In the world of small business, access to credit can be a game-changer. Whether you’re a seasoned entrepreneur or just starting, the financial flexibility to seize opportunities, manage cash flow, and fuel growth is essential.

That’s where the Nav Prime Card might step in as a compelling tool to help you navigate the complex landscape of business credit.

But, is it right for you?…That’s what I’m going to answer here.

This is what’s in store:

- What is the Nav Prime Card?

- Nav Prime Card Overview

- Who Wouldn’t Want a Nav Prime Card?

- How to Get Started with the Nav Prime Card

- Frequently Asked Questions

- So, is the Nav Prime Card legit?

Now, let’s roll!

What is the Nav Prime Card?

The Nav Prime Card is a charge card offered by Nav Prime ($49.99/month), designed for small businesses. It allows users to build business credit without an annual fee or personal guarantee. Unlike a credit card, it requires no security deposit and is linked to the user’s business checking account for daily use.

Nav can boost your business credit score and provide personalized funding recommendations for your small business you can't find anywhere else.

This card is more than just a piece of plastic. It can be a financial lifeline for small businesses, offering a range of benefits designed to help you build, strengthen, and leverage your business credit profile.

The Prime Card is issued by Blue Ridge Bank, N.A., adding a layer of credibility. Moreover, Nav, the company behind Nav Prime, is a well-established player in the business credit space, offering a range of financial tools and resources for businesses.

Before Nav became Nav in 2012, the company was called Creditera, and was helping to boost business credit scores before most of the other players in the game.

Let’s dive into the details and explore why the Nav Prime Card is becoming a top choice for savvy entrepreneurs.

→ Recommended: Nav Review: A Tool that Helps Build Up Your Business Credit Score

Nav Prime Card Overview

When it comes to the financial success of small businesses, one element often stands out: building a robust business credit profile. But, this isn’t always straightforward to achieve, especially if you’re just getting started or have limited credit history.

That’s where the Nav Prime Card steps in, offering a solution to this common challenge.

Business Credit Building Features

Building a robust business credit profile is a cornerstone of financial success for small businesses. However, it’s not always easy, especially if you’re just starting or have limited credit history.

The Nav Prime Card is specifically designed to address this challenge.

Here’s how it works:

- It’s a charge card – Unlike traditional credit cards, the Nav Prime Card is a charge card, which means you need to pay your balance in full every month.

- There’s no credit check – One of the hurdles many small business owners face is the dreaded credit check. The Nav Prime Card removes this barrier by not requiring a credit check for approval. This is fantastic news for those with less-than-perfect credit or those looking to avoid inquiries on their personal credit reports.

- The account reports as a tradeline – The Nav Prime Card reports your payment activity as a tradeline to major credit bureaus. This is where the magic happens; your responsible card usage translates into positive data on your business credit report, gradually boosting your business credit scores.

→ Recommended: Using 30 Day Net Vendors to Build Your Business Credit Score

No Security Deposit Required

Securing a traditional business credit card often involves putting down a security deposit, which ties up your capital. The Nav Prime Card eliminates this requirement, giving you access to credit without tying up your cash. It’s a win-win for your business’s financial health.

Daily Autopay Feature

Managing your credit card balance can be a juggling act. The Nav Prime Card simplifies this process with its daily autopay feature. Instead of fretting over a big monthly bill, your card balance is automatically paid down daily, which reduces the risk of carrying a high credit balance and potential interest charges.

Second Monthly Tradeline

In the world of credit building, tradelines are your best friends – The Nav Prime Card provides a unique advantage by automatically sending two monthly tradelines to all three major credit bureaus. This means your positive payment history is widely reported, strengthening your business credit profile faster.

But, it’s not right for everyone.

→ Recommended: Here’s How to [Actually] Get Business Credit With Just an EIN +More Options

Who Wouldn’t Want a Nav Prime Card?

While while Nav Prime has a good offer, here are some of the groups who might not want to take advantage of the card offer:

- Budget-savvy startups – If you’re a fresh-faced startup trying to make every dollar count and the Nav Prime Card asks for a monthly fee of $49.99 for Nav Prime, this could throw a curveball into your penny-pinching game. Early-stage businesses might steer clear to keep their costs in check

- Privacy buffs – If you need to guard their data like a treasure chest, keep in mind that the Nav Prime Card wants access to your bank accounts to set a credit limit. If you need to be all about data security and privacy, you might go, “No way!” and opt for another option. (But, nearly all card offers will require that you share at least some identifying info).

