As far as financial institutions are concerned, Sidney Federal Credit Union (SFCU) stands out as a beacon of community-focused banking. They offer tailored solutions to meet the needs of both individuals and businesses.

Unlike traditional big banks, credit unions like SFCU are member-owned cooperatives, which means that profits are reinvested into services. In turn, they’re usually able to offer exemplary products and rates for members. From a business credit perspective, SFCU has some interesting offers. Let’s take a closer look here.

This is what’s in store:

- What is SFCU?

- SFCU Business Financial Products & Services

- SFCU Customer Service

- SFCU Community Involvement

- Frequently Asked Questions

- Final Thoughts

Now, let’s roll!

What is SFCU?

SFCU originated when a group of employees from Scintilla Magneto Corp. gathered in Sidney, NY, to form a credit union. In 1949, they secured a charter from the Bureau of Credit Unions, officially establishing Sidney FCU, later known as Sidney Federal Credit Union.

Today, SFCU boasts 11 branches across several counties in New York state, including parts of Broome, Oneida, Herkimer, Chenango, Delaware, Otsego, Cortland, Onondaga, Madison, Schoharie, Montgomery, Fulton, Hamilton, and Essex. The credit union is governed by a Board of Directors comprising individuals who live and work within the communities SFCU serves.

Established with a mission to serve the local community, Sidney Federal Credit Union has been a cornerstone of financial support since its inception. With a strong commitment to assisting small businesses, SFCU provides a range of specialized financial products and services designed to fuel entrepreneurial growth.

Recommended: 3 Best Credit Unions for Small Business Banking in 2024

Locations Served

SFCU extends its services to individuals and businesses across various counties and towns in New York state.

These areas include:

- Chenango

- Cortland

- Delaware

- Essex

- Fulton

- Hamilton

- Madison

- Montgomery

- Onondaga

- Otsego

- Schoharie

In addition to these counties, specific towns within Broome, Oneida, and Herkimer counties are also within the field of membership.

These towns include:

- Colesville, Sandford, and Windsor Towns in Broome County

- Sangerfield, Bridgewater, Augusta, Marshall, Paris, Vernon, and Kirland Towns in Oneida County

- Winfield, Litchfield, Columbia, Warren, Stark, Danube, Frankfort, and German Flats Towns in Herkimer County

If you reside, work, attend school, worship, or conduct regular business activities within these areas, you may be able to take advantage of SFCU’s services and benefits.

SFCU Membership & Eligibility Requirements

Becoming a member of SFCU is a straightforward process designed to be accessible to all eligible individuals.

Here’s how you can join:

- To initiate your membership, open a savings account with SFCU online. The minimum deposit required is only $5, making it easy for individuals to get started.

- Once your savings account is opened, deposit at least $5 to fulfill the membership requirement.

- With your membership established, you are now eligible to apply for and access a wide range of financial services offered by SFCU, including banking services, business accounts, lending services, and more.

SFCU welcomes not only individuals residing within the specified counties and towns but also extends membership eligibility to employees of SFCU, immediate family or household members, organizations of such persons, and corporate or other legal entities—This inclusive approach ensures that a diverse range of individuals and entities can benefit from the superior service and exceptional financial services offered by SFCU.

SFCU Business Financial Products & Services

Now, let’s take a look at the business financial products offered at SFCU—We’ll look at the checking, credit cards, loans, and savings accounts that small business owners can take advantage of.

SFCU Business Banking/Checking

SFCU offers a few different business checking accounts:

- Basic Business Checking

- Community Checking (for nonprofits)

- Business Dividend Checking

With all business checking accounts, you’ll get a Mastercard debit card, free online and mobile banking with e-statements, and unlimited transactions. You’ll also get free bill pay and be able to access overdraft protection options.

With Basic Business Checking, there are no added fees and no minimum opening deposit. You can avoid the $5 monthly maintenance fee if you maintain a $500 minimum balance.

For not-for-profits, SFCU provides the Community Checking account. There is no minimum initial deposit requirement and no monthly maintenance fee.

