Since March 2021, when the U.K.-based company launched their U.S. business credit card, Capital on Tap has been a hot topic for business owners looking to obtain funding. They’re offering business credit lines up to $50K with cashback on all purchases. Sounds enticing, right? But, should you hop on this train or explore other options?

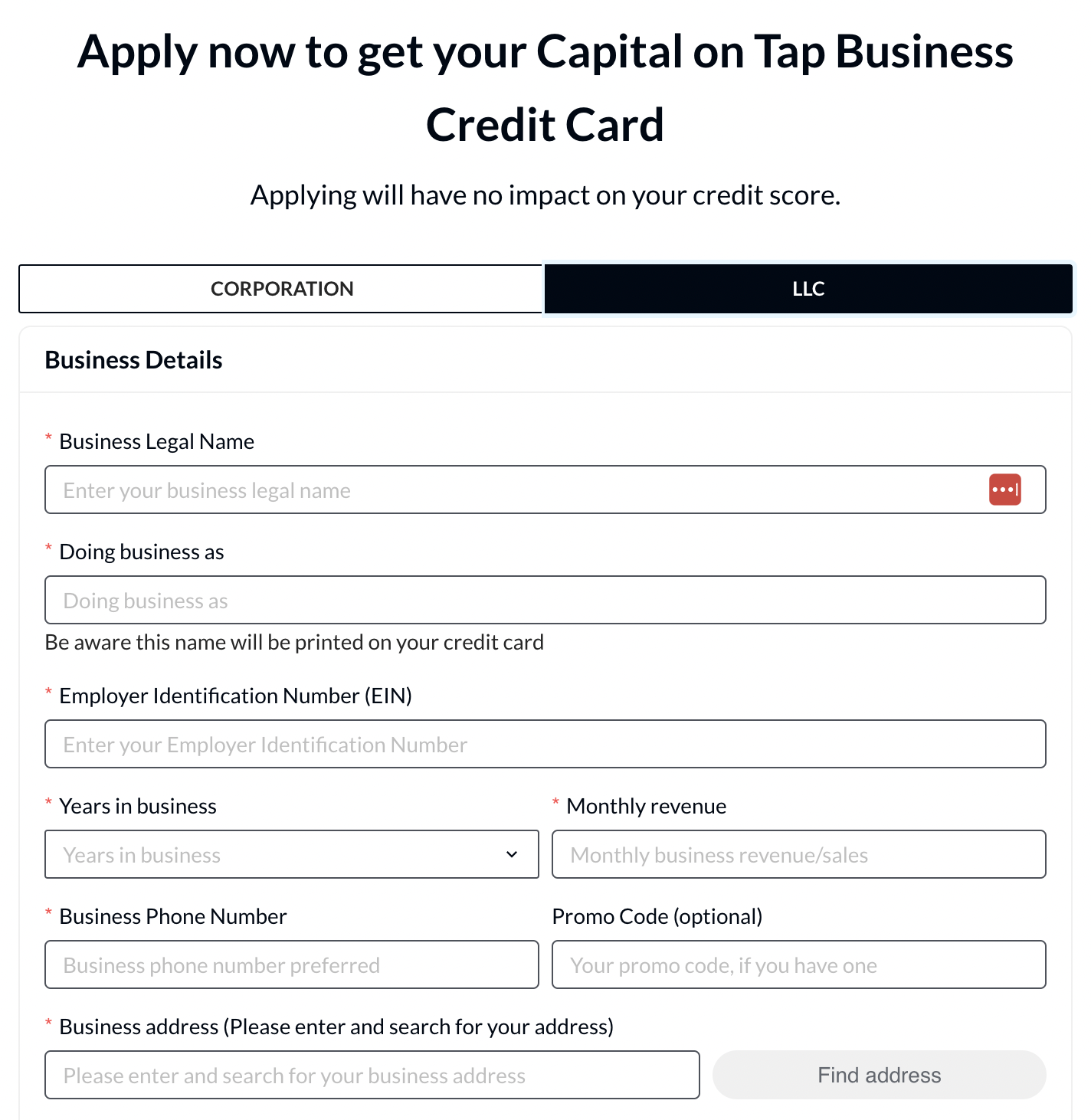

Apply now - takes 2 minutes and it will not impact your credit score. Your Capital on Tap business credit card will arrive within 4 days of approval!

We’ve done the research so that you don’t have to.

Here’s what’s in store:

- Company Overview

- What is a Capital on Tap Credit Card?

- Capital on Tap Competitor Overview

- Frequently Asked Questions

- Conclusion: Is Capital on Tap Legit?

Now, learn everything you need to decide if the offer is right for you.

Company Overview

While the name sounds like an offer that could be akin to Capital One, the two companies are unrelated.

