Key Takeaways

- Amex Business Checking earns 1.3% APY on balances up to $500K (and a longstanding 30K-point intro bonus for meeting account requirements).

- No monthly maintenance fees and free MoneyPass™ ATM access.

- Rewards debit card earns 1 point for every $2 spent, to help you accumulate rewards.

- High deposit limits accommodate balances up to $5 million, surpassing many competitors.

- No QuickBooks integration, no cash deposits, and limited support for Android users.

- Competitors like Bluevine and Novo offer higher APY, cash deposits, and additional features like virtual cards.

I first came across Amex’s new business checking account in a private Facebook group post back in 2023. While the company has been around for decades, American Express previously only serviced credit card and travel-related offers. Now, they’ve got a checking account that earns interest on up to $500K with enticing introductory bonus points for new accounts.

So, let’s explore the new offer in full, and find out what you need to know whether this is the right checking account for your business.

Here’s what’s in store:

- Amex Company Overview

- The Amex Business Checking Account

- Amex Business Checking Competitor Overview

- Frequently Asked Questions

- The Takeaway

So, let’s get to it!

Amex Company Overview

So, why is Amex so popular? Well, this NY-based institution has been around since 1850, servicing consumer and business credit, expense management, and travel products. The founders were Henry Wells, Irene Tserkovny, John Butterfield, and William Fargo.

Do any of these names sound familiar? As you might have guessed while reading (if you didn’t already know), Butterfield, Wells, and Fargo are the same people who founded Wells Fargo in the mid-1800s.

While big banks don’t tend to inspire everyone’s confidence, the fact that the company has been around for over a century is telling. Amex is a trusted name in American finance, and the odds are that they’re going to stick around for many years to come; this is important in an age where new, cutting-edge financial products are in and out of existence after a year or two in the marketplace.

Currently, American Express is a publicly-traded, for-profit global financial services company led by CEO Stephen Squeri. They’re best known for their credit cards, charge cards, and traveler’s checks. Lately, their checking accounts are quickly rising in reputation.

You might also like: A Complete, Unfiltered Amex Business Gold Card Review

The Amex Business Checking Account

In short, an Amex business account gives you the opportunity to earn interest and introductory rewards with free, online checking. Since every business needs a bank account, it may seem like you’ve nothing to lose by signing up.

And, while there are some great features with Amex business checking, there are some missing features…not all contemporary online checking accounts are the same. Read everything below to weigh the pros and cons for yourself.