Businesses looking to earn dividends on their checking balance can opt for the Business Dividend Checking account. With no minimum initial deposit requirement, businesses must maintain a $5K ADB to earn dividends, and to avoid the $5 monthly maintenance fee—This account offers a competitive .25% APY on balances.

| Feature | Basic Business Checking | Community Checking | Business Dividend Checking |

| Minimum ADB to Earn Dividends | N/A | N/A | $5,000 |

| Minimum ADB to Avoid Monthly Maintenance Fee | $500 | N/A | $5,000 |

| Dividend Rate * | N/A | N/A | .25% APY |

| Monthly Maintenance Fee * | $0 to $5 | $0 | $0 to $5 |

At SFCU, there seems to be a checking option for nearly any small business.

You might also like: Amex Business Checking Review: What You Need to Know…Really

SFCU Business Platinum Mastercard Credit Card

The SFCU Platinum Mastercard® offers a competitive APR starting as low as 13.15%, with a maximum APR of 17.99%. What’s great? There are no annual fees, making it an attractive option for businesses looking to stretch their dollars further.

With this card, you can earn rewards on everyday purchases.

The SFCU credit card earns a flat 1% back that can be redeemed for:

- Cash back

- Travel

- Gift cards

- Charity donations

Plus, there’s no balance transfer fees, and you can enjoy the convenience of tap-to-pay contactless payment. There’s also 24/7 fraud monitoring. If you need to increase your credit limit, you can apply for a limit increase hassle-free.

Recommended: Corporate vs Business Credit Card: What’s the Difference?

SFCU Business Loans & Lines of Credit

SFCU also has an array of business loans, including term loans, lines of credit (revolving), and real estate loans. All of their loans have competitive rates, flexible terms, and come with no prepayment penalties.

If you’re looking to expand or cover expenses, SFCU’s business term loans provide the financing you might need to keep operations running smoothly. Use them for inventory, equipment, or services. Plus, with fixed rates and the option to choose loan terms between 1 and 7 years, budgeting is pretty simple.

For when you need ongoing access to funds, SFCU also provides business lines of credit. These lines of credit offer financial flexibility for various purposes, including cash flow gaps and overdraft protection. With options for both secured and unsecured lines of credit, you can choose the option that best fits your needs and goals.

If commercial or investment real estate properties are on your radar, SFCU offers commercial real estate loans with flexible terms and structures—These loans come with both fixed and variable rates and can be customized to fit your unique needs and goals.

