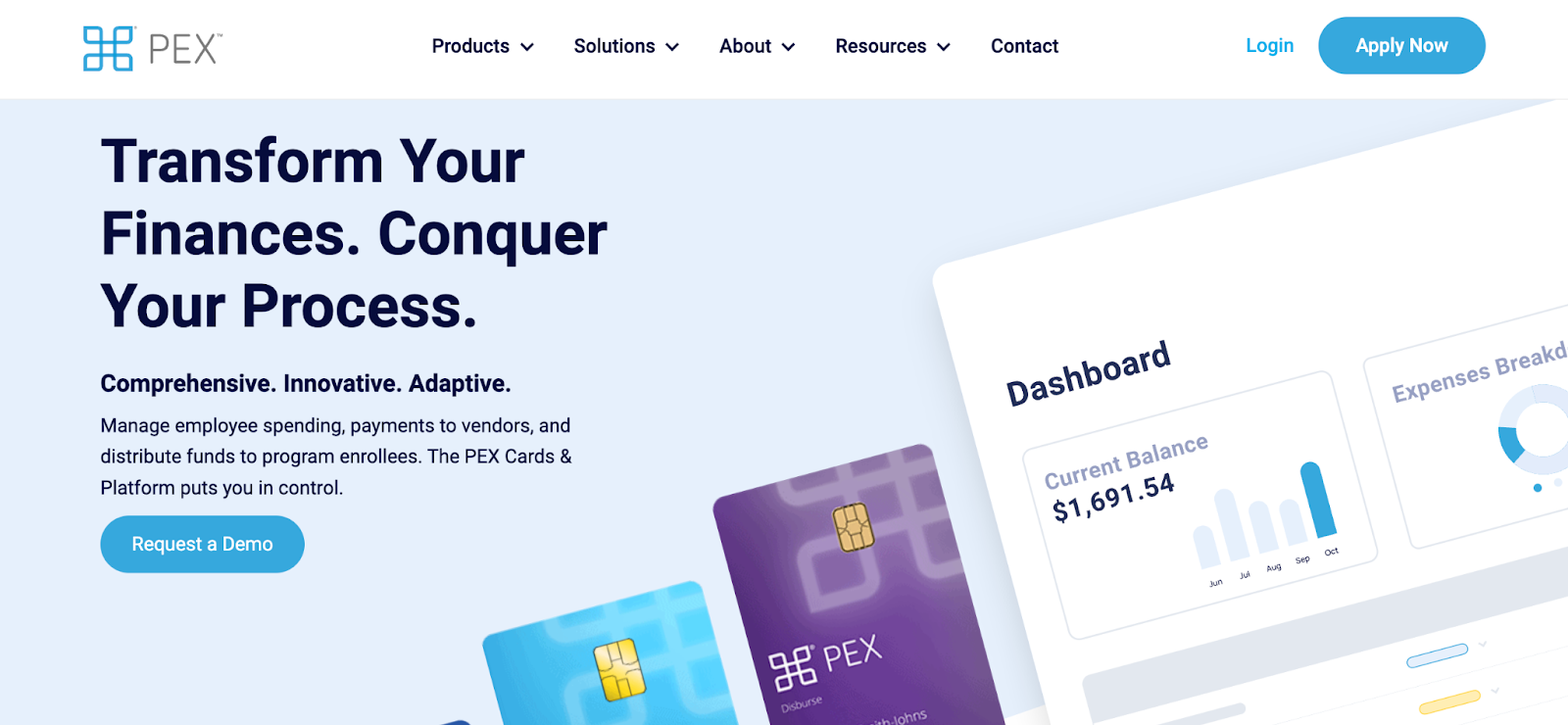

5. The PEX Card

The PEX Card offers a comprehensive corporate expense management solution. With features like prepaid and dynamic credit cards, you can efficiently manage employee spending, vendor payments, and fund distribution.

The platform provides a range of benefits, including 1% cash back on eligible purchases, a user-friendly app for real-time monitoring and authorization, and seamless integrations with accounting systems.

You can distribute both physical and virtual cards, set customizable rules and spending limits, and streamline grant fund distribution for nonprofits. Despite its strengths, consider your specific needs and compare alternatives before you make a decision.

Recommended: The PEX Card: Is it the Best Corporate Card for Your Business?

Frequently Asked Questions

What is the point of a charge card?

Charge cards offer a payment method where users pay the full balance each billing cycle to manage expenses while you avoid interest charges and promote responsible spending.

Why would a business issue a charge card to their customers?

Businesses issue charge cards to facilitate transactions while ensuring prompt payment, which can reduce the risk of outstanding debt for both parties.

What is the difference between a charge card and a debit card?

Charge cards require full payment each billing cycle and function like a short-term loan, while debit cards immediately deduct purchases from the cardholder’s bank account without the option to carry a balance.