The Introductory Bonus

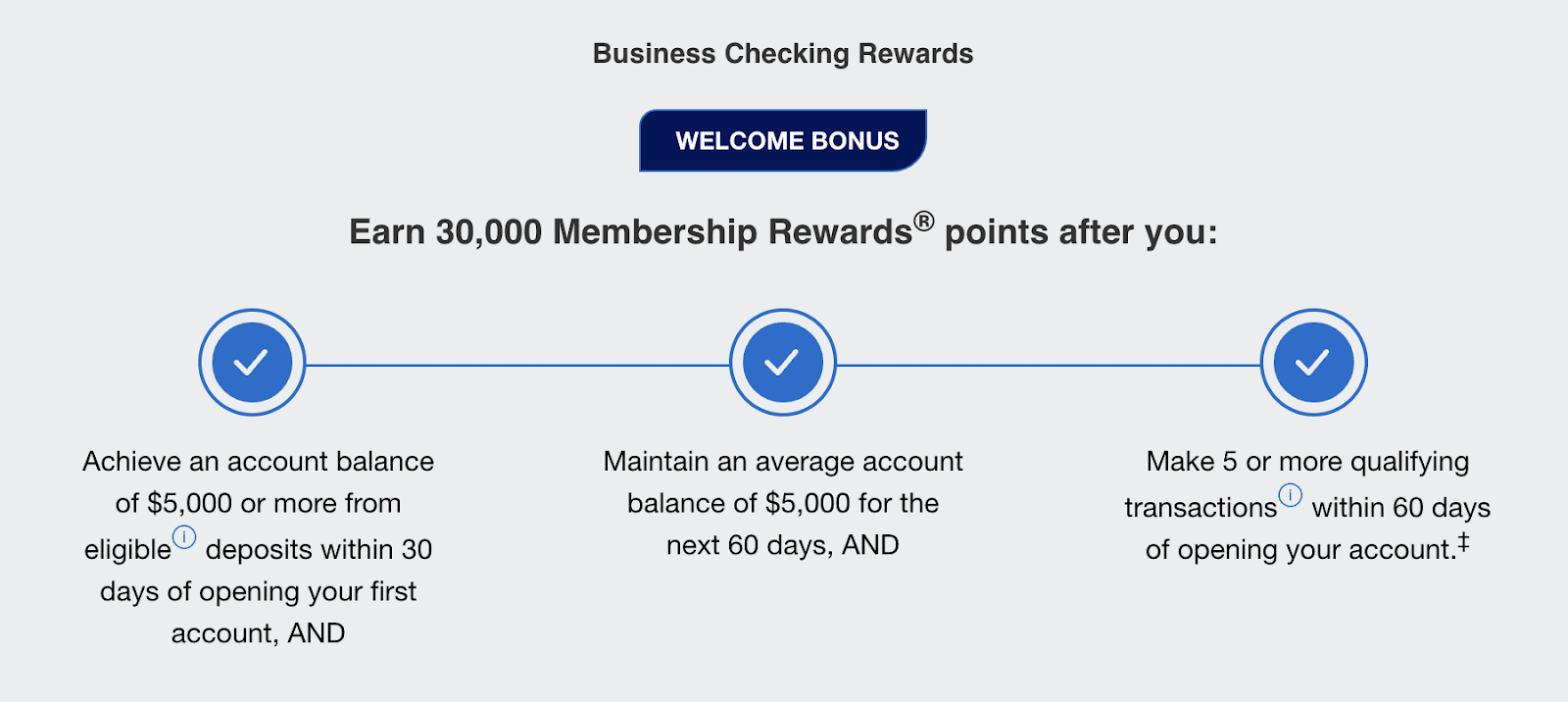

One of the most hyped benefits of an Amex business checking account is the intro offer. Currently, they’re giving away 30K rewards points (worth about $300 total) with qualifying activities on a new account. And, this offer has been in play since 2023, so they may stick with it.

Here’s what you’ll have to achieve to get the bonus points:

- Account balance of $5K within 30 days of opening your account

- An average account balance of $5K for the following 60 days

- 5 or more “qualifying transactions” within 60 days of opening your account

If you apply, are approved, and meet these requirements, the points should be distributed to your account at the end of the 90-day wait. Keep in mind that the intro offer is likely to change — some people got in when they promised 20K points and others were offered 60K.

So, what are “qualifying transactions?”

✅ Mobile deposits

✅ Check deposits by mail

✅ Electronic/online transactions (ACH, wire, and bill payments)

And, what are not qualifying transactions?

❌ Business debit card transactions

❌ Deposits using the “Redeem for Deposits” feature

We’ve seen other brands like Wells Fargo and Chase offer anywhere from $200 to $500 for new individual and business accounts with qualifying activities. The key difference with this offer is that Amex is delivering an online bank account, which is best compared to offers like Bluevine and Novo.

You might be wondering how hard it would be to get 5 or more qualifying transactions within 60 days (if this won’t be your primary account), and the answer is, ‘it would be pretty easy.’

All you would have to do is divide your deposit amount requirement ($5K) by the number of transactions you need (5) and make the appropriate number of mobile, check, or ACH payments into your new account (5 X $1K deposits) within the first month of opening the account.

But, don’t get ahead of yourself trying to work the system…you might actually decide to keep your account once you get in and realize the benefits.

Amex Checking Account Features

In a word, Amex checking accounts have some pretty cool benefits:

- Earn interest on checking account balance

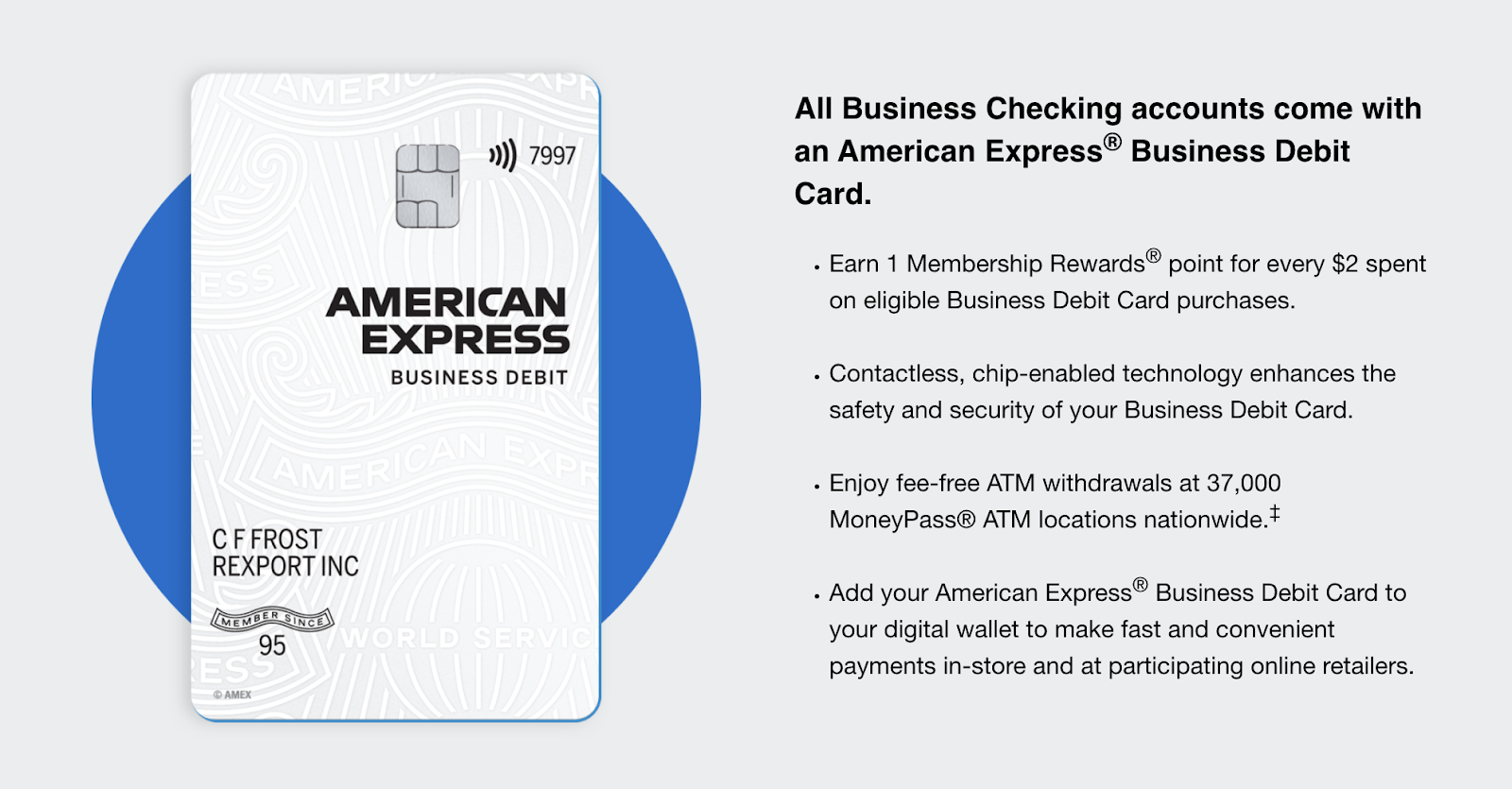

- Get 1 Amex point for every $2 spent

- Pay no monthly maintenance fees

- Gain fee-free MoneyPass™ access

- Take advantage of high deposit limits

- Get free, fast outgoing ACH

- Send free eChecks and use fee-free checkbooks

- Keep your Amex MR points alive

Just for fun, let’s explore the offer a bit more in-depth.

In addition to the intro points offer, Amex business checking accounts earn 1.3% variable APY on balances up to $500K.

So, you have a chance to earn a bit — an account with an average balance of $5K could be earning $65 each month. While most savings accounts offer the opportunity to earn, this isn’t a standard feature with checking accounts. With that said, Bluevine offers a 2% fixed APY on accounts that carry up to $100K, so that part of their offer outshines Amex.

Amex is the only popular online bank account with a rewards debit card that earns 1 point for every $2 spent. If you use your debit card to spend $200, you can earn $1. This may not sound like a lot, but rewards can add up quickly.

Plus, you’ll pay no monthly maintenance fees for an Amex business checking account. While most business bank accounts charge anywhere from $10 — like NorthOne, for example — to $30 per month, Amex checking is free (note: so are Novo and Bluevine’s offers).

With an Amex business checking account, you’ll incur no ATM fees within the MoneyPass™ network. You might, however, have to pay third-party fees. Note that Novo bank refunds third-party ATM fees at the end of each billing cycle, though there’s no telling how long this reimbursement offer will last since the company is in the earlier stages.

Furthermore, they have high deposit limits, which we can’t say for other online bank accounts and neobanks; most online checking offers are capped at $1K or $5K per day while Amex won’t cap your deposits — You can keep up to $5 million in your account.

And, you’ll never pay the typical fees you see with business checking accounts. So far, users have been satisfied with outgoing ACH, citing that it’s fast (usually same-day) and free to send money to external accounts. Checks are also free, and there are no fees for NSF, stop pay, billing inquiries, replacement cards, late fees, or admin processing.

Finally, you can save your existing Amex reward points, even if you plan to close out credit card accounts to bypass annual fees. Automatically redeem existing MR points in your Amex checking account.