- Geographically-challenged folks – Is your business California, Nevada, North Dakota, or South Dakota? Unfortunately, the Nav Prime Card doesn’t roll out the welcome mat in these states. So, if you’re doing business in any of these areas, it’s a no-go.

- Owners looking for a credit card – If you’re in the market for an unsecured credit card that you can use to expand and grow your business, you don’t need a business credit builder card (you might check out one of these instead).

These are the kinds of folks who might give the Nav Prime Card a polite pass. Whether they’re all about frugality, data security, or just prefer a different financial vibe, they’ve got their reasons to set their eyes on a different offer.

→ Recommended: Torro Business Funding Review: Is This “Zero Hassle” Offer Legit?

How to Get Started with the Nav Prime Card

Now that you’re intrigued by the Nav Prime Card’s benefits, you might be wondering how to get your hands on one.

Here’s a step-by-step guide to kickstart your journey to building and leveraging business credit with Nav Prime:

- Step 1: Check your eligibility

Before applying for the Nav Prime Card, ensure that you meet the eligibility criteria. While the card is designed to be accessible, it’s essential to confirm that your business qualifies.

In simple terms, if you want to sign up for a Platform Account, you need to meet some requirements:

- Your business must be based in the United States.

- You should have an active Nav Prime subscription.

- You have to complete identity verification, which means proving who you are.

- Your business can’t be involved in certain activities like adult entertainment, selling cannabis, dealing with cryptocurrency, running gambling or online gaming, or anything else that doesn’t go well with this card.

- The person applying for the account must be at least 18 years old and allowed to do this on your behalf.

- They might look at some other things to decide if you can get an account or the card, but that’s up to them.

