Recently, we’ve been reviewing popular online banks, and I noticed a trending issue: Many business banking offers are incompatible with Zelle — it’s hanging people up. But, there’s a promising technology that might give Zelle and other P2P payment platforms a run for their money: Real-Time Payments.

Here, I break down what I know about this tech and how real-time payments could revolutionize small business banking.

Here’s what’s in store:

- What are Real-Time Payments?

- Which Banks Offer Real-Time Payments?

- Frequently Asked Questions

- Summary

Now, let’s roll!

What are Real-Time Payments?

RTP® is a new, mobile-ready, instantaneous payment platform from The Clearing House. The platform has been available to its Real-Time Payments Network (participating banks and credit unions) for five years.

Recently The Clearing House announced some exciting changes:

- Higher volume capabilities

- Expanded technical access

- Enhanced fraud prevention

- Improved invoicing functionality

- New banks onboarding weekly

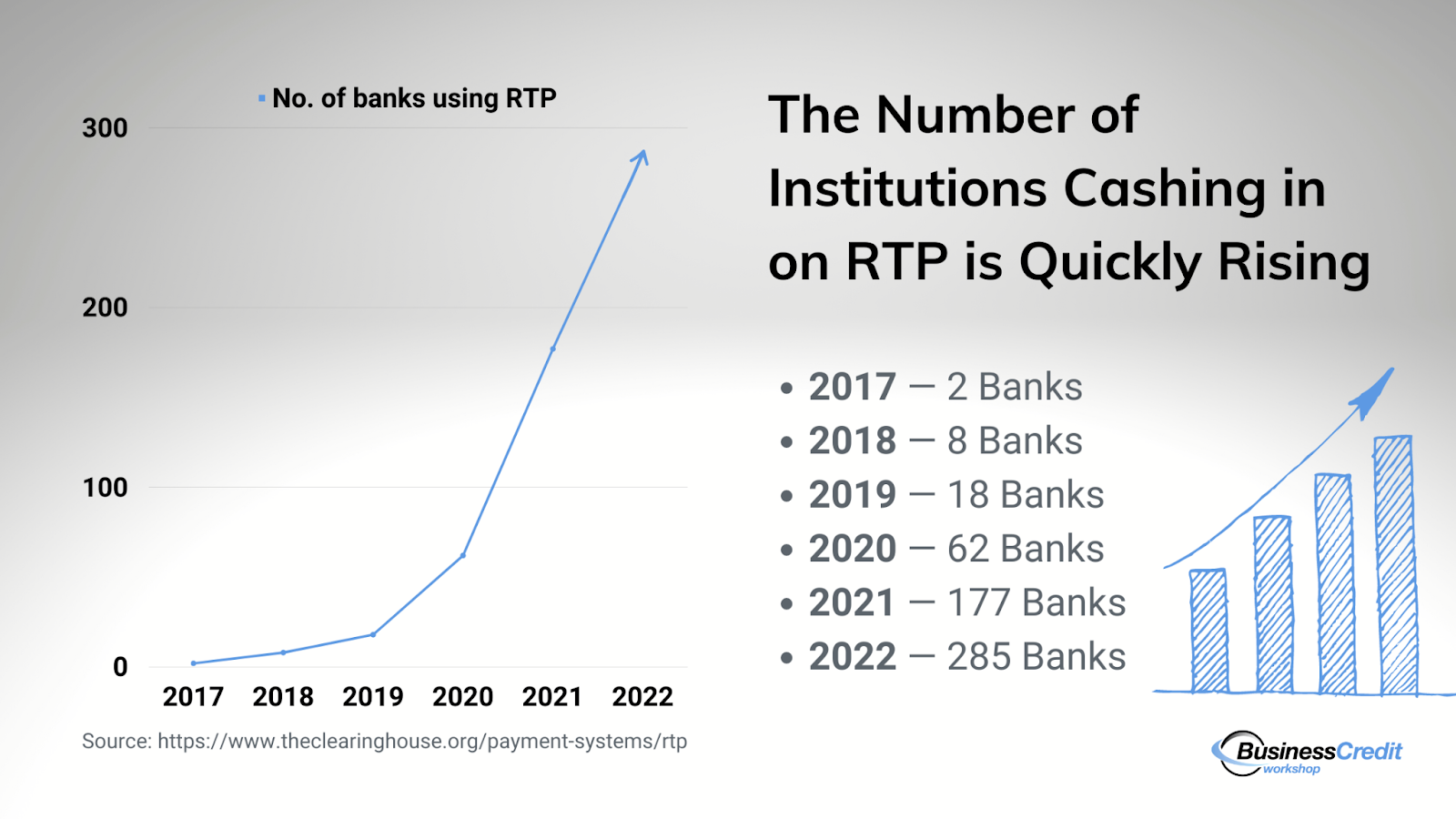

The platform has grown from 2 participating banks at the onset of 2017 to 62 in October of 2020, and engagement has since exploded — As of November 2022, 285 banks have signed on to offer RTP to their account holders.

You might also like: What’s the Best Payment Processor for a Small Business? Really

The Clearing House Company Overview

The Clearing House Payments Company, LLC, also known as THC, is a New York-based payments company, established in 1853 — it’s the oldest banking association and payments company in America. TCH is owned by the largest commercial banks, responsible for more than half of the country’s deposits.

|  |  |

|  |  |

|  |  |

|  |  |

The company provides payment, clearing, and settlement services to its banks and third-party financial institutions. THC is responsible for almost half of all funds-transfer and check-image payments in the United States, which total nearly $2 trillion daily.

TCH employs 479 LinkedIn members, led by the current CEO, James Aramanda. This is an established, well-trusted company with a highly-impressive track record.