Recommended: How to Get Money for Real Estate Investing: 18 Practical Ideas

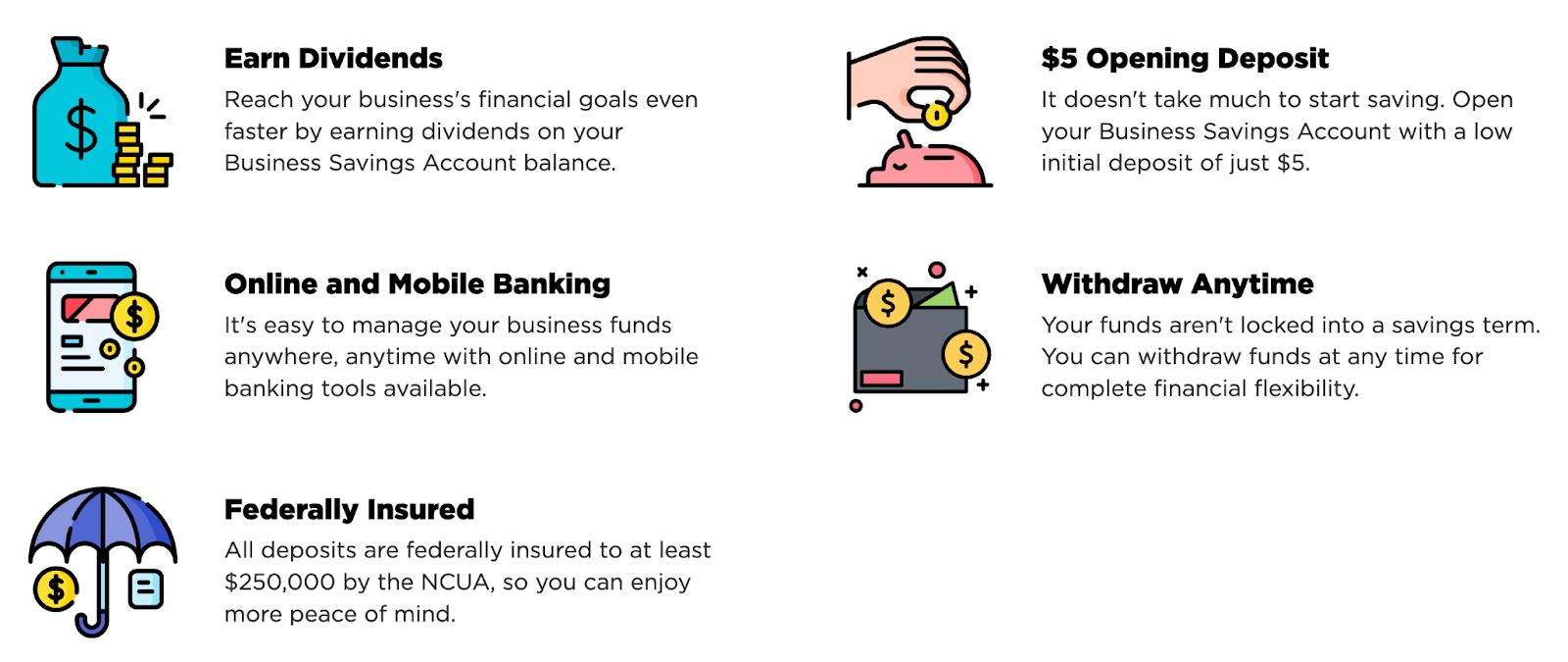

SFCU Business Savings & Investment Opportunities

SFCU offers a few business savings options tailored to suit different financial needs and goals.

- Business savings account

- Business money management account

- Business share certificates

The SFCU Business Savings Account is ideal if you’re looking to build up savings and maintain easy access to funds. With just a $5 minimum opening deposit, you can earn dividends on your balance (up to 0.05% APY)—This account might be good if you want to earn a little extra while saving for short-term business goals or emergencies.

Now, if you want to maximize your savings potential without sacrificing liquidity, SFCU’s Business Money Management Account might be a better choice. With higher dividends and no withdrawal penalties, this account offers flexibility while allowing your savings to grow. It’s suitable when you want to earn more on your funds and retain the ability to access them when needed.

When you’re aiming for long-term savings goals, such as expansion plans or major investments, the Business Share Certificates offer higher savings rates with flexible terms. With terms ranging from 31 days to 60 months and competitive rates as high as 2.53% APY, SFCU’s certificates provide an opportunity to earn more on your savings over time.

In all, SFCU’s business savings options provide opportunities to earn dividends and grow your funds. However, these aren’t the best rates I’ve ever seen.

Recommended: Bluevine Review: Free, High Yield Small Business Checking! Are They Serious?

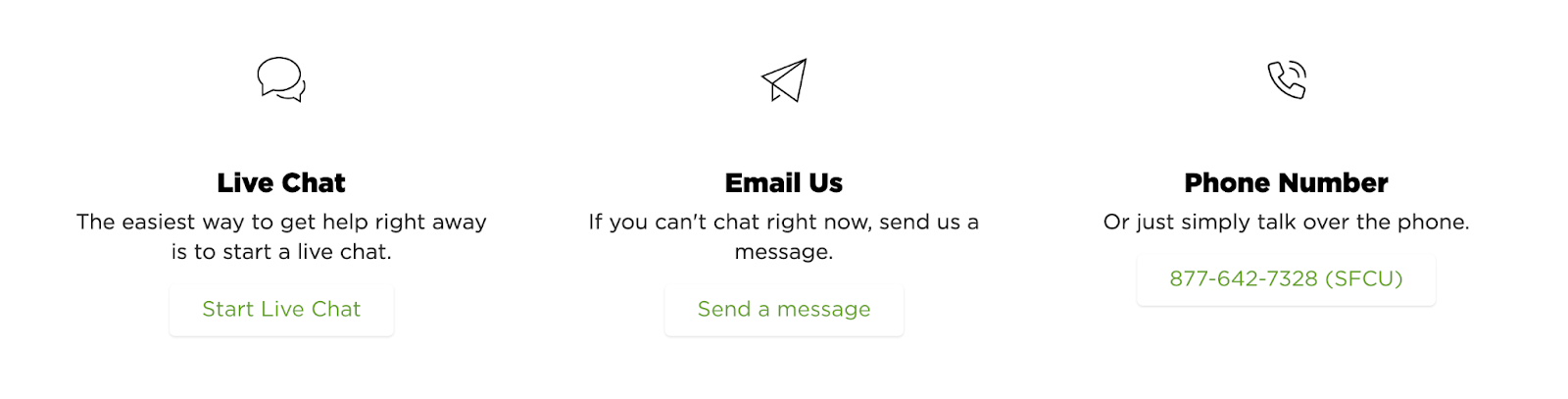

SFCU Customer Service

Sidney Federal Credit Union (SFCU) provides various customer service channels for members’ convenience:

- Live chat – Immediate assistance is available via live chat

- Email – Members can send messages for non-urgent inquiries

- Phone support – Accessible at 877-642-7328 (SFCU)

- SMS text messaging – Support for lost or stolen cards—24/7

- Text message alerts – Receive important notifications via text

These channels ensure members can access assistance promptly and efficiently. Keep in mind, they’re typically available during normal “banking hours” (9 to 5 Monday through Friday).

Of course, as with all services, you might expect mistakes to happen from time to time…But, SFCU has apparently closed all of their *minimal* complaints with the Better Business Bureau promptly. They maintain an A-rating on the platform despite not being accredited.

In all, you should be able to get in touch with someone when you need help.

You might also like: 6 Best 0% APR Business Credit Cards to Check Out

SFCU Community Involvement

Sidney Federal Credit Union (SFCU) is rooted in community spirit—they pioneer local events like the SFCU Hometown Day Parade. It’s a blast, stretching over 1.2 miles, starting at Sidney Central School and winding down to Keith Clark Park for a lively celebration. Locals are invited to be part of the tradition, soaking in the community vibes and enjoying the festivities.

Ever heard of the Fraud Seminar? SFCU teams up with the Montgomery County Sheriff’s Office to bring the community this eye-opening event. Scams are everywhere nowadays, but staying informed is key to protecting yourself. SFCU teaches the ins and outs of how to spot scams, protect your finances, and what to do if you fall victim to fraud.

And, if you feel a bit lost in the budgeting department, SFCU’s got your back. At their Budgeting 101 workshop at their Cicero branch, they’ll hook you up with all the tips and tricks to create a budget that actually works for you. Plus, there’ll be snacks and beverages to keep you fueled up while you learn.

You might also like: BILL Spend & Expense Card Review (Formerly Divvy Credit Card)

Frequently Asked Questions

Does Sidney Federal Credit Union have Zelle®?

Yes, Sidney Federal Credit Union does offer Zelle®. Simply log into the Sidney Federal Credit Union mobile app and select “Send Money with Zelle®.” From there, follow the prompts to enter the necessary information, accept the terms and conditions, and begin sending and receiving money.

What is the grace period at Sidney Federal Credit Union?

For most products, the grace period for Sidney Federal Credit Union is 10 days—This means that you have a window of 10 days after your due date to make payments without incurring any late fees. However, any payments received after this 10-day grace period will incur fees.

What is Sidney Federal Credit Union’s address?

SFCU’s main office is situated at 42 Union St., Sidney, NY 13838. Additionally, SFCU operates 11 branches across several counties in New York, including parts of Broome, Oneida, and Herkimer, as well as the entirety of Chenango, Delaware, Otsego, Cortland, Onondaga, Madison, Schoharie, Montgomery, Fulton, Hamilton, and Essex counties.

What is Sidney Federal Credit Union’s routing number?

The routing number for SFCU accounts is 221379905.

Final Thoughts

In summary, Sidney Federal Credit Union (SFCU) offers a range of financial products and services tailored to meet the needs of businesses in New York state. From business checking accounts and credit cards to loans, lines of credit, and savings options, SFCU provides comprehensive solutions to support entrepreneurial growth.

Additionally, their community involvement initiatives, such as the Hometown Day Parade and educational events like the Fraud Seminar and Budgeting 101 workshop, demonstrate their commitment to supporting and empowering local communities.

With accessible membership requirements and convenient customer service channels, SFCU strives to be a reliable partner in the financial success of its members—Just be sure to shop around and make sure you take advantage of the business financial products that best meet your needs and goals.

Do you want to learn how to obtain up to $100K in business credit in as few as 30 days? Join Business Credit Workshop today!