Capital on Tap is a subsidiary of New Wave Capital Limited, based in London (incorporated in Whales and the U.K.). The company was founded in 2012 by David Luck, George Karibian, and Jan Farrarons. Prior to starting Capital on Tap, Luck was part of the operations group at a venture capital company called KKR Capstone.

Karibian and Farrarons also co-founded Dojo in 2009 and Judopay in 2012. Karibian is a serial entrepreneur who founded a couple of other companies prior to 2009. Both Dojo and Judopay are, to this day, successful payment processing companies.

Now, Capital on Tap credit cards for U.S. cardholders are issued by WebBank, headquartered in Salt Lake City, Utah. Originally founded in 1997, the company was acquired by Steel Partners Holding Corp.

What is a Capital on Tap Credit Card?

A Capital on Tap business credit card is a line of credit geared toward small businesses. In the US, They offer lines of credit up to $50K with 1.5% unlimited cashback on all spending. They boast that you can apply for a line of credit in as little as two minutes and get approved within 48 hours.

Despite some rumors, a Capital on Tap card does require a personal guarantee. So, if the business fails to pay the revolving debt as agreed, the individual/applicant will be responsible for the repayment. Business credit cards with no personal guarantee are actually very rare.

Recommended: Here’s How to [Actually] Get Business Credit With Just an EIN +More Options

Capital on Tap Requirements

If you’ve made it through the benefits overview, and this sounds like the card for you, let’s make sure you’re in a position to qualify for the offer.

Here’s what you need to have:

- Be the Director of or own at least 25% of your company

- Business based in the U.S.

- Business annual revenue of at least $30K

- Good personal FICO credit score

While Capital on Tap doesn’t broadcast its credit requirements, applicants with a score of 670 seem to be preferred. So, your odds of qualifying will increase with your FICO score. And, these requirements are actually fairly lax.