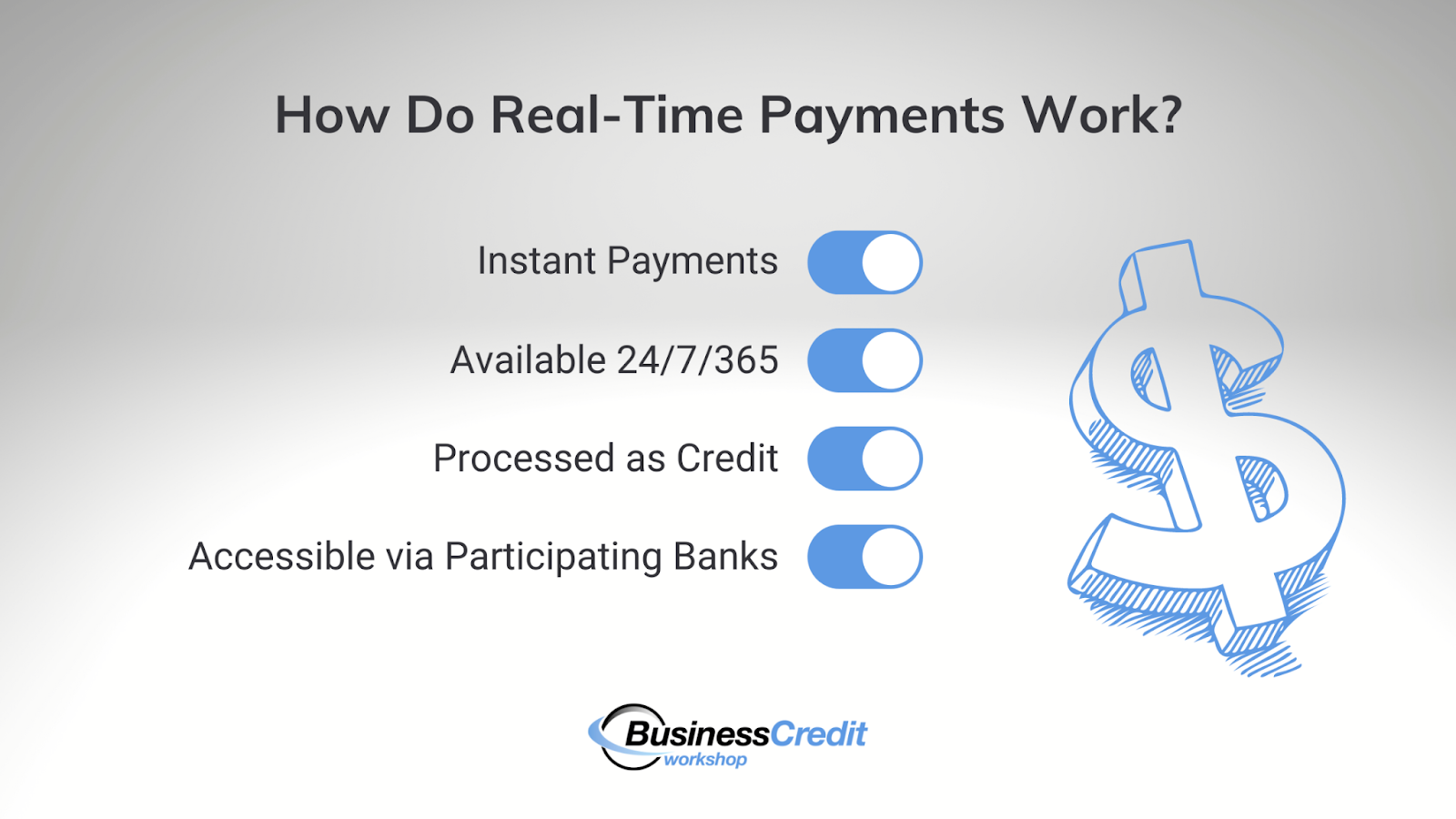

How Do Real-Time Payments Work?

On the user end, RTP enables consumers and businesses to receive funds almost instantly through their banking platform. With RTP, the time between a payment request and settlement takes seconds.

We’re not talking about ACH or same-day payments here — RTP is lightning-fast.

As a business owner, this feature can give you instant access to cash flow, which changes the game entirely: no more waiting 24-72 hours or longer to receive your funds.

Traditional payment communication is a one-way street in the way that transaction information is sent from the sender to the receiver. Now, RTP provides a gateway for two-way, inter-institution data (and funds) transfer in one transaction…instantly.

This not only gives you “real-time” access to money, but helps enhance trust, improve cash flow, and increase your level of financial control.

Real-Time Payments Features

There are a few standout features of RTP worth noting.

→ Transactions are final — RTP transactions can’t be reversed. This can be a risk for the sender, so there are some use cases for which RTP isn’t a good fit (this isn’t to say that any billable goods or services can’t be refunded at the discretion of the receiver).

→ Account numbers are protected — Secure Token Exchange via DDA tokenization now issues tokens that represent real account numbers when the RTP system sends or receives payments. So, there’s less risk of potential fraud within the system.

→ Internal communication is an option — PDF and XML documents are newly-available assets within the RTP platform; users can now send bills, invoices, and remittances as part of real-time payment requests or follow-up messages.

Where are Real-Time Payments Available?

75% of banks in the United States with demand deposit accounts (DDAs) have access to the RTP network, and 60% of them are taking advantage of the offer currently (see which banks offer RTP below). TCH’s payment platform is currently only available within its own network, hence available only in the U.S.

Keep in mind, however, TCH’s RTP is not the only real-time payments solution. In fact, there are several similar systems emerging worldwide.

First, Zelle is a household name that offers instant payments between banks. Again, many business bank accounts aren’t Zelle-enabled, which can be frustrating.

Next, the Federal Reserve is working on FedNow, a lightning-fast payment solution that will be available for select institutions soon. Note that the speed at which banks are signing on makes it appear that RTP’s reach might continue to surpass the Federal Reserve’s upcoming real-time payments system.

Furthermore, according to ACI, India is the global leader in real-time payment options. So, there are comparable systems available globally — maybe 50 or so across the world, with varying capabilities.