All-in-all, an Amex checking account could save you some money while it expands opportunities to earn and grow your business.

What is the Downside of American Express Checking?

As with all financial offers, there are some downsides for Amex checking account holders.

One of the most glaring issues for me is that there is no Quickbooks integration with an Amex checking account yet. However, you can connect an Amex account to Quickbooks online. 🤷

Furthermore, if you want to deposit cash, you’ll first have to exchange it for a money order or check, then transfer the funds to your account. No cash deposits could be extremely inconvenient for cash businesses. You can withdraw cash from an Amex account via ATM using your debit card.

And, as with all online bank accounts, you won’t be able to walk into a branch — they don’t exist. If this is important to you, choose a local branch to open your business bank account.

There’s also a rumor floating around that Amex checking accounts don’t offer wire transfers, but it isn’t true; incoming wires are free while outgoing wire transfers cost $20. And, this price is pretty typical.

Where Amex checking accounts actually fall short is in the fact that they facilitate no INTERNATIONAL wire transfers. If you really want to go with Amex, you can look into solutions from Wise or Plastiq for this — these platforms are more user-friendly than your typical wire process anyway.

Finally, if your business credit card is serviced through Amex, and you have any issues that arise at no fault of your own (overdrafts, chargebacks, etc.), these could negatively impact your credit accounts.

Some business owners opt to use different institutions for business credit and business banking because of this, though I recommend a different approach.

Amex Business Checking App

The Amex business checking app is only available on iOS (they do have an Android app for credit accounts), so any Android users will need to access their account from another device.

As a Google Play person myself, this seems a bit silly to me — there are lots of apps available for Apple while unavailable on Android, but I would think an online banking account would see the importance of serving customers across all devices.

But, if you’re an iOS user, keep reading…

The Amex business checking app allows you to create and schedule payments on the go, and it’s pretty slick. In addition to the usual app features like mobile deposits, transfers, and payments, you can manage and redeem Amex rewards points.

I mentioned this previously, but you may have missed it: existing Amex rewards members’ rewards points are automatically added to your checking account. I think this is pretty cool.

With this said, the app doesn’t have the best user ratings, so I have a quick tip for ya: if you find that your two-factor authentication is wonky, delete and reinstall the app — this seems to be solving the issue for existing app users (Plus, my bet is that the developers are getting this worked out as we speak).

Amex Business Checking Competitor Overview

The two brands with the closest offers to Amex’s current small business checking are Novo Bank and Bluevine. So, let’s look at how these three accounts stack up next to one another:

The most enticing competitive advantage is that Amex currently has the highest deposit limit. If you’re earning more than $5K via a website, app, or your POS, then neither Novo nor Bluevine will work for you — In this case, Amex would be a natural choice.

If you’re earning a little less, Bluevine might give you the opportunity to earn more on your monthly balance with 2% interest vs 1.3% with Amex; plus, they are the only solution that offers cash deposits.

And, Novo’s got the monopoly on virtual cards, reimbursed third-party ATM fees, and built-in invoicing (for now).

Keep in mind, you don’t have to choose an online business checking account. In fact, I typically recommend small business owners bank with small, local community banks for the best business credit opportunities (among additional interpersonal benefits).

Recommended: 3 Best Credit Unions for Small Business Banking

Frequently Asked Questions

Does Amex business checking pull credit?

No. When you apply for an Amex business checking account, you’ll be shown a consumer reporting disclaimer. This does not mean that opening an account will affect your credit score.

Does American Express business checking use Zelle?

No. Most business checking accounts are incompatible with Zelle. However, Bank of America and PNC Bank might be Zelle-compatible. Please check with the Banks for an up-to-date answer.

Can you use Venmo with American Express?

Yes! You can use the Send & Split™ feature in the Amex app to send money with Venmo.

How do I deposit cash into my American Express business checking account?

Unfortunately, American Express doesn’t support cash deposits. So, you will have to somehow convert any cash into a check or money order to make a deposit into an Amex checking account.

How much is 60K Amex points worth?

60,000 Amex points are worth roughly $600. Though, they can be redeemed for more through American Express’ promotional and travel offers.

Final Takeaway: Is Amex Worth the Hype?

If you’re an Android user, you run a cash business, or you expect a Quickbooks integration with your account, American Express might not be your top choice for business checking—But, it does have some pretty cool features.

If you’ll be depositing tens of thousands of dollars into your account, Amex is clearly the best online banking option, though I still recommend local community banks and credit unions where you can walk into a branch and build a relationship with the banker.

If you want to learn how to obtain up to $100K in business credit in as few as 30 days, join Business Credit Workshop today.