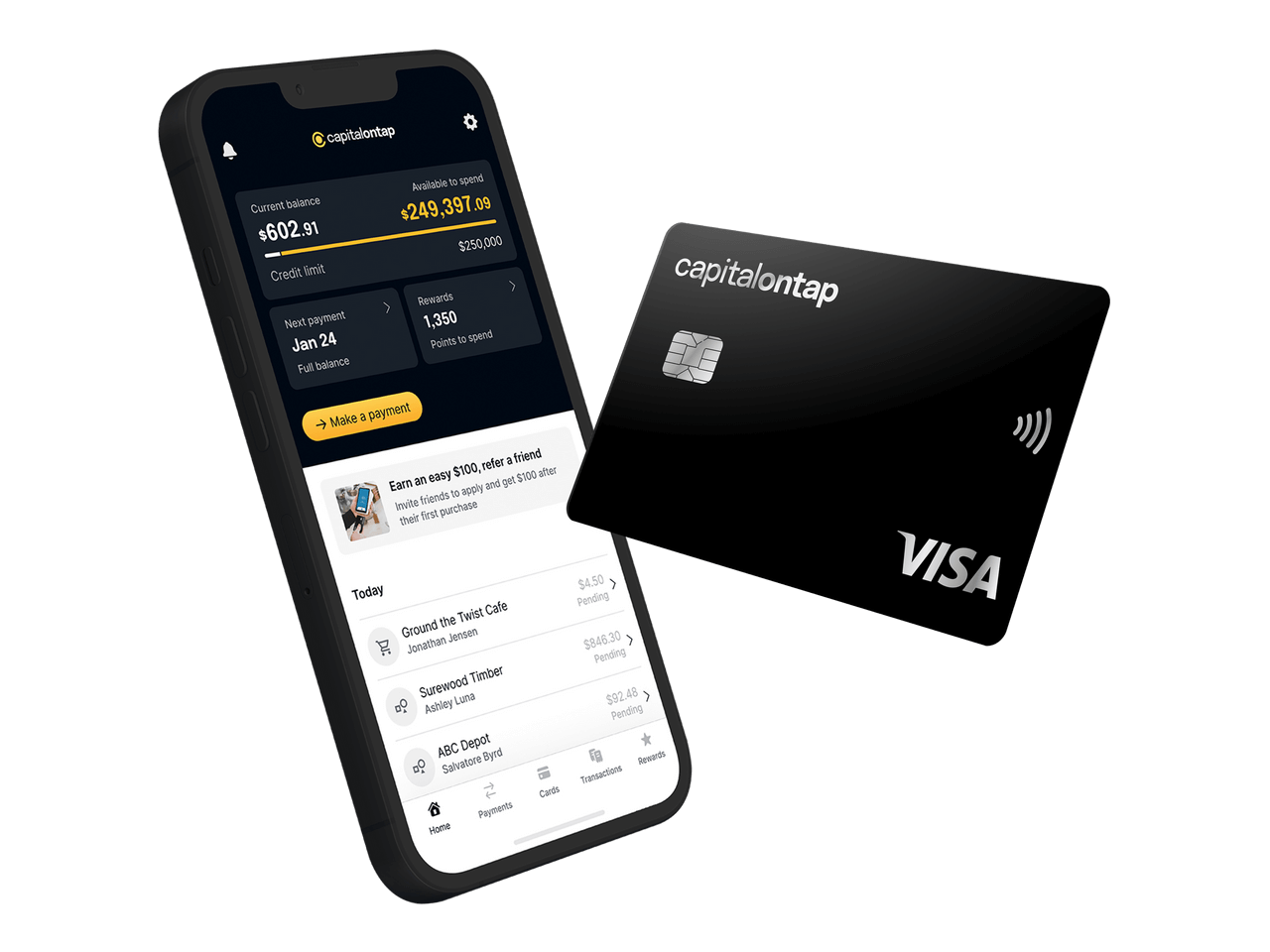

Capital on Tap Card Card Overview

Before you think about applying, why would you want to? Capital on Tap has features and benefits that, when compared to other offers, will help you make a decision about whether or not this is the right card for you.

- Unlimited Cashback – 1.5% cashback on all spending

- Instant Rewards Redemption– Cashback redeemed instantly to help repay your card balance

- Competitive Credit Limits – Credit lines as high as $50K

- Fee-Free – No foreign transaction fees or ATM charges

- Free Employee Cards – Unlimited, free cards for employee spending

- Spend Management – Budgeting tools to monitor employee spending

- No Annual Fee – Restrictions apply

While you can avoid interest “if you pay your balance in full each month,” actual interest for Capital on Tap cards ranges from 9.99% to 34.99% APR.

Furthermore, while there is no initial fee for ATM use, your interest rate may increase when you pull cash from your balance at an ATM.

Now, the Capital on Tap mobile app does have a 4.9-star rating in the iOS marketplace, which is impressive, as it outshines some of the biggest banks.

If you use the app, you’ll be able to make card payments, manage your cards and rewards, create virtual cards, and view transactions.

Capital on Tap Complaints

All business funding options come with their fair share of complaints. So, what do the people say is wrong with Capital on Tap’s offer? Only a small percentage of Trustpilot reviewers have had a bad experience. Here’s a summary of what unsatisfied cardholders and others don’t like.

- High interest rates

- Poor customer service

- Excessive junk mail

Note that most complaints mention the company’s advertising in one way or another — most do not mention the actual product. Keep in mind that financial “pre-approvals” are rarely a guarantee that you will qualify for a funding offer.

Capital on Tap Competitor Overview

Capital on tap is popularly compared to Amex and Capital One’s business credit card offers. So, let’s take a look at how they stack up side-by-side. For this case, we’ll compare the Capital on Tap Founder Rewards Card with Amex Blue Business Cash and Capital One Spark Business Cash specifically.

| Cashback | Annual Fee | Intro Offer | APR | FX Fees | |

| 1.5% | $0 | $200 w/$15K Spend in 3 Mos | 9.99% to 34.99% | 0% |

| 2% for 1 Year 1% Ongoing | $0 | $250 to $500 w/$5K to $10K Spend 3 Mos | 13.24% to 19.24% | 2.7% |

| 2% | $95 | $500 w/$4.5K Spend in 3 Mos Deferred Annual Fee | 20.99% Variable | 0% |

All of the cards come with their own set of pros and cons. For example, a Capital on Tap card comes with the lowest possible interest rates (9.99%) on regular spending, but can also be the highest (up to 34.99%). Spark Business Cash and Amex Blue Business offer the best introductory offers (Up to $500 with qualified spending). And, neither the Founder Rewards card nor the Amex Blue Business card will charge an annual fee.

You’ll need to decide which features are most important to you.

Frequently Asked Questions

What credit score do you need for capital on tap?

Capital on Tap has no set credit score requirement, but applicants with a score of at least 670 have a higher chance of qualifying.

Is capital on tap a soft pull?

Yes. While a Capital on Tap card does require a personal guarantee, the credit pull is soft, so it will not impact your personal FICO score to apply.

Does capital on tap require a personal guarantee?

Yes. If your business fails to make payments to Capital on Tap, you will be personally liable for the debt.

Is capital on tap a charge card?

No. Capital Tap is a credit card, with a revolving line of credit.

Which credit bureaus does Capital on Tap report to?

Capital on Tap reports payment history to Experian business.

Apply now - takes 2 minutes and it will not impact your credit score. Your Capital on Tap business credit card will arrive within 4 days of approval!

Conclusion: Is Capital on Tap Legit?

From what I can tell, the Capital on Tap offer stacks up well against the competition and offers some decent benefits for a business in the right position. As you know, it’s not your only option. While it’s not my absolute favorite business credit card, it’s definitely one that I refer a lot of my coaching clients to check out.

If you want to learn how you obtain $100K in business credit in as few as 30 days, join Business Credit Workshop today.