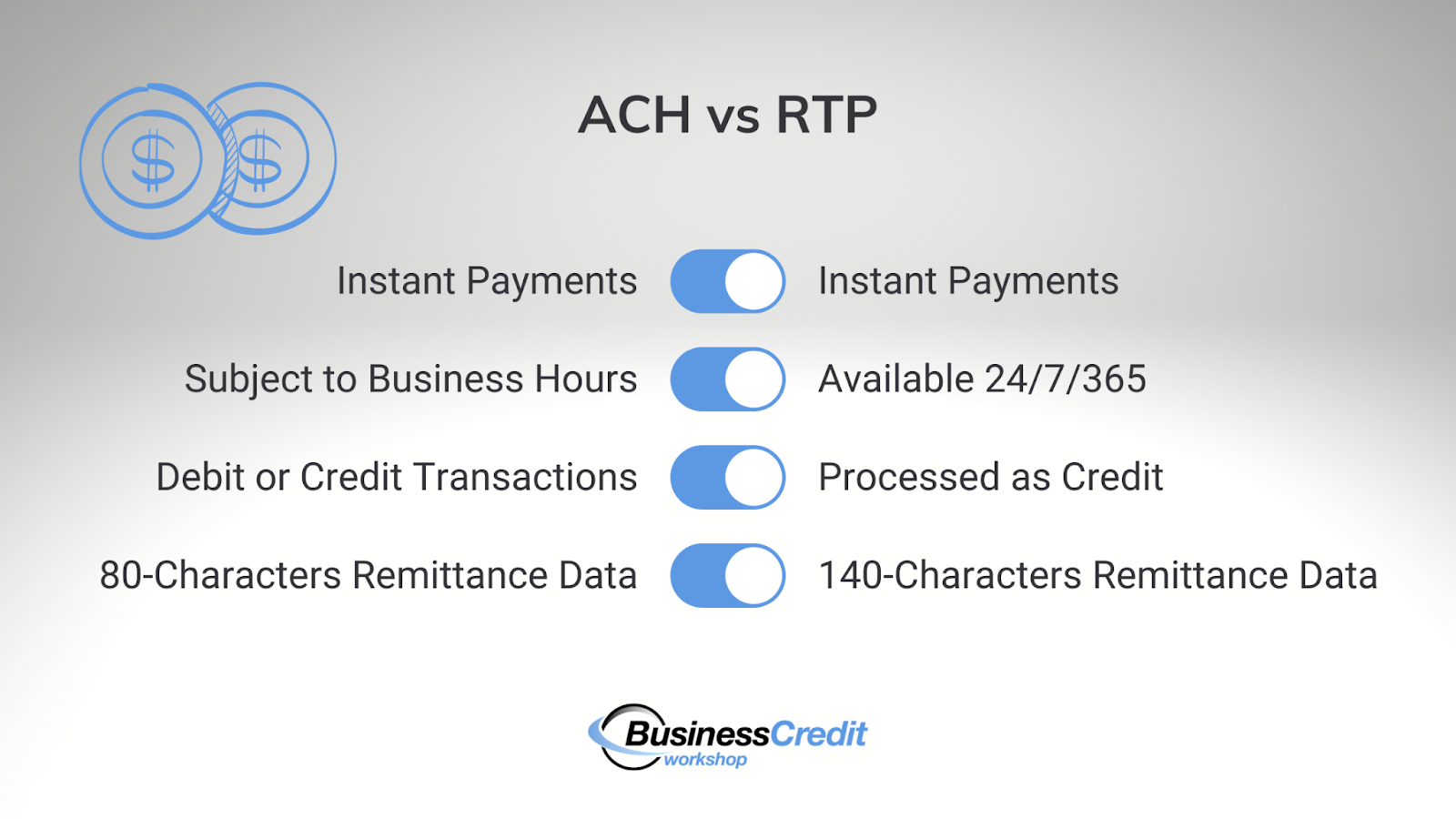

What is the Difference Between ACH and RTP?

ACH and RTP are not one in the same. While both of these systems offer a way to complete a transaction quickly, that’s where the similarities end.

≠ Between the two systems, there are differences in speed.

ACH can take several hours or days, and that’s if the sender chooses “same-day ACH” at the time of the transaction.

RTP, on the other hand, processes payments instantly; this means that the recipient receives the funds within a few seconds after they are sent.