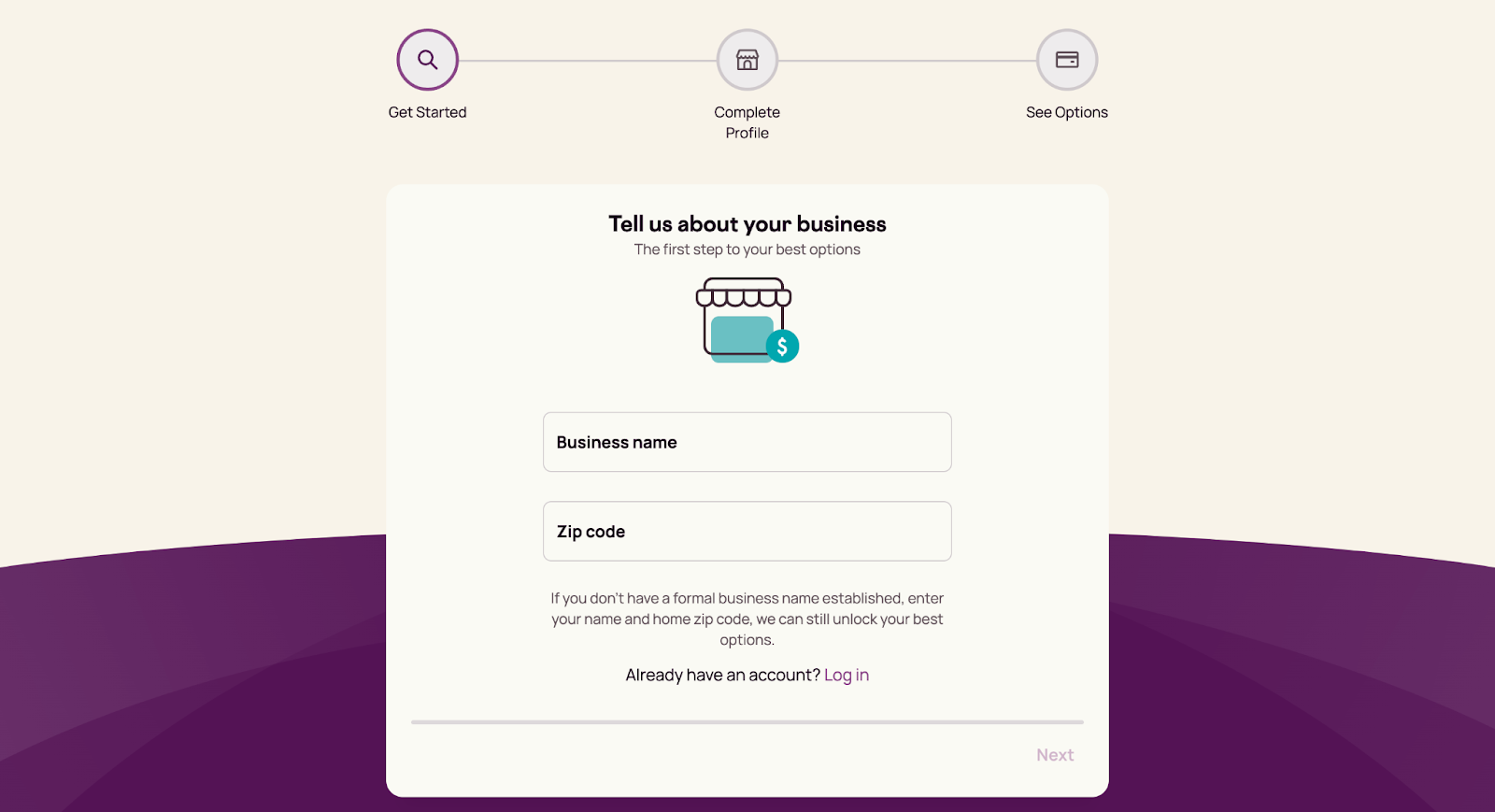

- Step 2: Apply online

The application process for the Nav Prime Card is straightforward and can be completed online. Be prepared to provide basic information about your business, such as its legal structure and industry.

- Step 3: Link your bank account

To set your credit limit and enable daily autopay, you’ll need to link your business bank account to your Nav Prime Card account – This step streamlines your finances, providing insights you can’t get from your bank alone.

- Step 4: Use your card responsibly

Once you receive your Nav Prime Card, it’s time to put it to work. Use it for your everyday business expenses…but remember that it’s a charge card, so paying your balance in full each month is crucial.

- Step 5: Watch your business credit grow

As you consistently use your Nav Prime Card and make on-time payments, you’ll start to see the positive impact on your business credit profile. Over time, your business credit scores will rise, opening doors to better financing options.

Frequently Asked Questions

What's the difference between a charge card and a credit card?

While both types of cards allow you to make purchases, there’s a key distinction. A charge card requires you to pay your balance in full each month, while a credit card allows you to carry a balance and make minimum payments. The Nav Prime Card is a charge card, offering the benefits of credit without the risk of long-term debt.

Can the Nav Prime Card help me secure business financing?

Yes, absolutely. By consistently using and managing your Nav Prime Card responsibly, you’ll build a strong business credit profile. This, in turn, enhances your eligibility for various financing options, including business loans, lines of credit, and more favorable terms.

Is the Nav Prime Card available nationwide?

Nav Prime Card is available in most states; however, it’s not currently offered in California, Nevada, North Dakota, or South Dakota.

How long does it take to see improvements in my business credit scores with the Nav Prime Card?

The timeline for credit score improvement can vary based on several factors. According to data tracking Experian® Intelliscore Plus business credit scores, many users have seen improvements of up to 50% in the first three months of having Nav tradeline reporting. Results may vary, but responsible card usage is key to achieving these improvements.

So, is the Nav Prime Card legit?

The Nav Prime Card is more than just a business charge card; it can be a powerful tool for building, strengthening, and leveraging your business credit profile.

With its unique features, including no credit checks, no security deposit, daily autopay, and the reporting of two monthly tradelines, it’s a valuable asset for small business owners looking to secure better financing options and improve their financial health.

If you’re ready to take control of your business credit journey, you can spare $49 per month for full access to Nav Prime, and if you’re in a region where the offer is available, the Nav Prime Card is probably worth looking into.

Do you want to learn how to get up to $100K in business credit in as few as 30 days? Join Business Credit Workshop today!