Conclusion

Business charge cards offer a unique payment solution for companies, promote responsible spending habits, and provide valuable expense management tools—While they require full payment each month and some may come with higher annual fees compared to credit cards, their benefits, including rewards programs and robust expense tracking, can outweigh these considerations.

However, carefully evaluate your company’s needs and financial situation before deciding if a business charge card is the right fit.

Do you want to learn how to obtain up to $100K in business credit in as few as 30 days? Join Business Credit Workshop today!

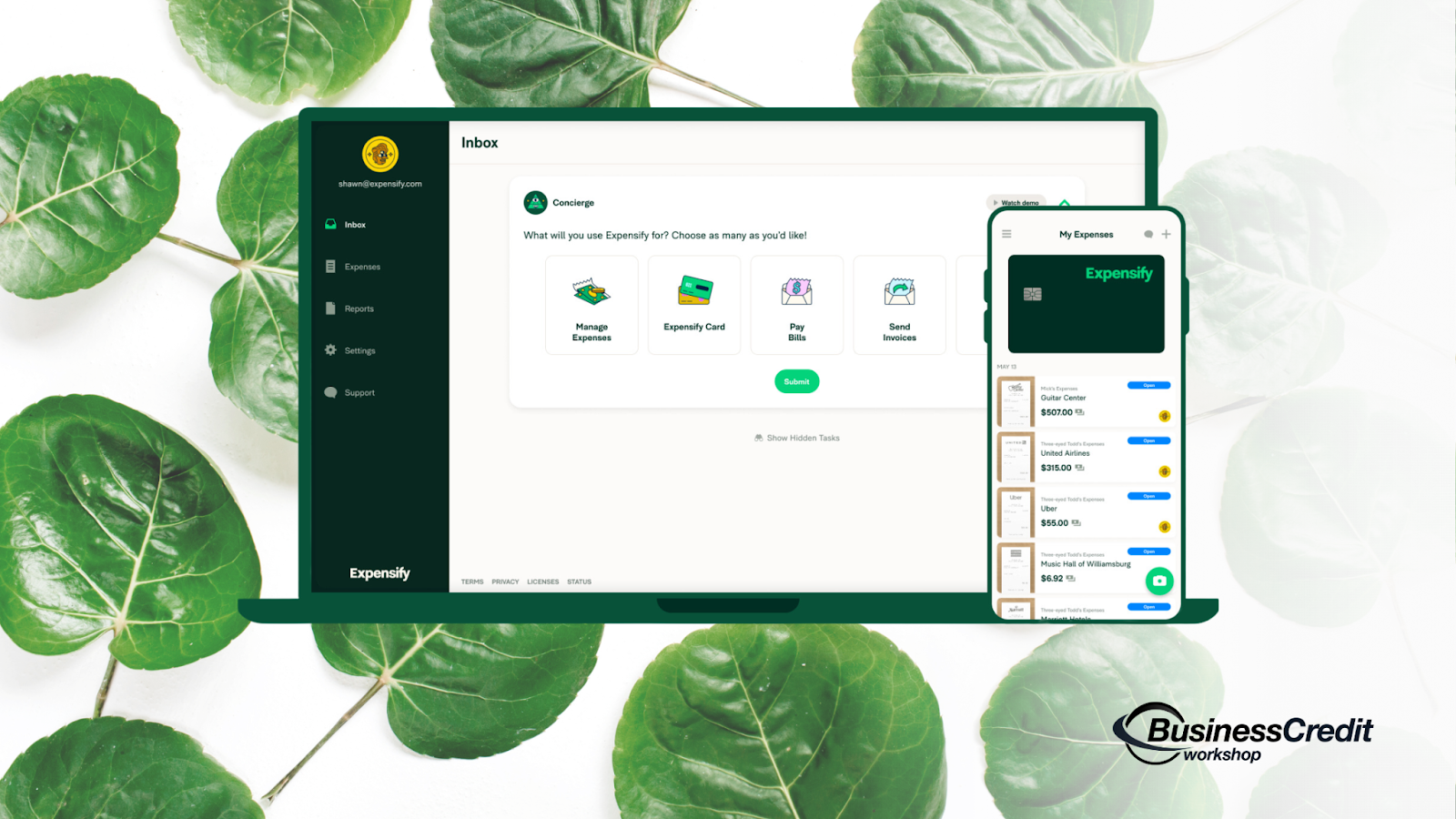

Expensify’s commitment to a seamless user experience is evident in the integration between the Expensify Corporate Card and the Expensify app. This integration ensures immediate and reliable syncing of your transactions, providing you with real-time insights into your financial activities.

Expensify’s commitment to a seamless user experience is evident in the integration between the Expensify Corporate Card and the Expensify app. This integration ensures immediate and reliable syncing of your transactions, providing you with real-time insights into your financial activities.