≠ RTP is “alwasy on.”

ACH payments are completed at the discretion of the institution. Hence, they’re subject to unavailability outside business hours, on weekends and holidays, and based on batch cutoff times.

On the contrary, RTP payments can be made at any time — 24 hours a day, 7 days a week, 365 days of the year. Any time a payment is sent, it will be received right away.

≠ The type of available payments vary with ACH and RTP.

Debit and credit transactions can be processed via ACH. So, funds can be transferred via either type of process.

With RTP, however, all transactions are processed as credit. Note that many merchants process all payments as credit — this doesn’t mean you can’t use a debit card to send real-time payments.

≠ RTP enables institutions to send more remittance data.

With ACH transactions, the remittance data sent with the payment is limited to 80 characters. Both institutions will have access to a very short amount of text to explain the transfer.

And, with RTP transactions, up to 140 characters of remittance data is allowed. Institutions can share a bit more data about the funds being sent and received with RTP than with ACH.

Which Banks Offer Real-Time Payments?

All of the federally-insured depository institutions are eligible to participate in RTP, and 285+ institutions currently take advantage of the system. Some names include big banks like Wells Fargo, US Bank, Bancorp, and BMO along with less-known companies like Regions, Bank of the West, and Security Financial.

With this, I know at least one online “neobank,” NorthOne, takes part via their servicer, Bancorp Bank. There are countless smaller institutions and financial offers that partner with more established institutions to provide both consumer and business financial solutions. So, there’s no telling for sure how many accounts are RTP-enabled.

With that said, these numbers are likely to grow, as the Real-Time Payments technology has only been around for about five years, and was recently launched.

Do All Banks Accept RTP?

We’ve just highlighted some of the banks that participate in RTP, which leaves us with another question: If your bank offers RTP, will the receiving bank be able to accept an instant payment, even if they’re not in the Real-Time Payments network?

The short answer is “no.” As with Zelle and other real-time payment processing solutions, both institutions — the sender and the receiver — must have the system enabled for RTP transactions to be completed instantly.

When the receiving bank is not RTP-ready, and an RTP payment is sent, the recipient will get their funds within the next available ACH deposit window.

Fortunately, a large percentage of banks in the U.S. are now RTP-enabled.

Frequently Asked Questions

Is RTP a direct deposit?

Real-Time Payments are technically a type of credit transaction, not an ACH direct deposit. However, employers and others sending funds can use RTP in many of the same use cases as a direct deposit has traditionally been used.

Do banks charge for RTP?

Banks are charged by The Clearinghouse (about 5 cents per transaction), so they may choose to charge account holders to take advantage of this service, yes.

Will RTP replace ACH?

As more institutions sign up and get acquainted with the RTP system, it could replace ACH as a method to send funds, maybe. But, since RTP cannot be used to collect funds, it is not likely to replace ACH altogether.

Is RTP cheaper than ACH?

RTP costs banks less than 5 cents per transaction, which might be less than the costs for processing ACH. However, fees are charged at the discretion of the institution and banks may charge more for their account holders to use RTP than they charge for ACH.

Is RTP a wire transfer?

In a word, no. RTP is not a wire transfer — by definition, Real-Time Payments are credit transactions.

Is Zelle Real-Time Payments?

Zelle offers a solution to process payments in real time. However, Zelle and the Clearinghouse’s RTP are separate systems. Just because an institution offers RTP does not mean that it offers Zelle and vice versa.

Is Venmo an RTP?

Venmo is a peer-to-peer payment solution that offers instant access to cash, but it is not part of the Real-Time Payments network.

Summary

Who needs Zelle when you’ve got Real-Time Payments? While the system is still in the early stages, RTP offers institutions and their account holders an opportunity to send payments that can be received instantly.

Check with your institution to see if they’re part of the real-time payments network and find out how you can take advantage of the system to pay your employees, square up with suppliers, and take care of your bills. Are you a business owner interested in learning more about the best banks to work with, and ways to grow your company? You might be interested in learning how to obtain up to $100K in business credit in as few as 30 days. If so, join Business Credit Workshop today.